Market Daily

Macro Update:

Fed reduce rates by 25bps but signals less cuts in 2025

The Fed lowered interest rates by another 25bps yesterday as expected, but delivered a hawkish view for 2025. The central bank signalled only two rate cuts (totalling 50bps) in 2025, versus the previously expected four cuts (a full percentage point). The Fed also lowered its 2025 forecast for unemployment rate and raised expectations for core inflation and economic growth. This is in line with recent data, which has suggested a resilient US economy, limiting the urgency for looser monetary policy. Investors were largely disappointed with the hawkish tone, and the equity market sold off while the treasury yields surged. Markets are also starting to price in a pause for the upcoming January FOMC with a much higher certainty at 88%.

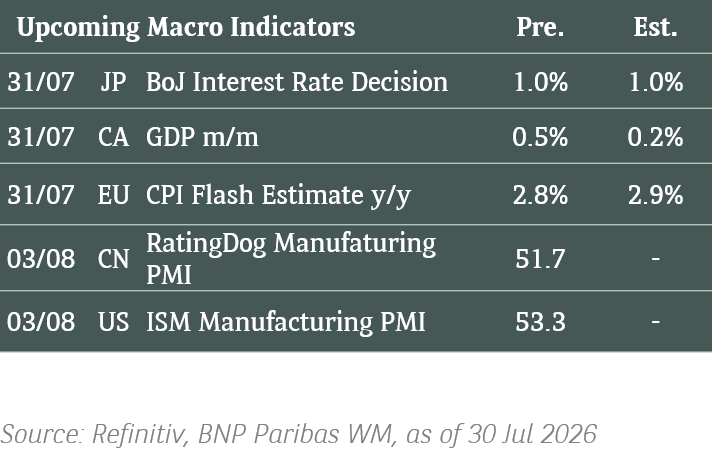

Main Upcoming Macro Indicators

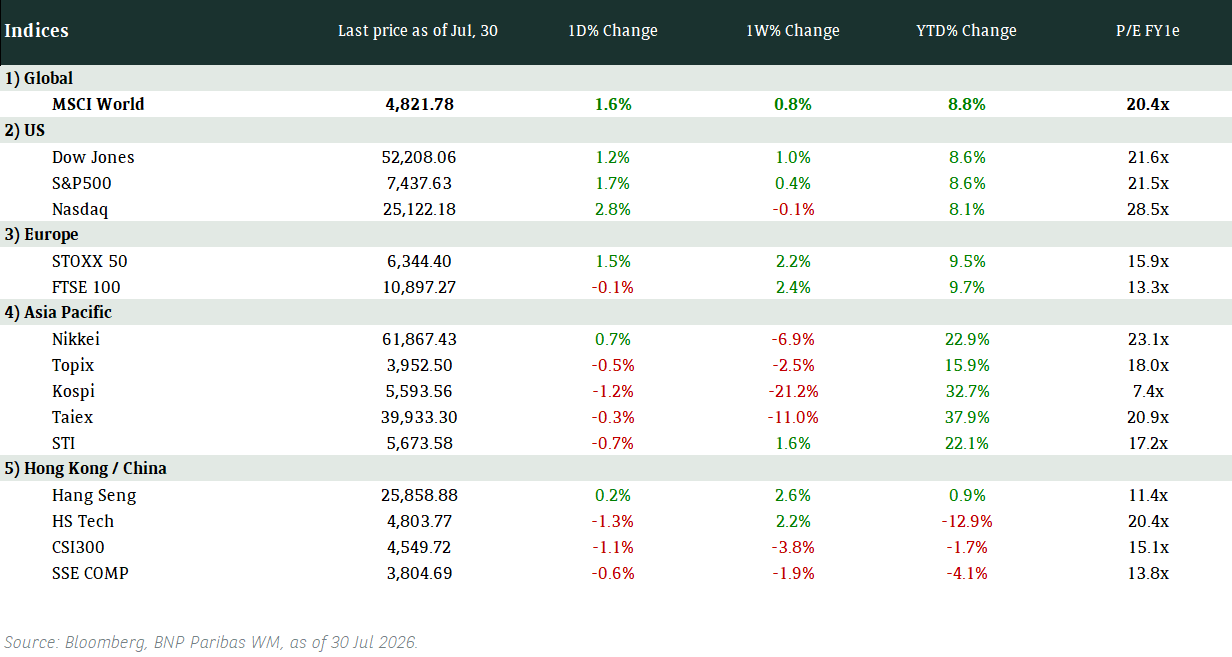

Equity Market Updates

US EQUITIES

US stocks fell on Wednesday as investors reevaluate the Fed’s policy rate trajectory after the central bank’s hawkish commentary yesterday.

EUROPE EQUITIES

European shares largely traded higher on Wednesday, boosted by technology stocks, though gains were capped as investors remained cautious ahead of the Fed’s policy decision and outlook.

HK EQUITIES

Hong Kong stocks rose on Wednesday as investors cheered the introduction of guidelines to help state-owned companies boost their values and the halving of service fees for dividend payouts.

Micron Technology (MU US)

Shares of Micron fell sharply in late trading on Wednesday after it announced a cautious outlook for its current quarter, citing weakness in consumer-oriented markets such as PCs and smartphones, even as its business serving data center booms. The company’s revenue forecast missed projections by about USD1B. This could put downward pressure to Micron’s stock price going forward.

Micron’s FY1Q25 revenue stood at USD8.7B, in line with expectations, while its adjusted EPS was at USD1.79 vs. USD1.76 expected.

MARKET CONSENSUS: 38 BUYS, 4 HOLDS, 1 SELL, AVERAGE TP USD146.52

Eli Lilly (LLY US)

Eli Lilly on Wednesday secured approval from the Chinese National Medical Products Administration for its Kisunla medicine to treat adults with early symptomatic Alzheimer's disease. China is the fourth major market in which Kisunla has received approval after the US, Japan, and the UK. This could boost the company’s top line in the country, supporting its share price going forward.

Eli Lilly’s approval was backed by a Trailblazer-ALZ 2 phase 3 clinical study, which tested two groups with low to medium and an overall population with high levels of tau protein. In the overall population, Kisunla reduced amyloid plaques by 61% on average at six months and 80% and 84% at 12 months and 18 months, respectively.

MARKET CONSENSUS: 29 BUYS, 5 HOLDS, 1 SELL, AVERAGE TP USD994.99

Netflix (NFLX US)

The Dutch Data Protection Authority said on Wednesday that it fined Netflix EUR4.75M for not properly informing customers about its use of their personal data between 2018 and 2020, concluding a case which started in 2019.

The fine is unlikely to materially impact Netflix’s financial health, as it only stands at around 0.2% of its latest quarterly net income. The unwinding of uncertainties surrounding the case, however, is likely a positive for the company.

MARKET CONSENSUS: 41 BUYS, 18 HOLDS, 4 SELLS, AVERAGE TP USD845.62

UniCredit (UCG IM)

Unicredit on Wednesday raised its stake in Commerzbank to 28%, building on previous efforts to stock up its holding in its German rival while reigniting expectations that it could launch a mandatory takeover offer for the lender.

UniCredit has been circling Commerzbank since September this year, when it flagged interest in a potential tie-up and disclosed a stake in the German group. Shortly after, it raised its shareholding further through the same mechanism of entering into financial contracts tied to Commerzbank shares.

UniCredit’s stake is now made up of 9.5% direct ownership and around 18.5% through derivatives.

MARKET CONSENSUS: 16 BUYS, 6 HOLDS, AVERAGE TP EUR47.02

Unilever (ULVR LN)

Unilever announced on Wednesday that its food brands Unox and Zwan, which have been a part of the company's portfolio for close to 100 years, will be acquired by Zwanenberg Food Group. Unilever expects to close the deal, terms of which were not disclosed, by 2025.

The move was made as Unilever aims to sharpen its Foods portfolio for long-term growth and scalability, focusing on fewer and bigger brands, in categories such as cooking aids, mini meals and condiments. This could improve the company’s efficiency and thus be supportive to its share price in the long run.

MARKET CONSENSUS: 15 BUYS, 8 HOLDS, 4 SELLS, AVERAGE TP GBp5005.17

Earnings Announcements

US Market

Darden Restaurants

European Market

Accenture

HK - China Market

-

Global Indices Changes (%)

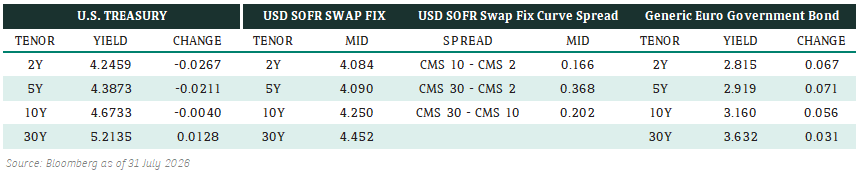

Fixed Income Market Updates

Investors have performed well this year and are likely to engage in some profit-taking within their fixed-income portfolios to secure year-to-date gains. As we approach year-end, they are expected to maintain a neutral stance on duration and the yield curve shape following the December FOMC meeting.

EUROPEAN BANK COCO (AT1)

The AT1 market had a subdued start to the holiday season, with flows skewed slightly towards selling. Recent rate weakness impacted the broader AT1 space, as the market shifted back to rate-watching mode, particularly if the 10-year yields approach the 4.5% level.

ASIA INVESTMENT GRADE (IG)

In China IG, spreads remained stable, with front-end bonds still in demand as investors sought short-dated carry ahead of the FOMC meeting. However, there was selling pressure on HK IG names, primarily from hedge fund reacting to the share price drop of New World Development. Outside of China, trading activity was muted amid year-end liquidity constraints. High-quality corporates continued to attract interest, with regional investors deploying cash into the 10-year segment of Thai and Indian papers as rates hovered around 4.4%.

ASIA HIGH YIELD (HY)

In China HY, New World Development was the most notable name, with its curve down 3 – 10 points amid early trimming by institutional accounts. The broader property sector showed limited reaction, with only minor selling in Jinmao and Longfor from private wealth accounts. Meanwhile, the Japanese HY space remained quiet, aside from some small purchase of SoftBank.

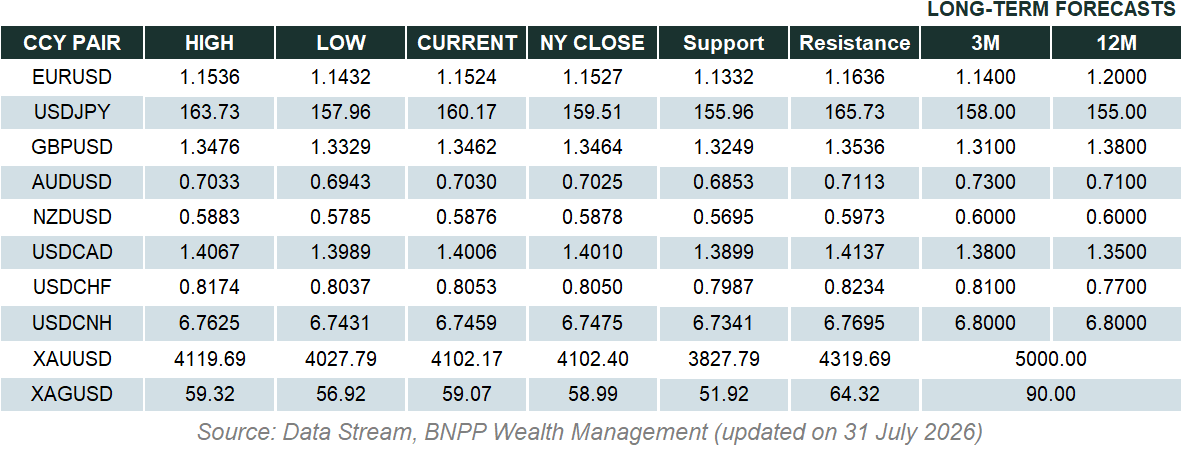

Forex Market Updates

Following the Federal Reserve's anticipated interest rate cut, the US dollar strengthened against other currencies on Wednesday, reaching its highest level in two years

USD

The US Dollar advanced against its peers on Wednesday, hitting its highest level in two years, after the Fed delivered a widely expected interest rate cut while also indicating it would slow the pace of its monetary policy easing cycle. Dollar Index rose to as high as 108.260, hitting its highest level since November 2022. Despite economic uncertainties, such as a weakening labor market and ongoing inflation, the central bank's gradual policy adjustments indicate a cautious approach between controlling US price pressures and fostering economic growth.

The Dollar Index looks poised to stay well supported above 106 in the near term.

AUD

The Australian Dollar hit fresh low on Wednesday as positive economic developments in the US captured the attention of investors, leading to an increased focus on the US dollar. The Aussie dipped a further 0.1% to a 13-month low of $0.6325. Investors have also become more confident that the Reserve Bank of Australia will start trimming its 4.35% cash rate as early as February. Additionally, the absence of specific details regarding China’s fiscal support has exerted pressure on the Aussie, considering China's significant role as Australia's largest trading partner.

AUDUSD may continue to face downward pressure to navigate the descending lower boundary around the 0.6200 level.

GBP

The Sterling experienced volatility against other major currencies following the release of the UK Consumer Price Index data for November. The data solidifies expectations that the Bank of England will maintain interest rates at 4.75% in their upcoming policy meeting, with a split vote of 8-1. Market participants will closely monitor BoE Governor Andrew Bailey's press conference for any indications of potential policy easing in 2025. Additionally, the UK November retail sales data, set to be released on Friday, will be of interest to investors.

Sterling is likely to find a cushion near the psychological support of 1.2500 moving forward.

XAU

Gold prices slipped more than 2% to a one-month low on Wednesday after the US Fed lowered interest rates as expected, but noted it will slow the pace at which borrowing costs fall any further, boosting the dollar and bond yields. Spot gold was down 2.1% at $2,589.91 per ounce, its lowest level since Nov. 18 this year. Investors will direct their attention to key economic indicators this week, including Thursday's release of US GDP data and the core Personal Consumption Expenditures (PCE) Price Index, which could impact Bullion demand.

The precious metal should remain range-bound staying between 2560 and 2720.