Market Daily

Macro Update:

China’s credit data disappoints despite policy support

China’s total social financing and new bank lending both missed expectations and slowed to new record lows of 7.8% YoY and 8.0% YoY respectively in October. The soft credit demand shows more fiscal stimulus to counter headwinds is needed.

The Ministry of Finance reiterated last Friday its rosy forward guidance for 2025. We expect more forceful stimulus in 2025 budget. Chinese equity market could remain volatile in the short term given concerns over US tariffs. That said, China A-shares are likely to be more resilient as they are more direct beneficiaries of the ongoing capital market reforms.

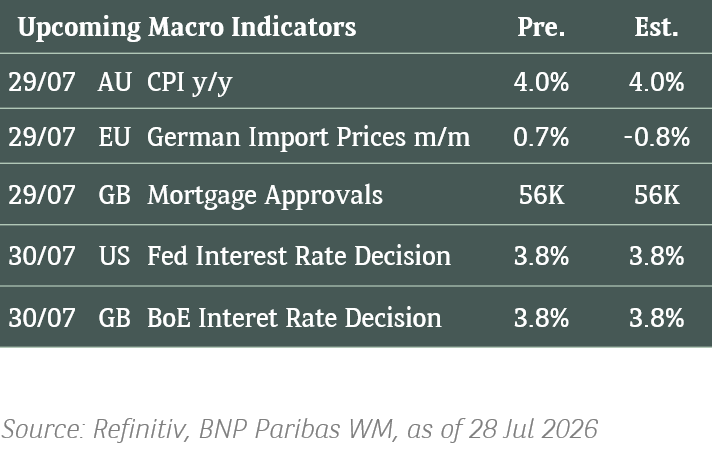

Main Upcoming Macro Indicators

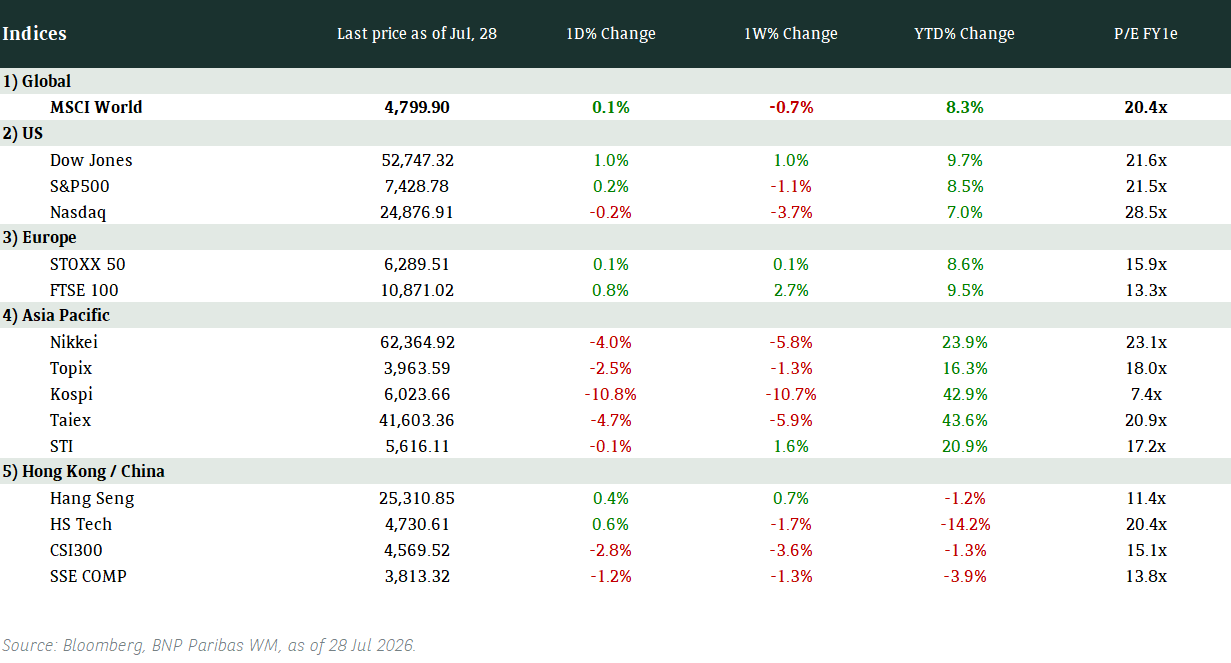

Equity Market Updates

US EQUITIES

US stocks rose again on Monday as the post-election rally continues.

Most of 2024’s uncertainties has now passed, and this upward momentum is likely to stay in the near term.

EUROPE EQUITIES

European equities logged solid gains on Monday, led by defence stocks, as investors await key economic data this week.

HK EQUITIES

Stocks in Hong Kong continued its move lower on Monday as investors digest Friday’s Chinese National People’s Congress announcements amid rising concerns about tariffs following the US elections.

Cigna (CI US)

Cigna confirmed on Monday that it is not pursuing a combination with rival health insurer Humana, days after Donald Trump's reelection as US president raised investor hopes that any merger would face far less antitrust scrutiny.

The announcement comes after Cigna and Humana previously canceled their merger talks after failing to reach a deal on price, alongside other financial terms in December last year.

Cigna’s stock price surged on Monday, while Humana’s fell.

MARKET CONSENSUS: 21 BUYS, 3 HOLDS, AVERAGE TP USD397.75

Chipotle (CMG US)

Chipotle was sued on Monday by shareholders for concealing how many of its restaurants were skimping on portions and failing to disclose growing unhappiness among customers with inconsistent portion sizes for its burritos and rice bowls. Developments regarding this lawsuit could potentially put downward pressure to the company’s share price in the near term.

The lawsuit came as Chipotle also named interim CEO Scott Boatwright as permanent CEO to replace Brian Niccol who departed in August to Starbucks.

MARKET CONSENSUS: 23 BUYS, 11 HOLDS, 1 SELL, AVERAGE TP USD65.29

Grab (GRAB US)

Singapore’s Grab on Monday raised its forecast for FY2024 revenue to USD2.76B-USD2.78B from USD2.70B –USD2.75B, as the company anticipates robust growth in its food delivery and ride-hailing businesses.

The announcement is likely to add fuel to the company’s recent share price rally as it reassures investors that its business is recovering nicely from a post-pandemic slump.

MARKET CONSENSUS: 25 BUYS, 3 HOLDS, 1 SELL, AVERAGE TP USD4.68

Continental (CON GY)

Shares of Continental rose on Monday after it posted a 3Q24 earnings beat. The company’s net income for the quarter stood at EUR486.0M vs. EUR457.3M expected.

Despite solid results, the German automotive and industrial supplier also cut its annual sales guidance for the second time this year, to EUR39.5B-EUR42.0B from EUR40.0B-EUR42.5B previously, citing weak industrial demand in Europe and North America. This could potentially raise questions on the sustainability of Continental’s growth trajectory going forward, injecting volatility to the company’s share price.

MARKET CONSENSUS: 12 BUYS, 9 HOLDS, 3 SELLS, AVERAGE TP EUR75.63

ASMPT (522 HK)

ASMPT said on Monday that it is no longer in privatization talks with a potential offeror after the company said last month it had received a takeover bid without providing any further details.

The news is likely to put downward pressure on ASMPT’s stock price as it slashed investors’ hopes on receiving a takeover premium.

Netherlands-based semiconductor equipment maker ASM International, which owns around 25% stake in ASMPT, has in the recent past been asked by activist investors to sell its holdings in the company.

MARKET CONSENSUS: 17 BUYS, 5 HOLDS, AVERAGE TP HKD101.48

Earnings Announcements

US Market

Home Depot, Plug Power, Skyworks Solutions

European Market

Bayer, AstraZeneca, Infineon Technologies, Spotify

HK - China Market

Tencent Music Entertainment, SJM Holdings

Global Indices Changes (%)

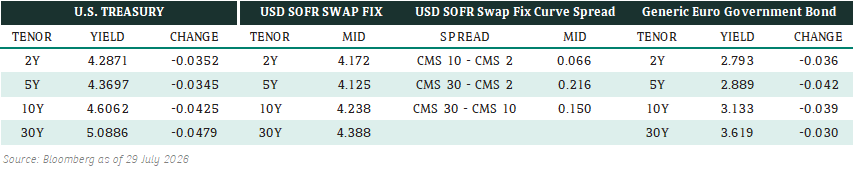

Fixed Income Market Updates

We expect the bond market sentiment will gradually stabilise from recent US Treasury panic sell-off after the election. We remain comfortable with 5-10 year good quality IG bonds. Fixed income remains a good defensive instrument amidst this volatile market environment, as it will likely be a while until we see how Trump’s actions going to impact the economy.

EUROPEAN AT1

European bank AT1s was largely stable but the market to question what will happen to the AT1 market after a Republican Sweep. It is also unclear how the growth outlook in Europe could be impacted especially when AT1 credit spread is already very tight. Going forward, we expect the AT1 market could turn more volatile and could see some correction as valuation is not cheap. However, any meaningful correction would be a good opportunity to add given we remain comfortable on European banks’ long-term credit fundamental.

ASIA INVESTMENT GRADE (IG)

Asia IG was relatively quiet as US was out for holiday. Sovereign and quasi-sovereign bonds traded in a muted tone with the Treasury market closed. IG credit spreads were largely unchanged with some selling seen in the long end, particularly in Philippine IG. Likewise, Indonesia IG was also under some selling pressure. Overall, we expect Asia IG will stay quiet as we approach year-end.

ASIA HIGH YIELD (HY)

Asia HY had a muted day. China HY was again the spotlight with the overall sentiment being quite weak after the smaller-than-expected debt swap package announced by the Central government last Friday. Within China HY property, Dalian Wanda and Shui On Land traded 0.5-1.5 points lower. We expect China HY will stay weak until we see more Government stimulus package. Outside of China, Indian HY space saw some institutional investors selling, but generally well absorbed by private bank investors. The Adani complex was particularly active with short-dated bonds relatively well bid by hedge fund investors.

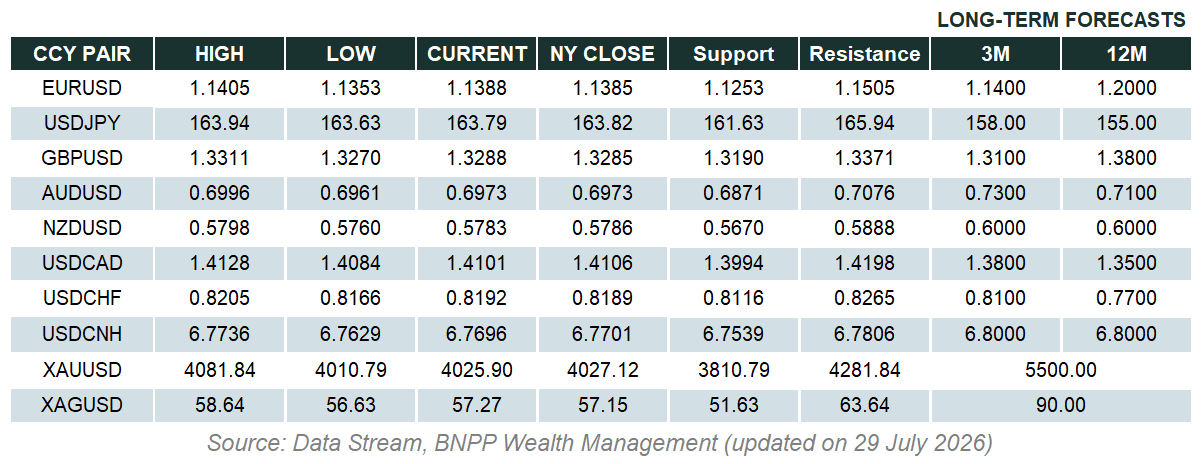

Forex Market Updates

The US Dollar advanced at the start of the week after a Fed policymaker gave a positive appraisal of the state of the US economy ahead of this week's key US inflation data.

USD

The US Dollar surged to fresh four-month highs against a basket of other major currencies on Monday with Trump trades still dominating market positioning. The greenback was also supported by comments from Fed policymaker Kashkari, who stated that the US economy has remained remarkably strong while the central bank has made significant strides in beating back inflation, and that “another rate cut is certainly possible” at the Fed’s December meeting. Echoing Fed Chair Powell’s recent comments, Kashkari added that the central bank can at this point only “wait and see” what the incoming Trump administration decides to do before analyzing what it will mean for the US economy.

USD bulls are likely to target the 106.00 handle in the Dollar Index with bullish momentum looking strong for now.

EUR

The Euro slumped yesterday to its lowest level in almost seven months against the USD on growing concerns that the Eurozone economy will be disproportionately affected by incoming POTUS Trump’s proposed tariffs. Analysts say that rumours that Trump had asked Robert Lighthizer, a well-known hawk on trade and the US Trade Representative during Trump’s first presidential term, to play a significant role in the new administration weighed on the common currency because the Eurozone economy is not just very open but also heavily exposed to China, while the inflationary effects of Trump’s tariffs could also serve to widen the Fed-ECB monetary policy divergence.

The common currency looks vulnerable to more near term weakness towards 1.0600.

CHF

The Swiss Franc fell to three-month lows yesterday as broad USD strength drove price action in FX markets. However, CHF losses were limited by somewhat hawkish comments by SNB Vice Chair Martin, who said that the central bank is not locked into more rate cuts in December. This ran contrary to previous remarks by both Martin and SNB Chair Schlegel that interest rates could be lowered further and even taken below zero, especially with Swiss inflation being reported at 0.6% in October, the lowest level in more than three years.

USDCHF could edge higher towards immediate resistance around 0.8860 moving forward.

XAU

Gold prices started the week extending their recent decline, hurt by broad USD strength and healthy risk appetite as markets expect the Fed to adopt a cautious approach to monetary policy easing under Trump 2.0. With a Red Sweep of POTUS, Senate and House of Representatives looking likely to materialize, Trump’s proposed fiscal policies are expected to encounter little resistance, which analysts say will complicate the Fed’s fight against inflation and lead to upside pressure on yields and a stronger USD, acting as possible headwinds for bullion moving forward.

The precious metal could weaken towards 2550 on a firm break below technical support around the 2600 handle.