Market Daily

Macro Update:

Markets Applaud Scott Bessent Nominated as Treasury Secretary

The Dow Jones Industrial Average and Russell 2000 small cap indices hit new highs after the market friendly appointment. Furthermore, the bond market also had a big rally overnight with the 10-year Treasury yield dropping 9 bps to 4.27%. Scott Bessent has advocated for deregulation, lower taxes, and lower fiscal deficits. In addition, he has had a distinguished career as a hedge fund manager including CIO of Soros. The markets have closely tracked this appointment and a highly experienced markets practitioner and historian strengthens the Treasury.

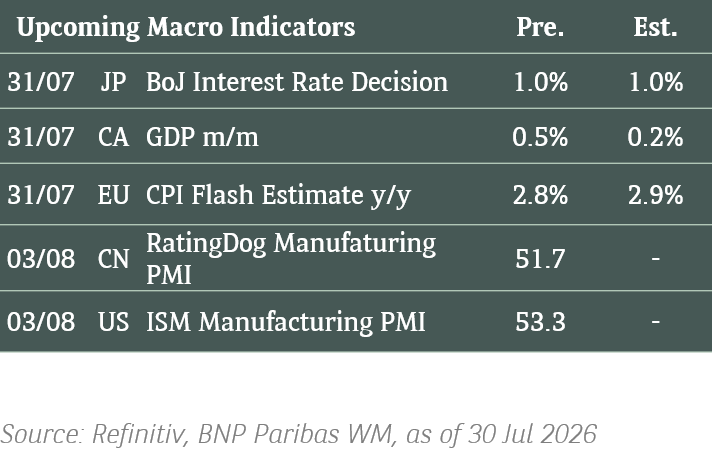

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

Stocks in the US rose on Monday, led by small caps, as investors digest president-elect Trump’s latest cabinet appointments.

The positive mood should be supportive for US equities jumping into 2025.

EUROPE EQUITIES

European equities traded largely flat on Monday, with a slump in energy stocks offsetting the positive developments from the US and the ECB.

HK EQUITIES

Hong Kong stocks retreated for the third session on Monday as concerns linger over US-China relations as well as the Chinese macroeconomic outlook.

Intel (INTC US)

The US government reportedly plans to reduce Intel’s preliminary USD8.5B federal chips grant to less than US8B, adding to the company’s recent slew of headwinds and potentially putting more downward pressure to its share price in the near term.

Intel's grant reduction follows a preliminary agreement this spring, which initially promised nearly USD20B in grants and loans for the company. Intel has strongly advocated for the bill’s approval, where the company was widely regarded as the law’s primary beneficiary. However, its recent business challenges added complexity to the negotiations over its final allocation.

MARKET CONSENSUS: 7 BUYS, 37 HOLDS, 7 SELLS, AVERAGE TP USD24.49

Macy's (M US)

Shares of Macy’s dropped on Monday as it postponed its FY4Q24 earnings release, originally due on Tuesday, until 11 December while it wraps up an investigation into accounting errors.

The company stated that one of its employees had intentionally made erroneous accounting entries to hide approximately USD132M to USD154M of delivery expenses from the fourth quarter of 2021 through the latest quarter, ended 2 November 2024.

This revelation could potentially put more downward pressure to the company’s share price as it has struggled to convince investors about the strength of its business model.

MARKET CONSENSUS: 4 BUYS, 9 HOLDS, 1 SELL, AVERAGE TP USD17.2

Zoom Video Communications (ZM US)

Shares of Zoom rose on Monday after the company raised its forecast for fiscal 2025 revenue, anticipating robust demand for its online video conferencing software as it expands its product portfolio, and clients embrace hybrid working models. Zoom also said it would expand its share repurchase plan by USD1.2B, potentially adding support to the share price going forward.

Zoom also posted an overall beat in its FY3Q25 earnings, with revenue at USD1.18B vs. USD1.16B expected, and adjusted EPS at USD1.38 vs. USD1.31 expected.

MARKET CONSENSUS: 10 BUYS, 21 HOLDS, 2 SELLS, AVERAGE TP USD77.82

Anglo American (AAL LN)

Anglo American announced on Monday that it reached an agreement to sell its portfolio of Australian steelmaking coal mines to US coal miner Peabody Energy for around USD3.8B as the company aims to trim operations.

The agreement comprises of an upfront cash consideration of USD2.1B, a deferred cash consideration of USD725M, as well as up to USD550M in a price-linked earnout and a contingent cash consideration of USD450M linked to the reopening of the Grosvenor mine.

The move was made as Anglo American faces increasing pressure to implement a large-scale restructuring plan it outlined in May 2024 to fend off a nearly USD50B takeover bid from rival BHP. Further realizations of this strategy is likely to swing the company’s share price to the upside going forward..

MARKET CONSENSUS: 10 BUYS, 8 HOLDS, 3 SELLS, AVERAGE TP GBp2454.76

UniCredit (UCG IM)

Italian bank UniCredit on Monday launched a USD10B offer to buy Banco BPM, setting its sights on a smaller domestic peer after negotiations of German Commerzbank stalled.

A potential UniCredit takeover of Banco BPM would create a European banking giant with a combined market capitalization of around EUR72.4B, leapfrogging Intesa Sanpaolo as Italy's No. 1 lender and Spain's Banco Santander as the biggest eurozone bank by market value.

If successful, the deal could strengthen UniCredit’s competitive edge and bolster the bank’s growth outlook going forward..

MARKET CONSENSUS: 16 BUYS, 6 HOLDS, AVERAGE TP EUR46.96

Earnings Announcements

US Market

Analog Devices, Crowdstrike, Workday

European Market

Compass Group

HK - China Market

Chow Tai Fook, China Education Group Holdings

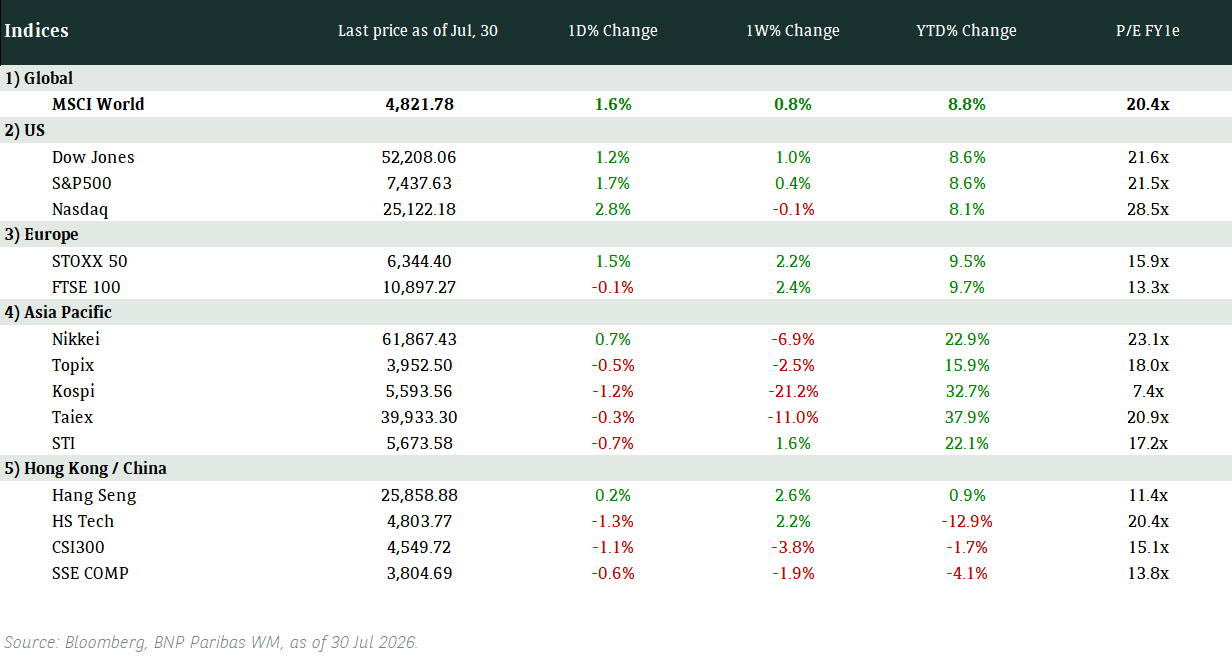

Global Indices Changes (%)

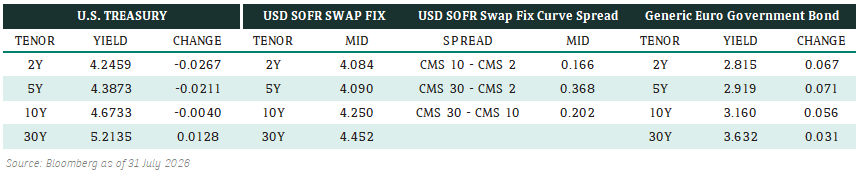

Fixed Income Market Updates

This week will be quiet due to the Thanksgiving holiday. Key US economic data, including PCE and Jobless Claims, may introduce some volatility to Treasury trading but are unlikely to disrupt the recent consolidation trend in the 10-year yield, as Trump-themed trades show signs of fatigue. Bank Tier 2 bonds offer a more favourable risk-reward than AT1 bonds.

EUROPEAN BANK COCO (AT1)

The AT1 market opened 0.125 to 0.375 points higher, providing relief to participants following the appointment of the new US Treasury Secretary. The recent selloff in AT1 bonds appears to be exhausted after several weeks of poor performance, although French AT1s continue to underperform due to ongoing budget concerns. UniCredit announced an all-share takeover of Banco BPM, resulting in unchanged former AT1s and a 0.5 to 1-point increase in the latter.

ASIA INVESTMENT GRADE (IG)

In China, IG spreads widened slightly despite lower US Treasury yields following the Treasury Secretary announcement. The 2- to 5-year tenor remained in demand from local investors, while 5-year benchmark names saw net selling from hedge funds. Meanwhile, Korean IG bonds were mostly unchanged or slightly weaker, with dated bonds and perpetuals trading 0.125 points lower.

ASIA HIGH YIELD (HY)

The China HY market remained relatively quiet, with slight markdowns in bond prices alongside declines in property stock prices. Dalian Wanda outperformed, with its curve rising by 1 point due to private bank accounts buying following a one-year extension for its 2025 bonds. Outside of China, the Adani curve fell by 2 to 6 points due to a lack of US investor interest, while the rest of the Indian HY market continued to drift lower amid concerns over Adani contagion.

Forex Market Updates

The US Dollar finally eased as Treasuries rally on Bessent Treasury nomination, but overall the greenback has risen for eight consecutive weeks due to numerous technical indicators.

USD

The US Dollar backpedaled from two-year highs on Monday, while US Treasury markets cheered Donald Trump's pick of hedge fund manager Scott Bessent for the US Treasury secretary, trusting he will be more fiscally disciplined than investors had been fearing. Traders see Bessent as old Wall Street hand and fiscal conservative. However, he has also openly favoured a strong dollar and supported tariffs, suggesting any pullback in the currency might be fleeting.

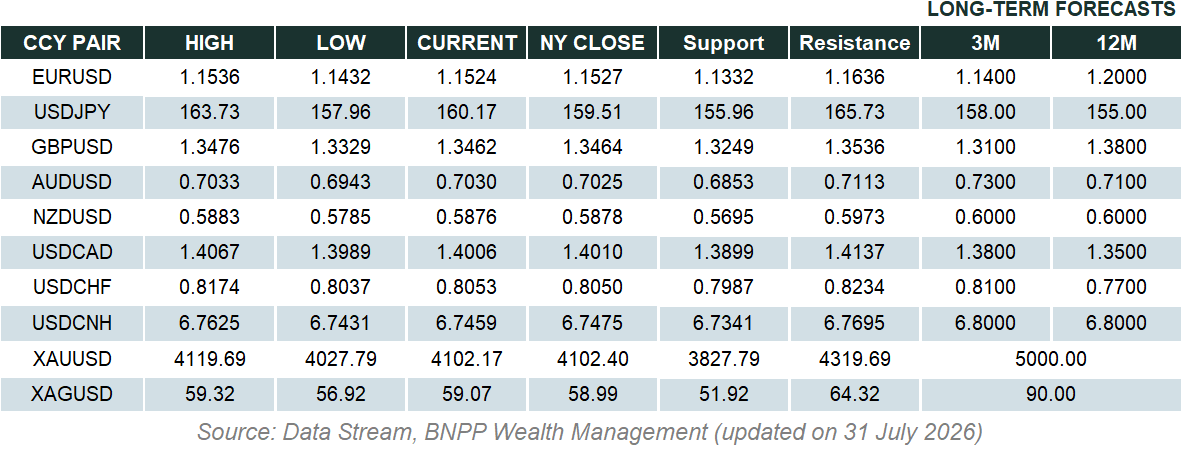

USD should remain supported at the 106 handle in the near term.

GBP

The British Pound was on track to snap a three-day losing streak on Monday, as the dollar's slide after the selection of fund manager Scott Bessent as US Treasury Secretary lent support to most major currency pairs. The pound firmed after slumping to a six-month low on Friday after disappointing British business output and retail sales data raised the prospect of more aggressive interest rate cuts by the Bank of England.

Should Sterling rebound on profit taking, there may be some resistance at 1.2720.

CAD

The Canadian Dollar steadied against its US counterpart on Monday as the bond market's enthusiasm about the choice of US Treasury secretary offset a drop in oil prices and caution ahead of comments by a Bank of Canada policymaker. Bank of Canada Deputy Governor Rhys Mendes is due to speak on Tuesday on monetary policy, the last scheduled appearance by a BoC policymaker before the interest rate decision on 11 Dec. Speculators have raised their bearish bets on the Canadian dollar to the highest level since July, data from the US Commodity Futures Trading Commission showed.

We expect to see USDCAD trading above its technical support level at 1.3825.

XAU

Gold prices plunged over 3% on Monday, breaking a five-session rally to its highest in nearly three weeks, as reports of Israel nearing a ceasefire with Hezbollah, coupled with Trump's nomination of Scott Bessent as the US Treasury Secretary soured the precious metal's safe-haven appeal. Gold prices were primed for a sell-off on buying exhaustion after last week's rally.

The precious metal should find support at 2536 with the current economic and geopolitical developments.