Market Daily

Macro Update:

FOMC minutes points to gradual cuts in rates

FOMC Minutes from the November 7th meeting pointed to gradual cuts in rates with employment near the maximum level as inflation moves closer to 2%. The minutes also revealed less concern about a rapid deterioration in the labour market which prompted the 50 bps cut back in September. We expect one more cut of 25 bps in December and an additional 3 cuts in 2025 ending with a terminal rate of 3.75%.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks ended higher on Tuesday as technology stocks rebounded and investors digest the latest Fed meeting minutes.

EUROPE EQUITIES

Stocks in Europe fell across the board on Tuesday, led by automakers as potential US tariffs dampened investor appetite.

HK EQUITIES

Hong Kong stocks pared early gains to close almost unchanged on Tuesday as investors remain concerned of potential policies that may hinder Chinese exports.

Dell (DELL US)

Shares of Dell closed lower in aftermarket trading on Tuesday as the company issued FY4Q guidance that missed analyst expectations, mostly due to customers delaying the purchase of new hardware and software products. This likely dampened investors’ confidence of the company’s growth prospects going forward. Further downward pressure to share price can be expected in the near term.

Dell on Tuesday also announced FY3Q revenue that missed Wall Street estimates, with the figure coming in at USD24.4B vs. 24.6B expected. The company’s net income was at USD1..54B vs. USD1.46B expected.

MARKET CONSENSUS: 24 BUYS, 3 HOLDS, 1 SELL, AVERAGE TP USD149.28

Rivian (RIVN US)

US EV company Rivian on Tuesday received conditional approval for a loan of up to USD6.6B from the US government to boost its production capability. Rivian stated that the funds will support the construction of its EV plant in Georgia and the production of more midsize vehicles, potentially supporting its growth prospects and thus share price going forward.

The announcement follows Rivian's recent collaboration with Volkswagen on a USD5.8B technology partnership earlier this month.

Rivian plans to build the facility in two phases, with each phase expected to produce up to 200,000 vehicles annually.

MARKET CONSENSUS: 13 BUYS, 12 HOLDS, 2 SELLS, AVERAGE TP USD14.33

Amgen (AMGN US)

Shares of Amgen fell on Tuesday after a mid-stage trial of its weight-loss drug MariTide failed to impress investors, despite still being able to shed up to 20% of patients’ body weight.

Analysts were specifically worried about MariTide’s longer list of side effects while benefits remained in line with peer drugs, such as ones from Novo Nordisk and Eli Lilly.

Further developments in MariTide’s late-stage trial could inject further volatility to Amgen’s share price going forward.

MARKET CONSENSUS: 18 BUYS, 15 HOLDS, 2 SELLS, AVERAGE TP USD336.25

Roche (ROG SW)

Roche said on Tuesday that its phase III lung cancer drug failed to reach its primary goal of overall survival in its final analysis despite prior studies showing positive trends. Failure to bring this drug to market might materially impact Roche’s financial performance going forward.

This statement followed another announcement by the company that it had signed an agreement to acquire clinical-stage biopharmaceutical company Poseida Therapeutics for a total value of up to USD1.5B. The two companies have collaborated since 2022 on developing off-the-shelf CAR-T cell therapies for patients with hematological malignancies.

MARKET CONSENSUS: 14 BUYS, 7 HOLDS, 6 SELLS, AVERAGE TP CHF299

UniCredit (UCG IM)

After UniCredit launched an offer to buy Banco BPM on Monday, the latter said on Tuesday that the former’s EUR10B bid is inadequate, citing undervaluation and oversized risks for current shareholders from UniCredit’s current expansion plans in Germany.

Banco BPM’s Board of Directors also said in a statement that UniCredit’s offer is "unusual" and that the latter's request for a response "in the shortest time possible" could negatively impact Banco BPM's legal autonomy.

Further developments regarding this deal could inject volatility to both banks’ share prices going forward.

MARKET CONSENSUS: 16 BUYS, 6 HOLDS, AVERAGE TP EUR46.96

Earnings Announcements

US Market

-

European Market

EasyJet, Aroundtown SA

HK - China Market

-

Global Indices Changes (%)

Fixed Income Market Updates

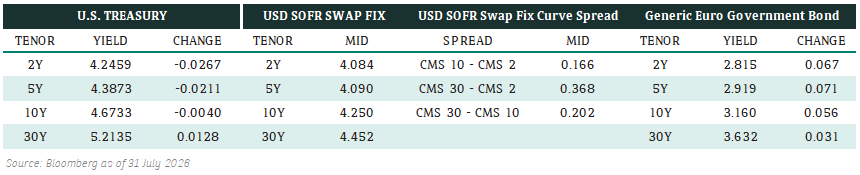

Bond market sentiment has improved after Trump named Scott Bessent as Treasury Secretary. 10-year US Treasury yield has come down to 4.2- 4.3% from 4.5% last week. At this level, we believe the risk-reward with long duration has become less attractive. We suggest to stay more defensive with 5-year IG bonds and look to add longer dated IG bonds when Treasury yield goes higher.

EUROPEAN BANK COCO (AT1)

European AT1 was slightly stronger with bond prices 0.125-0.375 points higher, largely supported by more favorable interest rate movements. The only exception was Commerzbank which was 0.25-0.75 points lower as the market is anticipating a new bond issuance for the bank.

ASIA INVESTMENT GRADE (IG)

For Asia IG, China and HK IG had a tough time, with credit spreads widening 2-5 basis points due to Trump possibly imposing an additional 10% tariffs on China. There was more selling interest for long dated tech names and high-risk non-state-owned enterprise bonds. Overall, we expect the selling pressure for China and HK IG will remain for a while due to trade war headline risk.

ASIA HIGH YIELD (HY)

Asia HY wise, the spotlight was India HY, particularly Adani bonds, which rebounded by 0.5-1 point after days of correction. There was demand for longer-dated bonds Adani bonds despite rating agency Fitch placed the company on a negative watch. Overall, Adani bonds were 0.25-0.75 points higher. We expect Adani complex will stay volatile as the investor confidence has become quite fragile after a few negative headlines this year.

Forex Market Updates

The US Dollar strengthened significantly against the Canadian Dollar, Mexican Peso, and the Chinese Yuan after President-Elect Trump pledged to impose tariffs on each respective country's imported products.

USD

The US Dollar rose on Tuesday after President-elect Donald Trump said he could impose tariffs on products coming into the United States from Mexico, Canada and China, as investors braced for policies that could set the stage for trade spats. In an initial knee-jerk reaction to Trump's comments, the dollar jumped more than 2% against the Mexican peso and hit a four-and-a-half-year high against its Canadian counterpart. The main scheduled news release left this week is on Wednesday with the October Personal Consumption Expenditures price index.

USD should remain supported at the 106 handle in the near term.

GBP

The British Pound was little changed on Tuesday, relatively unscathed after a threat from U.S. President-elect Donald Trump to ramp up tariffs on Canada, Mexico and China sparked volatility in currency markets. Sterling initially lost ground after Trump's comments, reflecting its position as a "risk-sensitive" currency that tends to fall at moments of economic uncertainty. But it later perked up and was last 0.1% higher at $1.2587. Some analysts say Britain's minor trade surplus with the United States meant it could escape President-elect Trump's focus.

Should Sterling rebound on profit taking, there may be some resistance at 1.2720.

CNH

The Chinese Yuan fell against the U.S. dollar to its weakest in nearly four months after U.S. President-elect Donald Trump said he could impose a 25% tariff on all products from Mexico and Canada, and an additional 10% tariff on goods from China. Offshore yuan (CNH) dropped roughly 0.3% on the news to 7.2730 per dollar, its lowest since July 30, while onshore yuan (CNY) also fell after the market opening. Prior to the market opening, the People's Bank of China (PBOC) set the midpoint rate, around which the yuan is allowed to trade in a 2% band, at 7.1910 per dollar, which was 450 pips firmer than the market's estimate.

USDCNH looks to be approaching the resistance level of 7.2800 as Dollar continues to remain strong.

XAU

Gold prices were caught in a tug-of-war on Tuesday, dipping to a week's low as safe-haven demand softened as Israel agreed to a ceasefire deal with Lebanon, while concern over Ukraine and U.S. President-elect Donald Trump's tariff plans limited declines. This follows Monday's dramatic $100 plunge, when gold retreated from a three-week high. The sell-off was fueled by Israel and Hezbollah ceasefire optimism and further pressured by Trump's nomination of Scott Bessent as Treasury Secretary, which tempered demand for gold as a safe haven. Concern over the wider fallout from Russia's invasion of Ukraine continues to remain very high, and gold will likely experience choppy consolidation in the near term, ranging between $2,575-$2,750.

The precious metal should find support at 2536 with the current economic and geopolitical developments.