Market Daily

Macro Update:

Hong Kong equities decline after Trump appoints China hawks

Trump is reported to appoint Mike Waltz as his national security adviser and close to nominate Marco Rubio to be Secretary of State. Both viewed China as a great threat.

We remain cautiously optimistic on China equities in the medium term due to three reasons: (1) It is likely that Beijing prefers to introduce further stimulus in 2025 budget after Trump’s inauguration. (2) The 60% tariffs on China is not our base case scenario. This could be Trump’s tactics for a trade deal (may take less time to reach a trade deal in Trade War 2.0). (3) Despite the volatility in the short term, we expect domestic A-shares (i.e. CSI 300 Index) to be more resilient because of the ongoing capital market reform. The swap facility has also been working well to improve market liquidity and encourage inflows into the A-share markets.

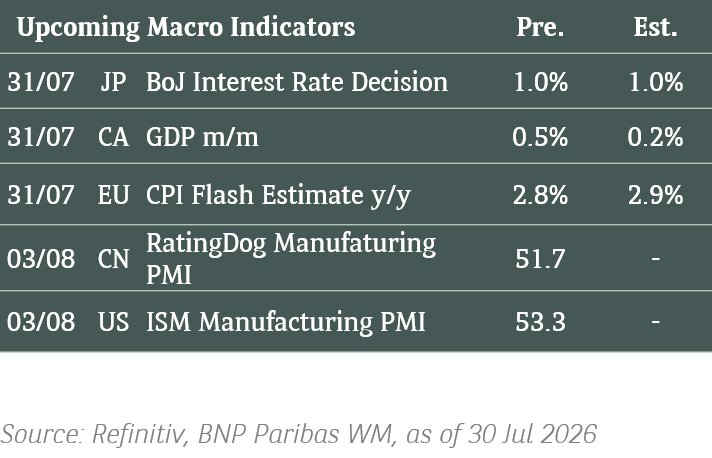

Main Upcoming Macro Indicators

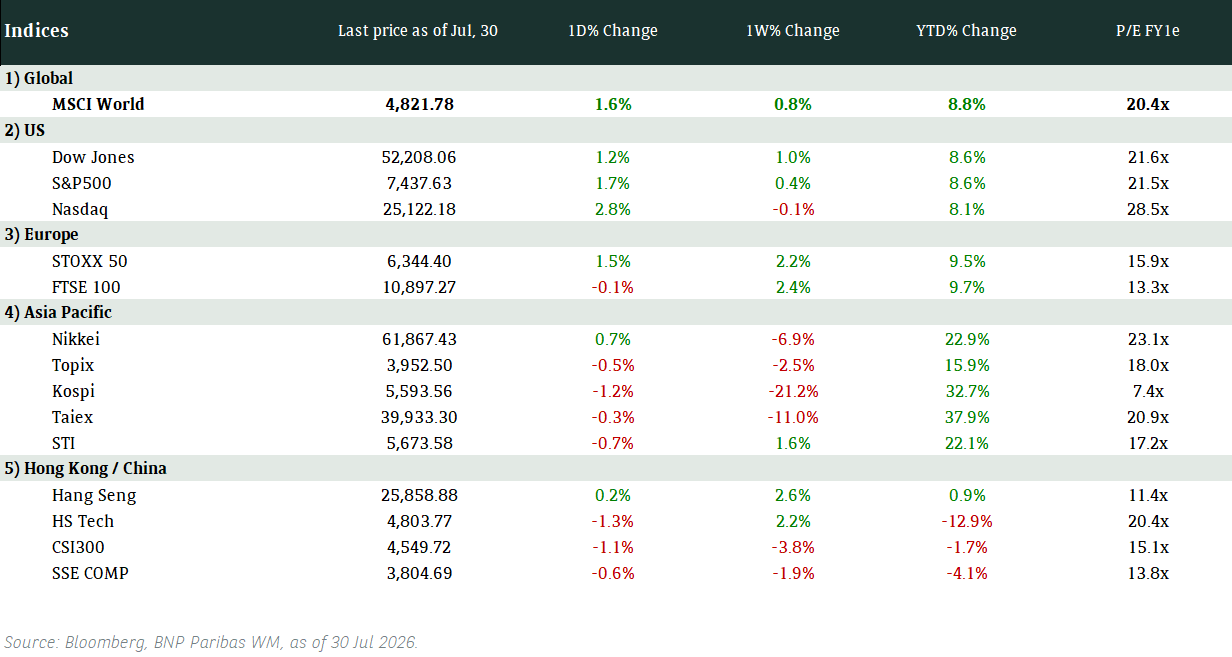

Equity Market Updates

US EQUITIES

US equities ended slightly lower on Tuesday as the market took a breather after a weeklong election-fuelled rally.

Nevertheless, the market's move up is likely to continue as we enter the tail end of 2024.

EUROPE EQUITIES

European shares plunged on Tuesday as concerns grew over stocks with significant exposure to China, while some downbeat earnings also weighed.

HK EQUITIES

Hong Kong stocks fell on Tuesday, erasing almost all of its stimulus-induced gains, as data showed borrowing in mainland China slowing in October.

Spotify (SPOT US)

Spotify on Tuesday announced 4Q24 profit guidance that beat Wall Street estimates, betting on its recent cost cuts and strong subscriber growth in the crucial holiday season.

The announcement provides evidence of management confidence in the company’s current strategic direction, potentially supporting share price in the near to medium term.

Spotify on Tuesday also posted beats in operating profit (USD454.0M vs. USD390.2M expected) and subscriber count (252M vs 250M expected), although revenue and net profit were slight misses.

MARKET CONSENSUS: 29 BUYS, 9 HOLDS, 1 SELL, AVERAGE TP USD413.9

Honeywell (HON US)

Activist investor Elliott Investment Management said on Tuesday that Honeywell should split into two separate businesses, following in the footsteps of other industrial conglomerates that have broken up in recent years.

Further developments on a potential breakup could inject volatility into the company’s share price going forward.

Elliott specifically said in a letter that it had built a stake worth more than USD5B in Honeywell, one of its largest ever, and that management should split the company into two standalone businesses focused on aerospace and automation.

MARKET CONSENSUS: 12 BUYS, 13 HOLDS, 1 SELL, AVERAGE TP USD234.1

Rivian (RIVN US)

Volkswagen said on Tuesday that it has raised its investment in Rivian by 16% to around USD5.8B, as the companies kick off their planned joint venture to develop electric vehicle architecture and software, sending the EV maker’s shares up in extended trading.

The investment could be a crucial lifeline for Rivian as it gears up to release its smaller, cheaper SUV called R2 amid high borrowing costs and slowing EV demand.

MARKET CONSENSUS: 25 BUYS, 3 HOLDS, 1 SELL, AVERAGE TP USD4.68

AstraZeneca (AZN LN)

AztraZeneca shared on Tuesday 3Q24 results that beat Wall Street estimates, with revenue at USD13.6B vs. USD13.1B expected, and adjusted EPS at USD2.08 vs. USD2.06 expected, boosted by increasing demand for medicines across Oncology, BioPharmaceuticals, and Rare Disease.

The company also raised its annual revenue forecast and plans to invest USD3.5B in its US business by the end of 2026.

Announcements on Tuesday provide evidence of AstraZeneca’s still-flourishing business, which should support share price going forward.

MARKET CONSENSUS: 22 BUYS, 7 HOLDS, 1 SELL, AVERAGE TP GBp13836.71

SoftBank (9984 JP)

SoftBank on Tuesday swung to its biggest quarterly profit in two years on a series of successful Indian listings. The company’s net income featured a massive beat at JPY1.18T vs. JPY294.8B expected, with revenues at JPY1.77T, largely in line with consensus.

SoftBank’s Vision fund in FY2Q25 logged a solid JPY373B gain, which was also bolstered by a lift in values of companies like Didi Global and Coupang Inc.

Positive announcements on Tuesday could prove to be signs of a positive turnaround for SoftBank, supporting its share price going forward.

MARKET CONSENSUS: 18 BUYS, 4 HOLDS, 1 SELL, AVERAGE TP JPY11711.18

Earnings Announcements

US Market

Cisco Systems

European Market

Siemens Energy, Porsche, ABN AMRO Bank

HK - China Market

Tencent

Global Indices Changes (%)

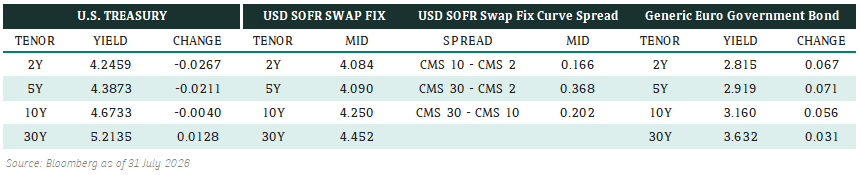

Fixed Income Market Updates

We expect China IG and HY bonds will both turn more volatile as the market was disappointed with the weaker-than-expected Government stimulus package. Another market concern is the more anti-China Trump’s new administration. We suggest to reduce China fixed income exposures for risk management ahead of more geopolitical headlines between US and China.

EUROPEAN AT1

European bank AT1s was slightly weaker. Bond prices were 0.125-0.25 points lower. There was more selling in the long end as investors worry about Trump’s inflationary policy. Going forward, we expect the sector could be under some selling pressure as the valuation is not cheap. But any meaningful correction will be a good opportunity to add, particularly the ones with short call date.

ASIA INVESTMENT GRADE (IG)

Asia IG consolidation continued. Overall market flows were mixed and quiet. Private bank clients are skewed towards buying whereas institutional investors were reducing fixed income exposures. In China-HK, we saw good demand on good quality names such as Meituan, AIA, and CK Hutchison. Outside of China, short-dated Korea IG papers were popular. In India IG, Adani continued to outperform and we saw more demand in its short-dated papers. Overall, we expect Asia IG trading activities will be low as we approach year-end.

ASIA HIGH YIELD (HY)

Asia HY remained slow. China HY property traded with a slightly better tone with Dalian Wanda rebounding 0.5 points higher. However, the sector is losing momentum after the weaker-than-expected credit data in China. We expect China HY will stay weak until we see more updates on government policy stimulus. Outside of China, India HY was mostly unchanged across various bonds.

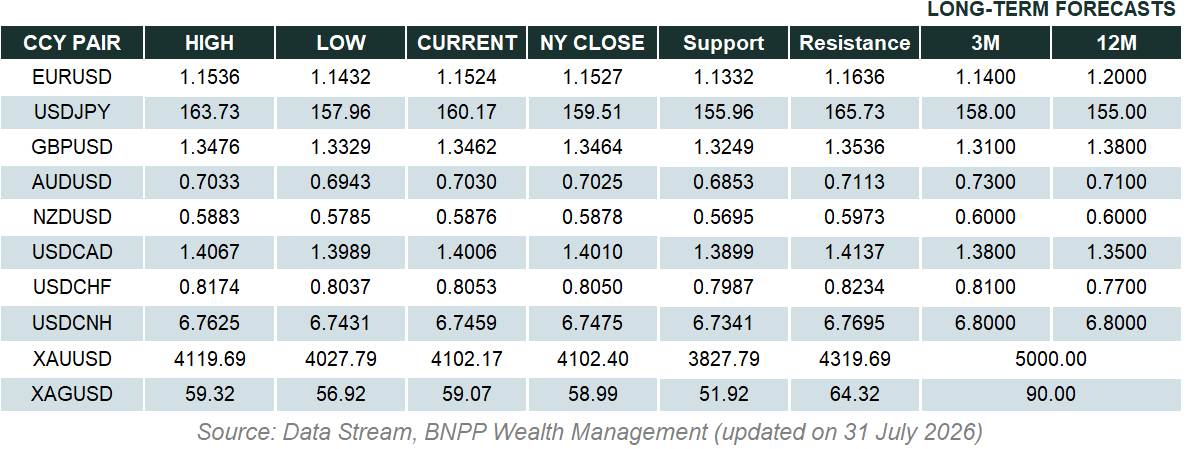

Forex Market Updates

The US Dollar continued its march higher, buoyed by economic growth expectations under a second Trump presidency and a reduced Fed easing outlook.

USD

The US Dollar rose to a more than six month high against a basket of other major peers before retracing slightly on Tuesday as traders continued to pile into the greenback on expectations that Trump’s proposed tariffs will push up prices and leave the Fed less room to cut interest rates. On the data front, a survey of US Small Business Optimism came in well above estimates, while the USD was also supported by bullish comments on the US economy from Fed policymaker Barkin, who also said that “the Fed is in position to respond appropriately regardless of how the economy evolves”.

The Dollar Index could see more near term strength, with USD bulls likely to target the 106.50 level.

EUR

The Euro's post-US election slump continued on Tuesday amid rapidly growing concerns about the outlook for the Eurozone economy, with some banks even seeing the possibility of a decline below parity should the Trump 2.0 administration deliver stiff global tariffs and aggressive fiscal easing. Elsewhere, ECB policymaker Rehn said that a December rate cut is likely and that further reductions are possible given that the central bank sees downside risks to the Eurozone economy, emphasizing that the “growth and productivity outlooks are weak” in the common market.

The common currency is likely to trade heavy moving forward, with 1.0525 the next level of support.

GBP

The British Pound fell to three-month lows yesterday on the back of a disappointing UK jobs report which showed that regular wage growth cooled in 3Q2024 to its lowest level in more than two years, while the unemployment rate ticked higher to 4.3%. Some analysts say that the easing in private sector wages suggest that the BoE will continue to cut rates gradually, although BoE Chief Economist Pill said that the data also showed that inflationary pressures in Britain remained too high for the BoE’s 2% inflation target.

Sterling looks poised to see more near term losses towards immediate support around 1.2660.

XAU

Gold prices fell for the third consecutive session, touching one-month lows in the face of a stronger USD, optimism about US economic growth under a second Trump presidency and a broader market pivot into riskier assets following last week’s US elections. Some analysts say that this recent pullback in the precious metal is just a corrective move in a longer term bullish market, and that the expected inflationary effects of Trump’s proposed tariffs, combined with ongoing geopolitical uncertainty, should drive gold prices higher again further out.

The precious metal could weaken towards 2550 on a firm break below technical support around the 2600 handle.