Market Daily

Macro Update:

Yields rally as investors eye key data and earnings

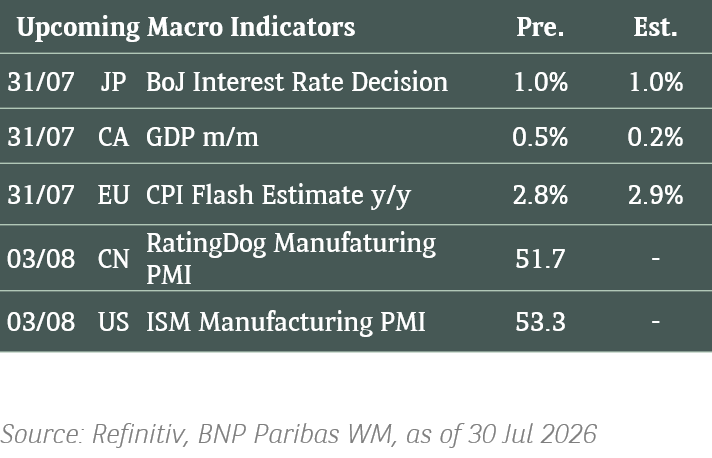

The US 10y Treasury yield inched up to 4.3%, its highest level in four months, as the market prepares for a busy week of economic data. Key releases include GDP growth estimates, PCE inflation, and payroll data, which should offer further insights into the strength of the US economy, just ahead of the presidential election and the Fed monetary policy decision next week. Market currently expects the Fed to adopt a more cautious approach in the easing cycle, and is fully pricing in a 25bps cut in interest rates for the November FOMC, similar to our forecast. Earnings will also be in focus this week as five of the "Magnificent Seven" megacaps set to report their quarterly results.

Main Upcoming Macro Indicators

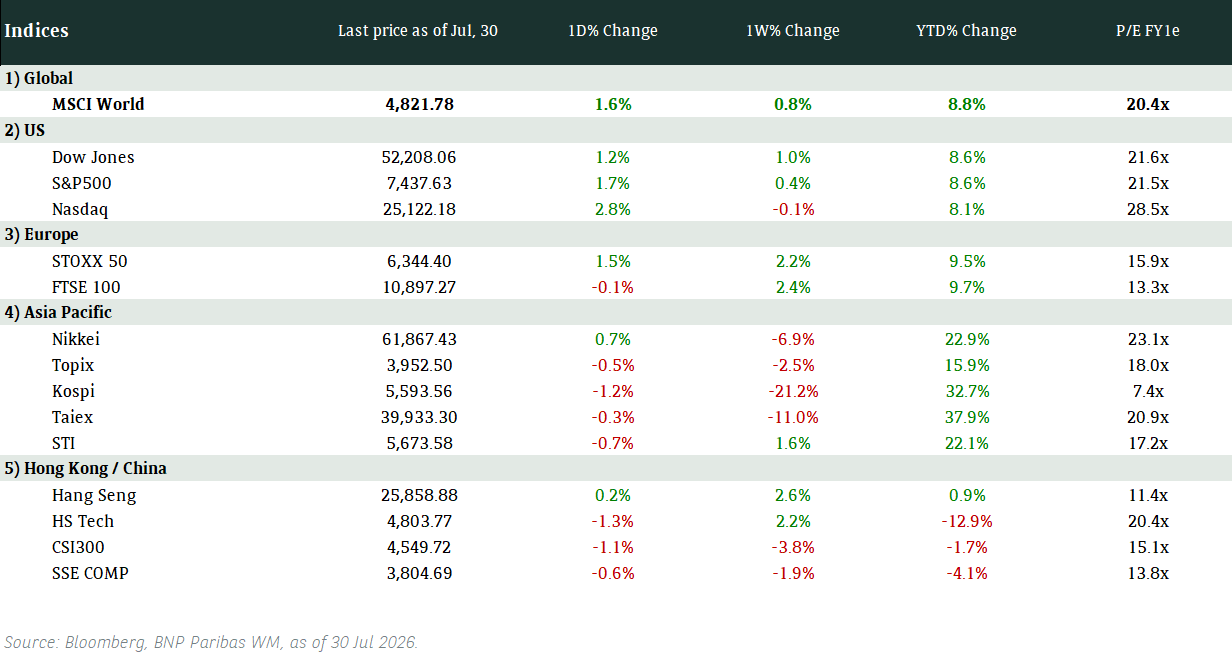

Equity Market Updates

US EQUITIES

US stocks closed mostly higher, with Dow soaring over 273 points as tech giants prepare to share their quarterly financial statements.

EUROPE EQUITIES

EU equities closed higher on Monday ahead of a week full of earnings reports from large European companies.

HK EQUITIES

HKCN equities closed Monday higher although China’s Vice finance minister stating that this round of stimulus will be “quite large” failed to spark significant buying interest.

Apple (AAPL US)

Indonesia had blocked Apple from selling its latest iPhones, saying that the firm has yet to meet local investment requirements.

The iPhone16, launched in September, cannot be marketed domestically as local unit PT Apple Indonesia hasn’t fulfilled the country’s 40% domestic content requirements for smartphones and tablets, the Ministry of Industry said in a statement. The ministry further disclosed that Apple had promised to invest IDR1.7T in local infrastructure and procurement. However, the actual investment amounted to only IDR1.48T.

MARKET CONSENSUS: 39 BUYS, 18 HOLDS, 3 SELLS, AVERAGE TP USD245.02

Xiaomi (1810 HK)

Xiaomi’s Chairman, Lei Jun, announced that the mass production version of the Xiaomi SU7 ultra is now available for pre-order, with a launch event scheduled for tomorrow (29th Oct) at 7pm.

Lei revealed that this version of the car embodies peak performance, technology, and control, capable of racing on tracks and navigating through city streets, and that it is his dream car.

MARKET CONSENSUS: 38 BUYS, 2 HOLDS, 1 SELL, AVERAGE TP HKD24.62

Eli Lily (LLY US)

Eli Lilly expects to start selling its highly popular weight-loss drug in Hong Kong as early as the end of this year, potentially making it the first of its kind to become available in the China region. The market view this as a positive development for the firm.

Its rival, Novo Nordisk, is already selling its diabetes drug in Hong Kong and mainland China, but its weight-loss version hasn’t been made available.

MARKET CONSENSUS: 26 BUYS, 6 HOLDS, 1 SELL, AVERAGE TP USD1013.92

McDonald’s (MCD US)

McDonald’s says Quarter Pounders will return to menus at all restaurants this week after ruling out beef patties as the source of a multistate E.coli outbreak that has sickened dozens and left one dead.

“The issue appears to be contained to a particular ingredient and geography, and we remain very confident that any contaminated products has been removed from our supply chain,” the firm said.

McDonald’s is expected to announce quarterly results on 29 Oct and this incident potentially put the firm in focus.

MARKET CONSENSUS: 26 BUYS, 14 HOLDS, 1 SELL, AVERAGE TP USD320.82

Alphabet (GOOGL US)

Google is set to roll out its AI Overviews feature in Search to over 100 countries worldwide this week following a successful launch in May, the company announced on Monday.

The launch will empower AI Overviews to serve 1B users worldwide each month, allowing them to find results faster by providing AI-generated snapshots "with key information and links to dig deeper," the firm added.

MARKET CONSENSUS: 58 BUYS, 12 HOLDS, AVERAGE TP USD202.85

Earnings Announcements

US Market

Alphabet, AMD, EA, Visa, Pfizer, Phillips 66

European Market

BP, adidas, Banco Santander

HK - China Market

HSBC

Global Indices Changes (%)

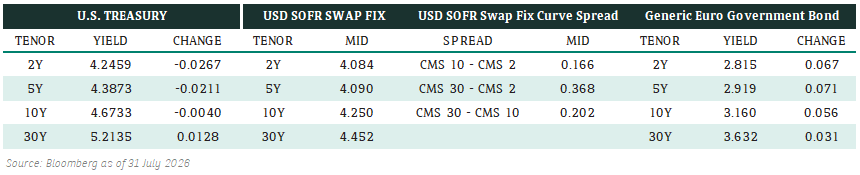

Fixed Income Market Updates

The 10-year Treasury yield is expected to rise in the upcoming week, influenced by a series of macroeconomic data releases. This presents a good opportunity to buy long-dated IG bonds at dips to secure yield. Additionally, interest rate volatility may remain elevated ahead of the US election, allowing investors to explore a wider range of rate products for yield enhancement.

European AT1

The AT1 market opened 5 basis points lower, primarily influenced by movements in the US Treasury and UK Bund markets. Flows from the Asian market were balanced across private wealth and asset management accounts. However, European hedge funds engaged in selling AT1s, particularly those with longer call dates and recent issuances. Two new perpetual non-callable 7-year AT1 deals were announced, one each from Belfius Bank and Skandinaviska Enskilda Banken.

ASIA INVESTMENT GRADE (IG)

The China IG market had a quiet start, with benchmark names widening by an average of 1 basis point. Trade flows leaned towards selling long-dated beta names while favoring the purchase of 2–5-year bonds for carry. The Huarong curve experienced profit-taking from institutional accounts but was well absorbed at reasonable levels. Outside of China, the Korean IG market saw strong interest in Hyundai Motor, particularly from onshore retail investors for 3–5 year tenors. The LG Energy Solution curve remained relatively stable, with institutional accounts primarily selling following its 3Q results.

ASIA HIGH YIELD (HY)

Prices In the China HY market, property benchmarks like Longfor and Future Land traded flat to 0.7 points higher. The Macau gaming sector experienced two-way flows between institutional and private wealth accounts. Conversely, Indian HY had muted trading activity, with most movements driven solely by rates. Many investors remained on the sidelines, unmotivated to buy on dips.

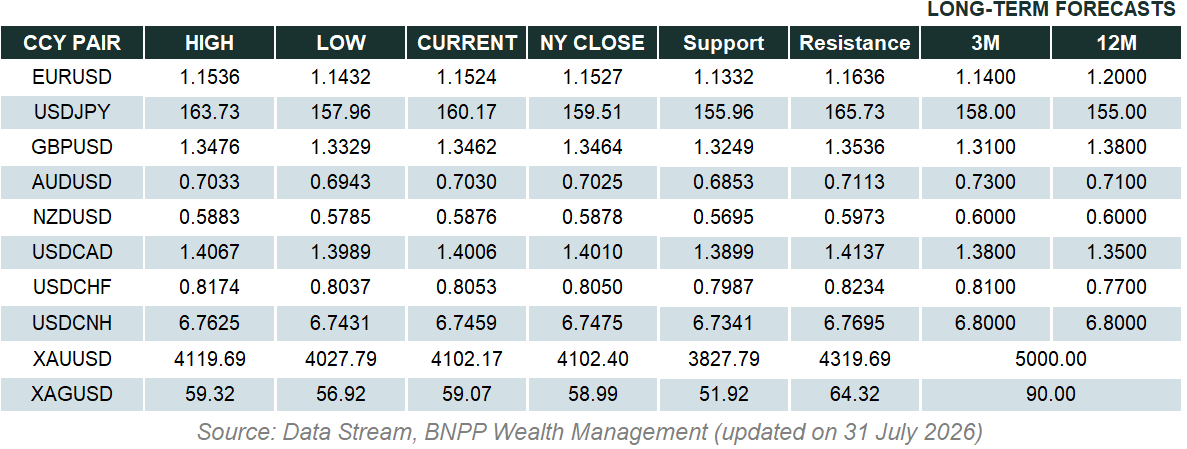

Forex Market Updates

The US Dollar remained strong and is heading for the largest monthly rise in two years on market expectations of delayed interest rate cuts.

USD

The US Dollar is headed for its largest monthly rise in two and a half years against a basket of major currencies, driven by signs of strength in the US economy. Bets on Donald Trump winning the presidency have also lifted US yields (as mentioned earlier) in anticipation of policies that could delay interest rate cuts. Analysts argued that markets are increasingly pricing in a Republican sweep, with Trump winning the presidency and his party controlling both chambers of Congress.

The Dollar Index is likely to maintain upside momentum above 103.50 ahead of Friday’s key NFP data.

JPY

The Japanese Yen hit three-month lows against the dollar on Monday, remaining under pressure as an election loss by Japan's ruling coalition raises political and monetary policy uncertainty. A period of wrangling to secure a coalition is likely after Japan's Liberal Democratic Party and its junior partner Komeito won 215 lower house seats to fall short of the 233 majority.

The Yen's near term outlook remains bearish, with 155 being the next potential target.

GBP

The British Pound post was on track for its biggest monthly fall since September 2023 against the dollar while being roughly unchanged versus the euro with markets focused on major central banks' monetary easing paths. Bank of England officials showed last week a more cautious approach to policy easing, with Governor Bailey arguing inflation is being pushed down by annual base effects. Interest rate-setter Catherine Mann, meanwhile, said the cooling of price growth still had "a long way to go" before hitting the central bank's 2% target.

Sterling could see some consolidation between 1.2900 and 1.3100 heading into Wednesday’s UK Budget.

XAU

Gold record rally took a breather on Monday, as US Treasury yields and dollar gained the upper hand, while investors awaits key US economic data mentioned earlier and how it will affect the Federal Reserve's interest rate outlook. With the Nov. 5 US election approaching, Vice President Kamala Harris and former President Donald Trump are caught in a knife-edge battle to win over some of the more competitive states.

The precious metal is likely to remain well-supported above 2700 in the near term.