Market Daily

Macro Update:

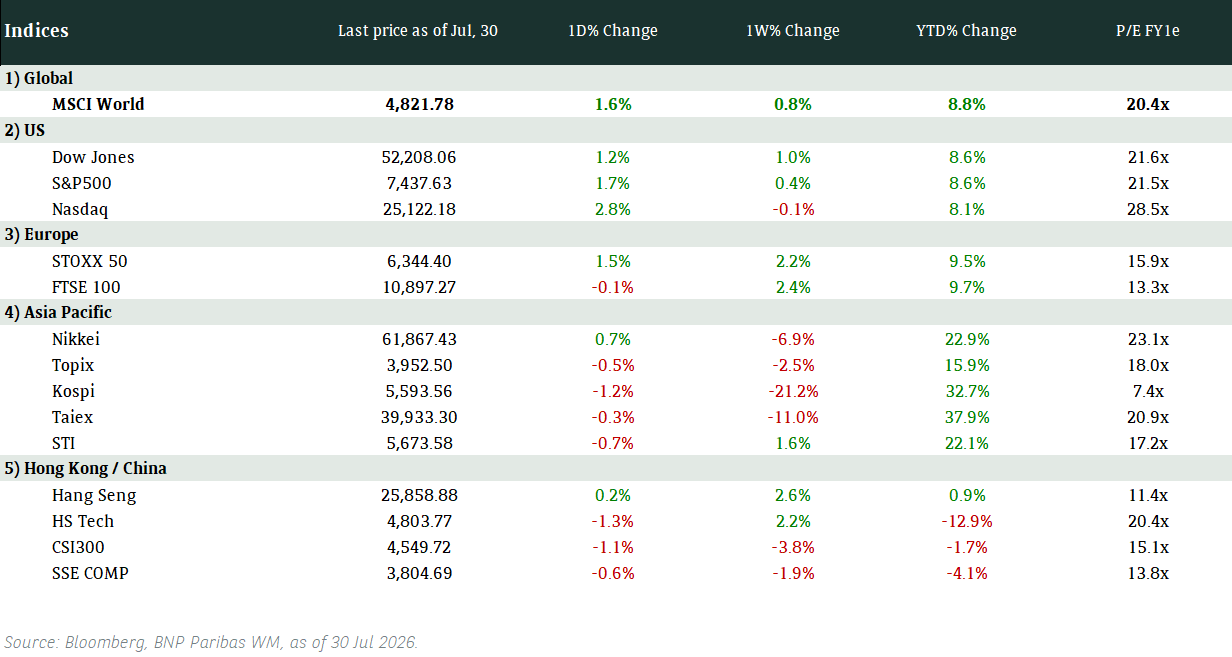

Dow closes at record high

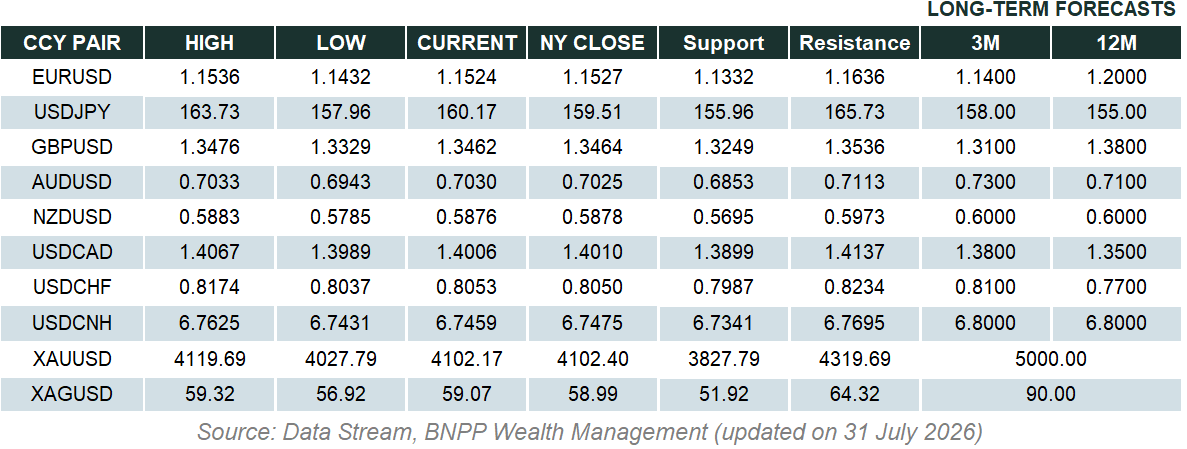

The Dow Jones Industrial Average Index gained 1% to set a new closing high last Friday. Non-tech sectors have been catching up after the elections. We continue to be positive on US equities and favour financials, selected cyclicals and small-mid caps. The USD Index briefly hit above 107. We expect some consolidation in USD in the short term with 3-month target at 105.5. We continue to expect further USD strengthening in the medium term with 12-month target at 108.8.

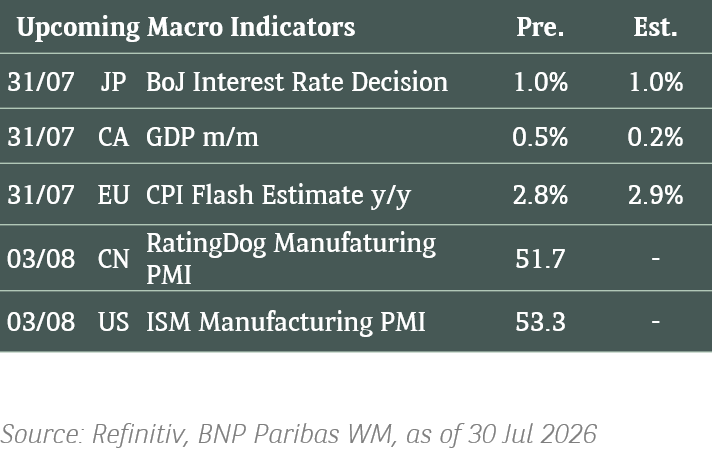

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks closed higher on Friday as robust economic data boosted investor sentiment. This positive momentum is likely to continue as we enter the tail end of 2024.

EUROPE EQUITIES

European equities surged on Friday, led by real estate companies, while easing geopolitical tensions also relieved some of the week’s selling pressure.

HK EQUITIES

Stocks in Hong Kong fell on Friday as downbeat earnings announcements dampened sentiment and reignited concerns on China’s growth outlook.

Amazon (AMZN US)

The European Union is reportedly set to investigate Amazon in 2025 for allegedly favouring its own in-house branded products.

The probe will focus on whether Amazon’s marketplace gives an unfair advantage to its own products over those sold by third-party vendors, and if Amazon is found to be in violation of the DMA, it could be hit with a fine amounting to 10% of its global annual turnover.

The potential fine could materially impact Amazon’s bottom line. Thus, further developments on the probe is likely to inject volatility to the company’s share price going forward.

MARKET CONSENSUS: 77 BUYS, 5 HOLDS, AVERAGE TP USD233.59

UPS (UPS US)

The US Securities and Exchange Commission (SEC) announced on Friday that it reached a USD45M settlement with UPS as the company agreed to pay a penalty for "improperly valuing" its business unit UPS Freight.

The SEC had charged UPS over its failure to follow generally accepted accounting principles (GAAP) in valuing "one of its worst performing businesses." The agency stressed that UPS used an outside consultant's valuation of Freight instead of its own; despite knowing it was three times as much as UPS had determined.

MARKET CONSENSUS: 18 BUYS, 13 HOLDS, 3 SELLS, AVERAGE TP USD149.47

Honeywell (HON US)

Honeywell shares traded higher on Friday after the company announced that it is selling its Personal Protective Equipment (PPE) business for USD1.33B, further streamlining its business and potentially boosting bottom line performance going forward.

The company’s PPE business sale is expected to close in the first half of 2025 and comes after the company announced last month that it also plans to spin off its Advanced Materials business into an independent, U.S. publicly traded company, which is targeted to be completed by the end of 2025 or early 2026.

MARKET CONSENSUS: 12 BUYS, 13 HOLDS, 1 SELL, AVERAGE TP USD237.1

Thales (HO FP)

Shares of Thales slipped on Friday after French and British authorities launched an investigation into suspected arms-sales-related bribery and corruption at the aerospace and defense group.

While details of the allegations were not disclosed, further developments on this topic may inject volatility to the company’s share price in the near term as any notable charges could potentially derail its strategic plan going forward.

MARKET CONSENSUS: 12 BUYS, 8 HOLDS, 1 SELL, AVERAGE TP EUR174.84

Midea Group (300 HK)

The Hang Seng Indexes Company announced on Friday that it is adding Midea Group to the Hang Seng TECH index while WB-SW will be removed. All changes will be implemented after market close on 6 December 2024 and will take effect on 9 December 2024.

This addition is likely a positive for Midea’s share price as funds that benchmark its performance to the Hang Seng TECH index will now have to buy Midea as well.

MARKET CONSENSUS: 6 BUYS, AVERAGE TP HKD96.23

Earnings Announcements

US Market

-

European Market

-

HK - China Market

Want Want

Global Indices Changes (%)

Fixed Income Market Updates

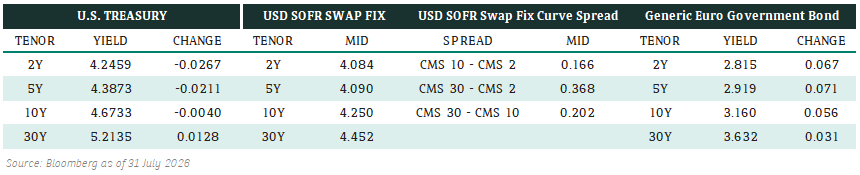

This morning US Treasury yields are lower driven by Scott Bessent's nomination to Treasury Secretary. We could see more volatility as the shape of Trump 2.0 gains clarity over the next several weeks. With the Treasury yield curve flattening at the moment, we like Tier-2 US banks that provide decent pick-up over comparable seniors bonds.

EUROPEAN ATT

Overall tone in the European AT1 space is cautious with weak technicals. Euro denomiated AT1s underperformed as of Friday close. Technicals and liquidity slowed as we approach thanksgiving and December. However, some accounts were happy to take the other side of recent weakness. There is going to be very good dislocations going into December as those street technicals continue to dominate.

ASIA INVESTMENT GRADE (IG)

In China IG space, spreads generally traded wider last week. Appetite for duration was weak with better interest in long duration bonds. China IG traded wider with China tech 2-9bps wider. Korea was rather benign for the most part, +2/-7 bps on the week. Onshore accounts were better buyer on the 3-5Y part of the curve. Overall, we still prefer 5-10 year Investment Grade bonds in this current rates environment.

ASIA HIGH YIELD (HY)

Quieter day with the focus again on Adani complex. Overall high yield bonds continued to drop during US hours. Combo of S&P rating actions and reports of more probes continued to weigh on sentiment. Some real money started to dipping toes but dealers fought hard to make sales and the prints kept resetting lower. Apart from Adani, India HY overall took a breather with some funds adding names in renewables. Other Asia HY also traded firm with flow skew to better buying in gaming.

Forex Market Updates

The US Dollar hit a two-year high as investors lowered expectations of significant interest rate cuts, as well as safe-haven buying on escalating geopolitical risk in Ukraine.

USD

The US Dollar rose to a two-year high, and its third straight weekly advance. Investors have scaled back expectations for the path of interest rate cuts from the Federal Reserve recently, currently pricing in a 52.7% chance of a 25 basis point cut at the Fed's December meeting, down from 69.5% a month ago, according to CME's FedWatch Tool. Investors are waiting for Trump to name a Treasury secretary. The Wall Street Journal reported on Thursday that Trump floated the idea of appointing Kevin Warsh, a former member of the Fed's board of governors, to the post, with the understanding that he could later become Fed chair.

USD could see some resistance around the 108.00 level, with some investors taking profit.

GBP

The British Pound tumbled on Friday after data showed British business output in November shrank for the first time in more than a year, and retail sales also fell by much more than expected in October. Sterling hit its lowest on the dollar since May, and was last down 0.56% at $1.2517. If future data continues to show economic weakness, the Bank of England may be forced to cut rates more dramatically than markets currently expect.

While Sterling’s immediate outlook remains bearish, the 1.2500 handle should provide some support for now.

AUD

The Australian Dollar hit a seven-week high on the euro on Friday as the single currency dived amid an escalating war between Russia and Ukraine, while diverging rate outlooks sent the Aussie to a near four-month top on the kiwi. Against the U.S. dollar, the Aussie was flat at $0.6513 and was set for a weekly gain of 0.80%, well off a three-month low of $0.6441. Australian markets have not fully priced in a rate cut from the Reserve Bank of Australia until next July.

The Aussie looks to have found some support at the 0.6440 level but could continue to test it.

XAU

Gold prices breached the $2,700 threshold for the first time in over two weeks on Friday, on track for their biggest weekly gain in nearly two years, as safe-haven demand outweighed dollar strength and lower expectations of a U.S. rate cut next month. Some analysts say that the escalation in the Russia-Ukraine conflict seems like it's expanding to a Russia-U.S. war, and that's definitely boosting short-term safe haven appeal. Bullion gained over 5.7% last week, poised for its best weekly performance since March 2023, when a wave of banking crises roiled global markets and boosted demand for safer assets.

The precious metal could see more near term gains towards previous high of 2790.15.