Market Daily

Macro Update:

Markets mixed following heightened geopolitical tensions

Tuesday started with a general flight to safety as investors sought safer assets amid growing concerns over an escalation in the Ukraine-Russia conflict. Tensions intensified as Russian President Vladimir Putin revised nuclear doctrine, lowering the threshold for nuclear response amid US-enabled Ukrainian missile strikes inside Russia. Market participants flocked to the dollar, gold and treasury, albeit geopolitical concerns were quickly brushed aside, with equities gaining slightly in anticipation of Nvidia's earnings report. Crucially, geopolitical tensions seldom have a lasting impact on markets, hence pullbacks should be treated as an opportunity for entry.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US equities ended higher on Tuesday as Walmart shares climb after it raised its annual forecasts.

All eyes are now on Nvidia’s results, which are to release after the US market closes today.

EUROPE EQUITIES

Shares in Europe were lower on Tuesday as geopolitical tensions subdued sentiment.

HK EQUITIES

Hong Kong stocks rose for a second day on Tuesday on optimism that China will ramp up support for the city’s financial market.

Walmart (WMT US)

Shares of Walmart rose on Tuesday after the US consumer giant boosted its outlook for the year on strong demand from consumers searching for value, reassuring investors of a still-healthy business amid a bumpy macro backdrop and potentially supporting share price in the near to medium term.

The company now sees full-year adjusted EPS to be between USD2.42 to USD2.47 from USD2.35 to USD2.43 previously.

Walmart also posted solid FY3Q25 results with revenue at USD169.6B vs. USD167.5B expected, while adjusted EPS was at USD0.58 vs. USD0.53 expected.

MARKET CONSENSUS: 43 BUYS, 2 HOLDS, 1 SELL, AVERAGE TP USD91.86

SMCI (SMCI US)

Shares of SMCI surged on Tuesday after the company announced that it had appointed BDO as its new auditing firm and unveiled a strategy to avoid being removed from the NASDAQ stock exchange listings. Further developments in this topic is likely to provide further upside to share price going forward.

SMCI has struggled recently after the company’s previous auditor, Ernst & Young, resigned at the end of October, citing concerns regarding the firm's "commitment to integrity and ethical values,“ which forced the company to delay its quarterly filings.

MARKET CONSENSUS: 3 BUYS, 7 HOLDS, 2 SELLS, AVERAGE TP USD34.67

Meta Platforms (META US)

Meta is reportedly setting up a new AI-focused product group to develop innovative tools, such as chatbots for WhatsApp and Messenger, designed to enhance customer interaction and drive business transactions. This is a positive development for the company, providing evidence of progress towards AI monetisation.

The AI product division that will serve the 200M businesses on Meta's platforms, will be led by Clara Shih, the former CEO of Salesforce AI.

MARKET CONSENSUS: 67 BUYS, 9 HOLDS, 3 SELLS, AVERAGE TP USD651.78

Thyssenkrupp (TKA GY)

Shares of Thyssenkrupp surged on Tuesday after it expects a swing to profitability in the current fiscal year, indicating that its turnaround plan which includes restructuring the company’s ailing steel division is making progress. If things go as expected, Thyssenkrupp’s share price is likely to find support in the near to medium term.

The German manufacturer specifically sees net income of at least EUR100M in the year through next September, significantly up from a net loss of EUR1.4B last fiscal year. It is also projecting a rise in operating earnings, although cash burn will increase due to higher investments and restructuring costs.

MARKET CONSENSUS: 3 BUYS, 6 HOLDS, 2 SELLS, AVERAGE TP EUR4.79

XPeng (9868 HK)

XPeng on Tuesday revealed a solid beat in its 3Q24 revenue at RMB10.1B vs. RMB9.9B expected, driven by robust vehicle deliveries. Adjusted net loss was also less than expected at RMB1.53B vs. RMB1.64B expected.

Adding to the good news was XPeng’s better-than-expected 4Q24 revenue forecast thanks to new car models and an improving domestic market.

If this growth trend continues, we might see further upside to the company’s share price.

MARKET CONSENSUS: 30 BUYS, 5 HOLDS, 1 SELL, AVERAGE TP HKD57.24

Earnings Announcements

US Market

Target, Snowflake Inc., Palo Alto, Nvidia

European Market

British Land

HK - China Market

Nio, Kuaishou

Global Indices Changes (%)

Fixed Income Market Updates

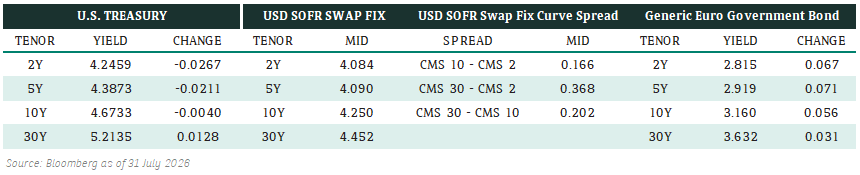

We do not see a strong fundamental case for US Treasury to further sell-off. We expect the yield will eventually come down to our CIO 12-month target of 4.25% as market shifts its focus back to fundamental of US economy. At this juncture, we remain comfortable with 5-10 years good quality IG bonds as risk-reward is favourable.

EUROPEAN AT1

European AT1 had a soft day. Most bond prices were 0.125-0.25 points lower as market took time to digest the recent round of new issuance supply. The Trump inflation theme is also not helping the sector and long call date AT1 bonds continue to be under pressure. Having said that, we remain comfortable with European bank credit fundamentals and we would be a buyer for AT1 bonds if prices further correct.

ASIA INVESTMENT GRADE (IG)

It was a quiet day for Asia IG and the spotlight was Alibaba’s new bond issuance announcement. China tech space was largely stable with credit spread slightly tighter. Outside of China, we saw mixed market flow with some selling in longer dated 5-10 years bond as we approach year end. Overall, we expect Asia IG to stay quiet as we approach year-end.

ASIA HIGH YIELD (HY)

Asia HY market tone was generally weak. India HY continue its weakness as more investors took profit before year-end. We saw more selling in the longer tenor India HY bonds, particularly from hedge funds. As a result, the space was generally 0.125-0.25 points lower. We expect the weakness for India HY to stay as the sector valuation is not cheap, in our view.

Forex Market Updates

The US Dollar held steady against a basket of other major currencies as geopolitical tensions sustained safe haven demand, with maarkets awaiting US inflation data and fiscal policy signals for future direction.

USD

The US Dollar remained steady yesterday as geopolitical tensions sustained demand for safe haven assets. The Dollar Index held around four-day lows, reflecting cautious investor sentiment following Russia’s nuclear doctrine update, with analysts noting the market's prior complacency toward geopolitical risks. The greenback has gained over 3% this month but has retreated from one-year highs as markets reassess Fed rate cut expectations. Markets are currently awaiting inflation data and signals on US fiscal policy under the incoming Trump administration, which is likely to influence the USD’s trajectory moving forward.

The Dollar Index should remain well-supported above the 105.00 handle in the near term.

GBP

The British Pound was little changed on Tuesday against the USD while hitting multi-week lows against the Yen and Swiss Franc as geopolitical tensions spurred demand for safe haven currencies. Analysts expect UK inflation data on Wednesday to guide the BoE's monetary path, with a gradual approach to rate cuts anticipated amid forecasts suggesting core inflation may slow to 4.3%. Elsewhere, BoE official Greene said UK services inflation and wage growth are still too high and reinforced her argument for cautious interest rate cuts.

GBPUSD could test its next support level of around 1.2600 moving forward.

CAD

The Canadian Dollar strengthened against its US peer on Tuesday as Canadian inflation rose to 2% in October, exceeding forecasts of 1.9%. Core inflation also increased, prompting markets to scale back expectations of a large BoC rate cut next month. Meanwhile, softer oil prices capped CAD gains. Markets are now turning their attention to the upcoming Canadian Retail Sales figures at the end of this week and next week's GDP data for additional cues.

USDCAD could continue to face near term pressure, with immediate technical support around 1.3860.

XAU

Gold prices climbed to a one-week high, gaining 0.9%, as escalating Russia-Ukraine tensions spurred safe haven demand. The recent rebound, driven by geopolitical risks and investor caution, follows a dip to two-month lows last week. A weaker USD also supported bullion, with analysts pointing to central bank purchases and heightened economic uncertainty as key factors likely to bolster the allutre of the precious metal moving forward.

The precious metal looks poised for more gains towards near term resistance around 2685.