Market Daily

Macro Update:

Market lowers expectation for cuts

The market remains cautious following comments from the Fed Chair Jerome Powell last week, on holding off rate cuts due to strong economic growth and a robust labor market. Market is now pricing in a 62% probability of a 25bps reduction in rate for the upcoming December FOMC, a significant drop from 86% at the start of last week. Meanwhile, the US 10Y treasury yield held around the 4.42% level, on lower expectations for a Fed rate cuts in 2025 and potential inflationary pressures from Trump's proposed policies. Our 12 month target for the US 10y yield has been revised up slightly to 4.25% following the US election results.

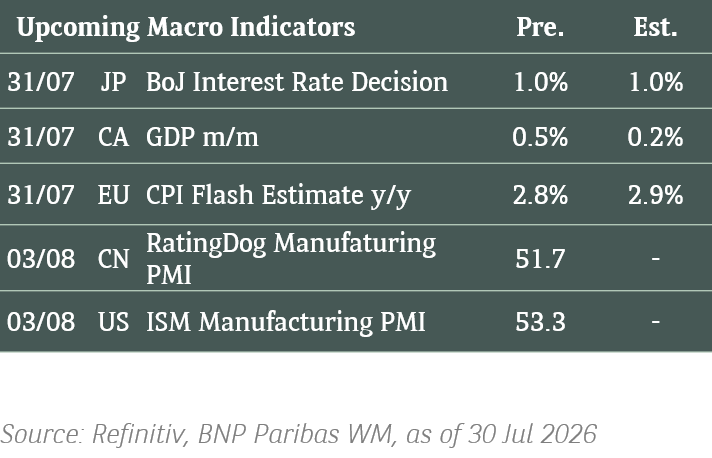

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks closed higher on Monday, recovering some of the prior session’s losses, as investors anticipate AI leader Nvidia’s earnings announcement this week.

EUROPE EQUITIES

Stocks in Europe traded largely flat on Monday, weighed by declines in real estate stocks, while investors digest speeches from ECB policymakers to assess rate cut prospects.

HK EQUITIES

Hong Kong stocks rebounded from a 6-day decline on Monday as Chinese banks rose following regulators urging companies with share prices lower than book values to improve their efficiency and performance.

Tesla (TSLA US)

Shares of Tesla jumped on Monday after a report stating that president-elect Donald Trump is seeking to create a federal framework for self-driving cars.

Currently, licenses for self-driving cars are issued for the most part by states. A federal framework has the potential to make them easier to obtain, while also making it possible for autonomous cars to drive across US state lines.

Further developments on this topic is likely to support Tesla’s share price in the near term, as it would be a significant tailwind for Tesla’s autonomous and AI strategies.

MARKET CONSENSUS: 27 BUYS, 18 HOLDS, 16 SELLS, AVERAGE TP USD243.77

AstraZeneca (AZN LN)

AstraZeneca announced on Monday that its treatment for patients with unresectable non-small cell lung cancer, Tagrisso, gained key recommendation for approval in the European Union.

The recommendation was made by the European Medicines Agency's Committee for Medicinal Products for Human Use based on results from the Laura phase 3 trial, in which Tagrisso helped reduce the risk of disease progression or death by 84% compared with placebo.

This development opens up a significant market for the drug, which could support AstraZeneca’s share price in the near term.

MARKET CONSENSUS: 24 BUYS, 6 HOLDS, AVERAGE TP GBP13645.76

Daiichi Sankyo (4568 JP)

Japanese pharmaceutical giant Daiichi Sankyo is reportedly gearing up to start the exportation of its vaccines to global markets, initially targeting Southeast Asia by 2030.

If successful, this move has the potential to open up significant markets for Daiichi’s products, which would support the company’s bottom line and thus its share price.

With the support of the government, Daiichi Sankyo also reportedly plans to finalize the construction of production facilities designed to manufacture vaccines specifically during pandemic situations by 2028.

MARKET CONSENSUS: 17 BUYS, 2 HOLDS, AVERAGE TP JPY6387.5

Xiaomi (1810 HK)

Xiaomi on Monday reported a solid beats in its 3Q24 results with revenue at RMB92.5 vs. RMB90.3B expected, while adjusted net income was at RMB6.25B vs. RMB5.91B expected. The results was largely driven by strong sales across the company’s business segments, including smartphones, internet services, and surprisingly electric vehicles.

Xiaomi has witnessed robust sales in its new EV business since it launched its first car in late March, with deliveries of its Xiaomi SU7 series exceeding the delivery target of 100,000 units.

This is a positive sign that Xiaomi’s venture into electric vehicles is progressing smoothly, likely supporting its share price in the near to medium term.

MARKET CONSENSUS: 39 BUYS, 2 HOLDS, 1 SELL, AVERAGE TP HKD29.29

Alibaba (9988 HK)

Alibaba is reportedly on Monday planning to raise USD5B through USD and offshore RMB bonds in what would become Asia Pacific’s largest corporate bond deal so far in 2024.

The current dollar tranche would consist of a 5.5-year, 10.5-year and 30-year dollar bond, while the company is also working on yuan bonds with a 3.5-year, 5-year, 10-year and 20-year span.

Alibaba reportedly aims to use the proceeds for corporate purposes, including debt repayment and share buybacks. These could potentially support share price in the near term.

MARKET CONSENSUS: 40 BUYS, 3 HOLDS, AVERAGE TP HKD120.12

Earnings Announcements

US Market

Walmart

European Market

Thyssenkrupp

HK - China Market

XPeng, Tongcheng Travel, ZTO Express

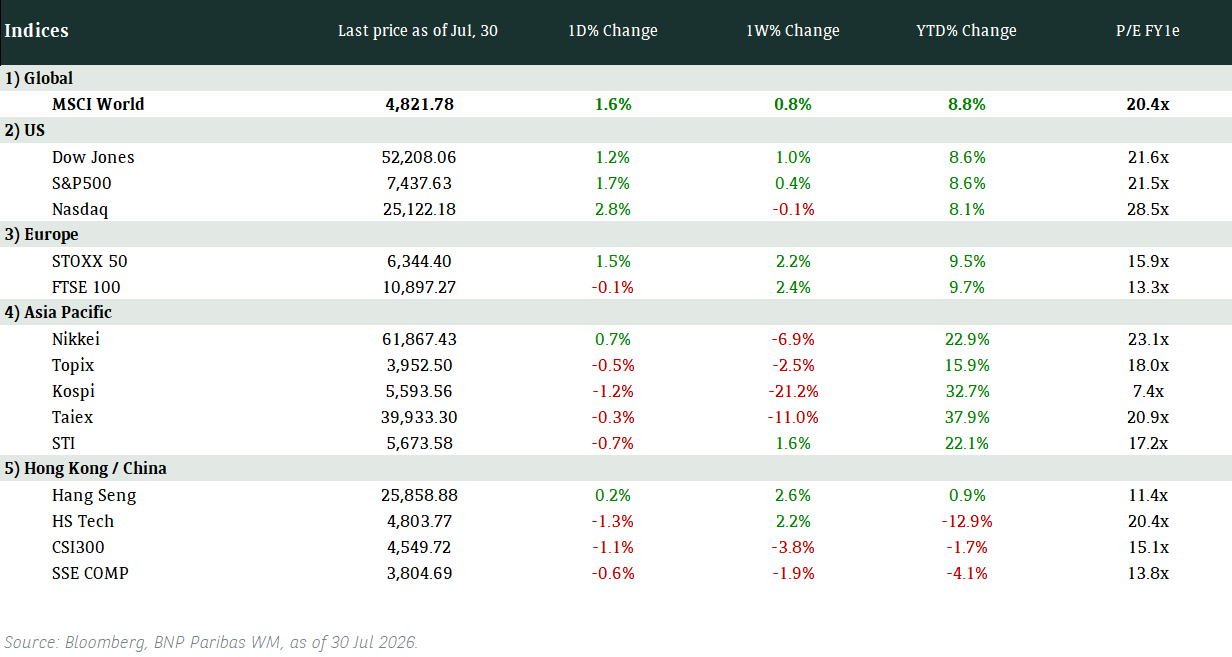

Global Indices Changes (%)

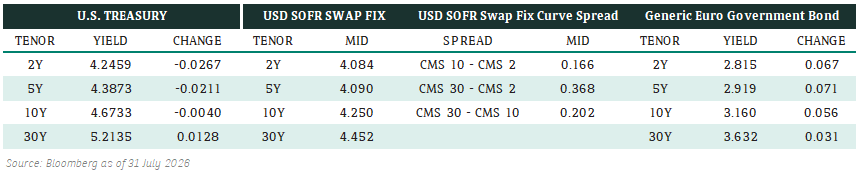

Fixed Income Market Updates

Recent increases in Treasury yields and wider credit spreads, driven by hawkish Fed commentary and reflation concerns, have led to a price correction in the long end of the curve. The market will remain technically fragile until rates stabilise. We believe this presents a favourable opportunity to gradually extend duration.

EUROPEAN AT1

The AT1 market opened quietly after a lackluster session last Friday, which followed the digestion of four new issues over the past week. Recent deals have driven significant activity across AT1 curves, with institutional accounts being the most active participants, while private bank accounts remained relatively subdued. The technical landscape for AT1 bonds has become more fragile, necessitating stability in rates and yield hunting to counterbalance selling pressures.

ASIA INVESTMENT GRADE (IG)

In the China IG market, the opening was soft, with spreads widening by 2 to 5 basis points due to risk-off sentiment that emerged last Thursday. Following Alibaba's announcement of a US$5 billion new issue, the company’s long-dated bonds widened by 6 to 7 basis points, while the broader technology sector saw spreads increase by 3 to 4 basis points. Outside of China, Korean IG experienced selling from private banks and global institutional accounts, particularly on high-beta names like LG Energy Solution and SK Hynix. In Thailand, the oil sector faced selling pressures, with spreads widening by 5 to 10 basis points.

ASIA HIGH YIELD (HY)

Within China's HY market, positive sentiment from property equities did not translate into bond performance, as private wealth accounts continued to exhibit marginal selling. The Macau gaming sector declined by 0.25 points due to small-scale selling. Meanwhile, the Indian HY market traded on a weaker tone, with institutional accounts selling recent new issues, resulting in levels dropping by 0.125 to 0.25 points. Notably, Piramal Capital fell by 0.75 points amid whistleblower allegations.

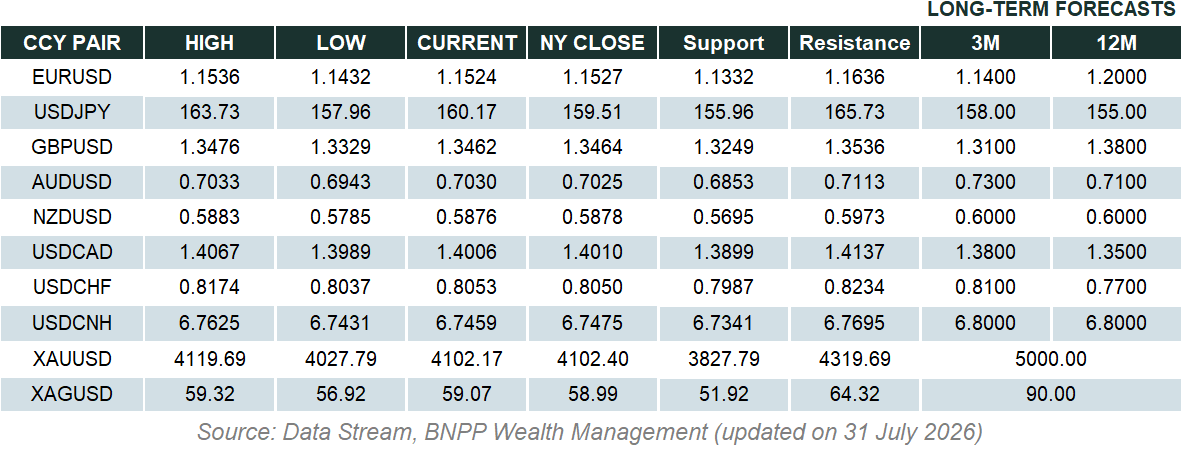

Forex Market Updates

The US Dollar weakened on a relatively quiet Monday as markets awaited key Trump economic and fiscal policy appointments.

USD

The US Dollar slumped against a basket of other major currencies at the start of the week as markets continued to take profit on Trump trades and USD long positioning established over the previous two weeks whilst awaiting key Trump appointments in the areas of economic and fiscal policy. On the central bank front, weekend comments by prominent Fed officials also weighed on the greenback, with policymaker Collins saying that she was not taking a possible December rate cut off the table and that some amount of easing is appropriate over time, while policymaker Goolsbee sees rates softening along the lines of the dot plot.

The Dollar Index could see more losses moving forward, with 105.70 a realistic target for USD bears.

JPY

The Japanese Yen returned a small portion of Friday’s strong gains yesterday after BoJ Governor Ueda said that Japan’s economy is progressing towards sustained wages-driven inflation and warned against keeping interest rates too low lest inflation accelerates more than expected. In a sign the BoJ was likely to push rates up again soon, Ueda added that the central bank wouldn’t necessarily wait for external risks, such as uncertainty over Trump’s economic policies, to completely subside before hiking rates again.

USDJPY could see some near term downside towards technical support around 152.60.

EUR

The Euro extended its recovery from 13-month lows against the USD on Monday despite comments by two top ECB officials signaling their worries about the negative impact of Trump’s proposed tariffs on the Eurozone. Policymakers De Guindos and Nagel both put the emphasis on the hit that new trade restrictions would have on the single market economy while appearing more sanguine on the outlook for inflation, which has been trending lower after a two-year surge. Nagel added that if geoeconomic fragmentation does lead to greater inflationary pressures, the ECB and other central banks could keep it at bay via higher interest rates.

While the common currency’s near term outlook remains bearish, technical support at 1.0500 looks poised to hold for now.

XAU

Gold prices rose for the first time in seven days in the face of a broadly weaker USD as well as heightened uncertainty over the Russia-Ukraine conflict. Outgoing US President Biden’s decision to authorize the use of US long-range missiles for Ukraine to strike deep into Russian territory rekindled safe haven demand for the precious metal, helping gold prices close above the 2600 handle for the first time in a week.

The precious metal looks poised to remain supported above 2535 for the time being.