Equity Market Updates

Market sentiment was positive, despite a softer US Q2 GDP growth. Brent crude oil stabilised near $84 per barrel amid signs of improving shipping activity through the Strait of Hormuz and continued diplomatic efforts to ease regional tensions.

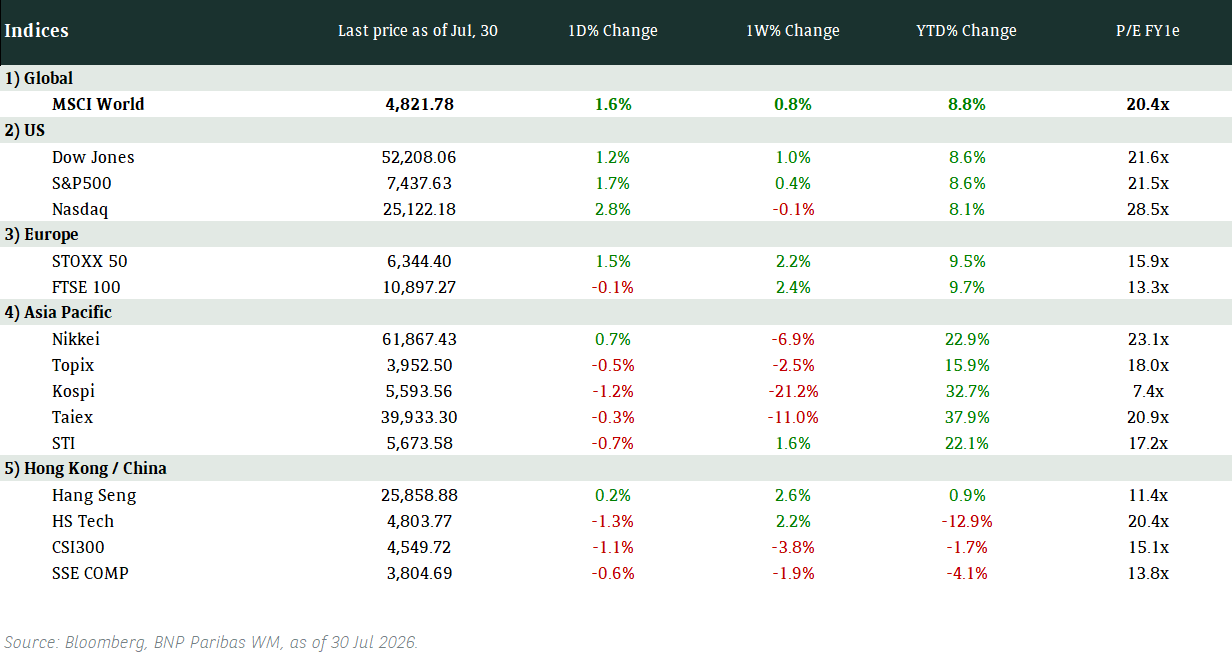

Wall Street closed out July 2026 on a high note, led by a powerful tech rally that snapped a multi-session losing streak. Benchmark US indices advanced strongly, particularly the tech-heavy Nasdaq. The upside momentum was spearheaded by blockbuster mega-cap technology earnings, most notably Microsoft, which surged over 15% after its Azure cloud division surpassed $100 billion in annual revenue. Semiconductor stocks rebounded aggressively, with the PHLX Semiconductor Index jumping 8% as dip-buyers re-entered the trade.

Inflation-wise, US headline Personal Consumption Expenditures (PCE) eased to 3.7% from 4.1%, while core PCE inflation edged down to 3.3% from 3.4%, both in line with forecast. Nonetheless, the market still expects a 25bps rate hike at the next Federal Open Market Committee (FOMC) meeting in September 2026. We continue to see a rate hike in December 2026, and no further hikes in 2027.

Equity Market Updates

European shares gained on Thursday as strong earnings in cyclical sectors such as financials and industrials offset worries about geopolitical uncertainties in the Middle East.

Within Europe, we maintain relative preference towards healthcare, industrials, and utilities.

Amazon (AMZN US)

Shares of Amazon surged during post-market trading on Thursday after its cloud-computing revenue accelerated for a fifth straight quarter, easing investor concerns about AI monetisation. The company’s Q2 top- and bottom-line both exceeded market expectations, helped by a 37% jump in AWS sales to USD42.2bln. Nevertheless, Amazon’s Q3 sales forecast was weaker than expected at between USD197bln and USD202bln vs. USD203.9bln expected.

MARKET CONSENSUS: 79 BUYS, 4 HOLDS, AVERAGE TP USD315.79

Mastercard (MA US)

Mastercard on Thursday reported better-than-expected Q2 results, featuring a 21% rise in adjusted EPS as the company benefitted from its expansion beyond traditional payment-network services. Total spending volume on Mastercard’s network jumped to USD2.88tln vs. USD2.86tln expected.

MARKET CONSENSUS: 47 BUYS, 2 HOLDS, AVERAGE TP USD650.1

Apple (AAPL US)

Shares of Apple fell during after-market hours on Thursday as component shortages weighed on the company’s sales forecast. It now expects revenue to rise 9% to 11% in FY4Q vs. 12% expected by the market. In terms of overall FY3Q results, Apple’s revenue and net profit both exceeded market estimates.

MARKET CONSENSUS: 36 BUYS, 18 HOLDS, 4 SELLS, AVERAGE TP USD323.27

Shell (SHEL LN)

Shell announced on Thursday Q2 net income that nearly tripled YoY to USD10.8bln. This was mainly due to strong operational performance, despite severe disruption across global energy markets. The company maintained its 2026 capex forecast of USD25bln.

MARKET CONSENSUS: 14 BUYS, 11 HOLDS, AVERAGE TP GBp3731.97

Adidas (ADS GR)

Shares of Adidas fell more than 11% on Thursday after it announced Q2 operating profit that missed estimates, dragged by 30% higher marketing spend compared to Q2 2025 due to FIFA World Cup campaigns. Despite the earnings miss, Adidas’ Q2 sales rose 13.3% YoY to EUR6.7bln, with the company also increasing its sales outlook for the year.

MARKET CONSENSUS: 70 BUYS, 4 HOLDS, AVERAGE TP USD555.13

Earnings Announcements

Global Indices Changes (%)

Fixed Income Market Updates

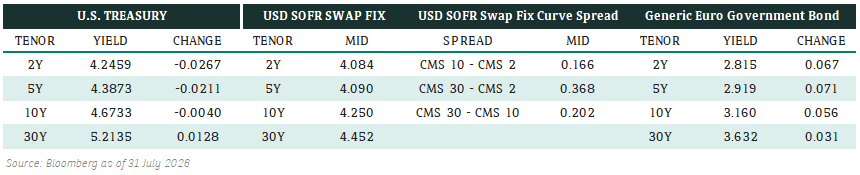

We saw the futures market reprice the odds of a September rate hike downwards from 100% to ~65% following the Fed's rate decision. This stoked inflation fears, pushing the 30-year US Treasuries up to 5.23% during Asia hours. While most market participants remain cautious towards the month-end, the higher rates backdrop gives better entry opportunities for all-in yield buyers to gradually pick-up risk.

With focus shifting to the upcoming inflation and labour market data to determine future rate hike path, we suggest to remain selective with a preference for investment grade and the short-end to the belly of the curve.

European Bank coco (AT1)

European AT1s continued to trade range-bound +/- 25 cents with two-way flows amid the macro volatility. Buyers stepped in whenever the prices dipped especially for the perpetual AT1 CoCo bonds with short call dates up to 5-years. With the July month-end portfolio rebalancing, the battle for better yields vs tightening spreads continue to play out across currencies in the AT1 CoCo space.

Asia Investment Grade (IG)

Asian IG credit continued to trade sideways with overall spreads trading flat to +/-2bps at market close amid subdued activity and thin liquidity. Any loose offers in the market were easily absorbed by all-in yield buyers. Although there were some two-way flows on long-dated papers, it continued to underperform as investors remained cautious in adding duration. Perpetuals and AT1 bonds closed about 25 cents lower on the day. In China IG space, onshore investors were picking up the 5-year to 10-year papers of technology/media/telecom names. Away from China, India and Japan IG financial names continued to see better buying interests. Investors remained largely cautious on Korea IG names, albeit selling pressures eased for some companies like LG Energy Solution post stable earnings report. In Australia, investors continued to selectively add AUD bonds and the USD bonds of Australian IG credit names in their portfolios.

Asia High Yield (HY)

As expected, Asian HY bonds generally traded on a weaker tone with lower cash price (-25 cents to -50 cents) and wider spreads at market close. Activity going to the month-end was muted as the rates volatility remained elevated. Selling interests were seen in Softbank bonds, with prices falling 50 cents to 1 point at market close. In India HY space, there were sellers of HY non-bank financial names like Muthoot. Vedanta USD bond complex closed 25 cents lower despite some buying interest seen on the longer end of its curve.

Forex Market Updates

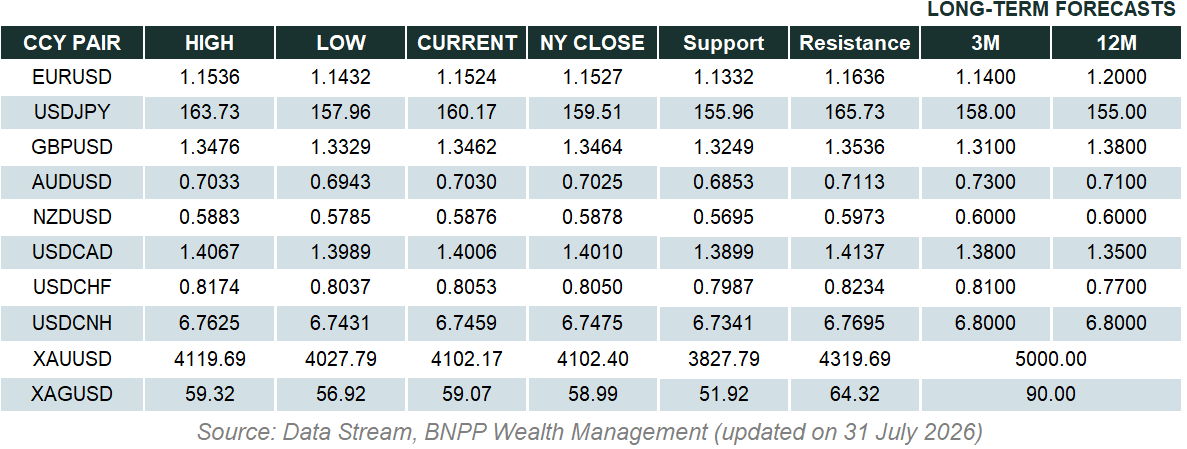

The US Dollar index eased on Thursday following the latest data release of a softer PCE at 0.1% month-on-month versus the forecasted 0.2, suggesting less urgency for rate hikes by the Fed.

USD

The Dollar index eased to around 99.86 on Thursday following latest data release of a softer PCE at 0.1% month-on-month versus the forecasted 0.2%, suggesting less urgency for rate hikes by the Fed as markets at the same time, digested the FOMC's decision to hold rates at 3.50% – 3.75% for a fifth consecutive meeting. The FOMC voted 9-3 to leave rates unchanged, with three members dissenting in favour of an immediate hike. Chair Warsh stressed that the hold should not be viewed as a sign of policy inertia, adding that markets would continue to respond to incoming economic data, but the absence of an immediate hike was enough to prompt a modest unwind of long dollar positioning built ahead of the decision. On the middle east side, fresh US air strikes on Iran resumed following attacks on American forces in the region, keeping the conflict live and limiting any deeper dollar pullback.

The Dollar index may see some level of easing as CPI data suggests less urgency for rate hikes.

GBP

The Sterling traded higher at 1.3465 as the Bank of England kept its key interest rate at 3.75% on Thursday, with the MPC voting 6-3 to hold following a bigger-than-expected drop in June inflation, which gave policymakers breathing space to assess the fallout from renewed fighting in Iran. This is also an escalation from June's 7-2 split and signalling growing internal MPC pressure for a hike. Governor Andrew Bailey mentioned that inflation had “fallen faster than we’d expected” but warned that recent escalation in the Middle East conflict could mean prices are likely to rise again.

The Sterling may see gradual strength in the near term as a hold with a hawkish shift in vote count keeps the currency supported.

JPY

The Dollar-Yen fell sharply by as much as 3% in what analysts said looked like official intervention by Tokyo on Thursday. The fall could also be further driven by pre-decision positioning as traders are trimming short yen exposure ahead of the BOJ announcement, wary of a hawkish hold that catches the market off guard given the yen's proximity to 40-year lows. Core consumer price index inflation rose 1.9% year-on-year in July above the expectations of 1.8% showed that inflation continues to pick up amid support from elevated energy prices. On the backdrop of mounting inflationary pressure from the Middle East war, weak yen and global AI demand, markets look to see how Governor Kazuo Ueda will signal during the press conference.

The Yen looks for direction from the BoJ rate decision and Ueda’s press conference language on Friday.

XAU

Gold rebounded to around $4,100 per ounce on Thursday after some encouraging data on inflation. The Fed decision to hold on interest rates also brought relief to bullion investors, as higher rates reduce demand for the non-yielding metal. Turning to the Middle East conflict, the renewed escalation kept oil prices elevated, raising concerns of inflation risk which complicates Fed’s path toward easing monetary policy after renewed strikes against Iran with U.S Central Command describing it as “a powerful response” for the attempted Iranian strikes on American forces a day earlier.

Gold may stay supported at $4,100 level in the near term.

Please read carefully the disclaimer here:

Asia Disclaimer:

https://wealthmanagement.bnpparibas/asia/en/disclaimer1.html

Europe Disclaimer:

https://wealthmanagement.bnpparibas/ch/en/disclaimer.html