Market Daily

Macro Update:

US data remains robust while BoE and BoJ held rates steady

Robust data in the US suggests a stronger than expected economy. GDP was revised higher in its final estimate to show a 3.1% annualized expansion in Q3, while initial jobless claims tumbled more than expected, which lowers the urgency for the Fed to reduce rates in 2025. Elsewhere in UK, the Bank of England left interest rates unchanged at 4.75%, reflecting heightened concerns over stubborn inflation despite signs of slowing growth. The Bank of Japan also left its policy rate unchanged at 0.25%. BoJ Governor Ueda dovish comments post-meeting, as well as the stronger dollar post FOMC, pressured the Japanese yen. We still think the BoJ is likely to hike in January 2025, and that should help to stablise the Yen going forward.

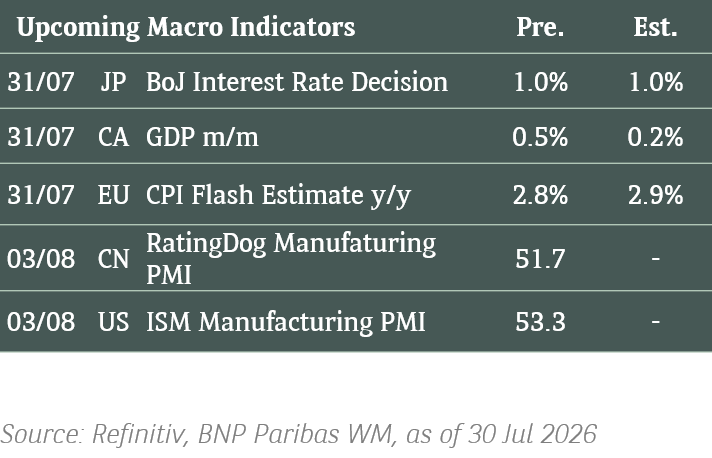

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks ended largely flat on Thursday as investors continued to parse the Fed’s hawkish comments.

EUROPE EQUITIES

Stocks in Europe slid on Thursday as markets readjust their policy rate outlooks.

HK EQUITIES

Hong Kong stocks closed lower on Thursday on possibly lower rate cuts from the US next year.

Hang Seng Index nevertheless pared losses from more than -1% when it opened to around -0.5% at close.

Nike (NKE US)

Nike on Thursday posted FY2Q25 results that beat estimates with revenue at USD12.4B vs. USD12.1B expected, while EPS was at USD0.78 vs. USD0.63 expected.

Looking ahead, new Nike CEO Elliot Hill pledged in the company’s earnings call to reignite growth by refocusing on sports and mending ties with retail partners, specifically through “more aggressive” sports-related marketing and eliminating discounts for online sales. Nevertheless, Hill noted that some of his plans will have a negative impact on near-term results. This could add volatility to Nike’s share price in the near to medium term.

MARKET CONSENSUS: 23 BUYS, 20 HOLDS, 2 SELLS, AVERAGE TP USD90.48

Apple (AAPL US)

Apple is reportedly in early discussions with Tencent and ByteDance to integrate their artificial intelligence (AI) models into iPhones in China.

Due to censorship reasons, the US' AI models (ie. ChatGPT, OpenAI) cannot be deployed in China. This hence paves the foray for local systems.

The Apple collaboration, if eventually realised, will likely improve Tencent and ByteDance’s positions in the AI space, supporting both companies’ share price going forward.

MARKET CONSENSUS: 39 BUYS, 18 HOLDS, 3 SELLS, AVERAGE TP USD245.4

FedEx (FDX US)

Shares of FedEx jumped in after-market trading on Thursday after it announced a spin-off of its freight division, a move that will advance CEO Raj Subramaniam’s push to streamline the parcel giant and thus support the company’s share price going forward.

Yesterday’s share price surge happened despite FedEx trimming its FY2025 outlook, citing weak demand in Freight and Parcel.

FedEx’s FY2Q25 revenue stood at USD22.0B vs. USD22.1B expected, with adjusted EPS at USD4.05 vs. USD3.98 expected.

MARKET CONSENSUS: 20 BUYS, 14 HOLDS, 2 SELLS, AVERAGE TP USD307.83

Accenture (ACN US)

Shares of Accenture surged on Thursday after it posted a results beat for FY1Q25, driven by strong demand for generative AI services. This further establishes Accenture as a significant beneficiary of the current structural AI trend, likely supporting its share price going forward.

Accenture’s FY1Q25 revenue was at USD17.67B vs. USD17.1B expected, while EPS was at USD3.59 vs. USD3.42 expected.

MARKET CONSENSUS: 19 BUYS, 9 HOLDS, 1 SELL, AVERAGE TP USD391.7

Roche (ROG SW)

Roche on Thursday said that its investigational early-stage Parkinson's disease drug prasinezumab failed to meet the primary endpoint of the phase 2b Padova study, potentially adding uncertainty to the drug’s journey to market and downward pressure to the Roche’s share price going forward.

According to a statement by Roche, prasinezumab showed potential in delaying confirmed motor progression, though the results were not statistically significant. The company added that the experimental drug continued to be well tolerated, with no new safety signals flagged during the study.

MARKET CONSENSUS: 14 BUYS, 8 HOLDS, 4 SELLS, AVERAGE TP CHF306

Earnings Announcements

US Market

-

European Market

-

HK - China Market

-

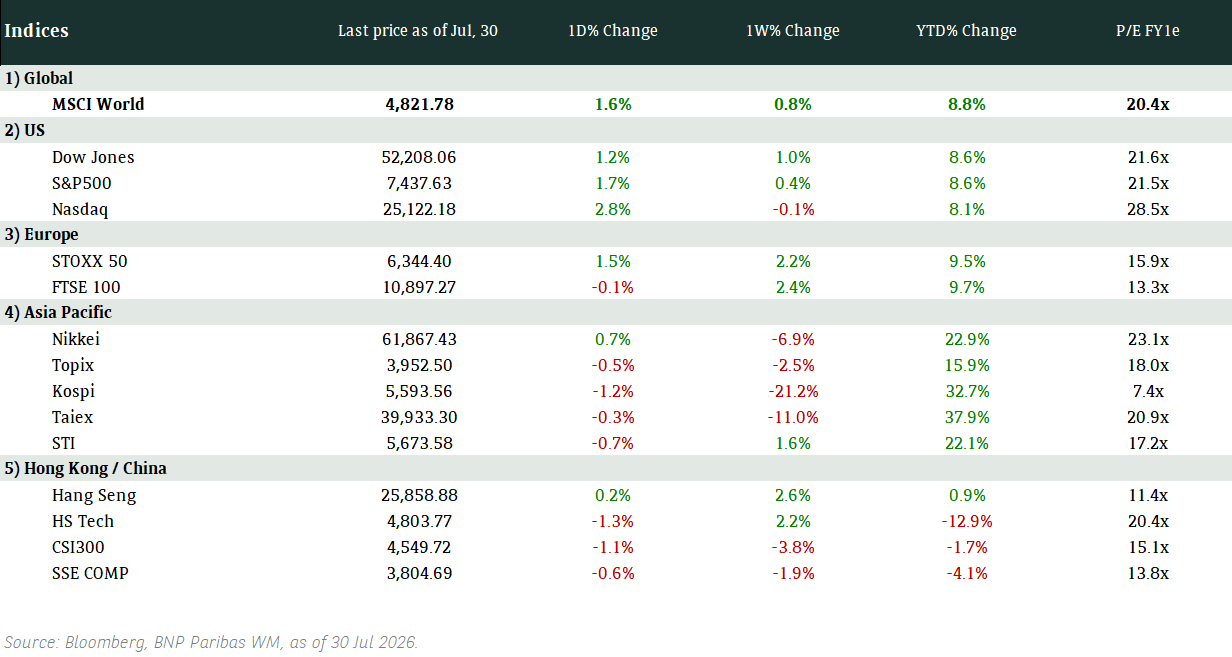

Global Indices Changes (%)

Fixed Income Market Updates

As rates stay higher for longer, we are wary of the effects of higher borrowing costs on corporates' operating margins. Credit selection will remain key going forward.

EUROPEAN BANK COCO (AT1)

Prices were lower post FOMC in the Eurpoean AT1 market, with prices down around 0.375-1.25point on average. Most of the price movements were due to rates, with only small amounts of widening. Thin liquidity as we near Christmas holiday season exacerbated the price moves. We still like AT1 bonds of major banks with solid fundamentals for yield pickup and would position to buy on dips next year.

ASIA INVESTMENT GRADE (IG)

South-East Asia IG space continued to resist any US Treasury led weakness and closed the day unchanged to 2bps tighter mainly due to a lack of sellers. Korea IG space stabilised post weeks of political drama. In India IG, trading activity was on the lighter side as well with spreads broadly unchanged on the day. Long-duration bonds continued to underperform with more selling while 1-5year bonds had better demand.

ASIA HIGH YIELD (HY)

New World Development was the focus in Greater China HY space. It was another day of heavy selling especially on higher cash priced perpetuals which were down 5-7 points. The company's announcement did not calm most investors' nerves. Both asset managers and private banks were sellers. In India HY, it was a risk-off session as well and the space was down 0.25-0.75point on average. We remain highly selective in the HY space as the higher for longer rates environment will pressure operating margins in this segment the most.

Forex Market Updates

The US Dollar remained strong as markets digested the Fed's monetary policy easing trajectory in 2025 and expect fewer rate cuts next year.

USD

The US Dollar hovered near its two-year high on Thursday after the Federal Reserve cut interest rates and signaled a much slower monetary policy easing trajectory in 2025. The dollar edged higher from losses early in the session after a stronger-than-expected reading on US third quarter GDP. The number validated the Federal Reserve's cautious new take-it-slow approach to easing, as did a bigger-than-expected fall in the number of applications for unemployment insurance.

The Dollar Index looks poised to stay well supported above 106.5 in the near term.

AUD

The Australian Dollar struggled to stay off two-year lows on Friday after a punishing week of losses against their U.S. counterpart cracked major support levels. The Aussie was indirectly aided by a sharp retreat in the yen as markets scaled back wagers on a January rate hike from the Bank of Japan. The resulting short squeeze sent the Aussie surging 2% overnight to stand at 98.17 yen. A soft report on Australian growth led the Reserve Bank of Australiato take a dovish turn last week, and futures now imply around a 57% chance of a quarter-point rate cut in February.

AUDUSD may continue to face downward pressure to oscillate near the lower boundary around the 0.6200 level.

GBP

The Sterling slipped and two-year gilt yields pulled back from seven-month peaks after the BoE held its key interest rate at 4.75%, as expected, but three policymakers voted to lower borrowing costs. Analysts said the surprise vote split highlighted the risks of British interest rates falling faster than anticipated next year - a development that could weigh on sterling but shore up bond markets.

Sterling looks to be testing the previous low of 1.2484 before potentially breaking lower, with the next level of support at 1.2296.

XAU

Gold prices edged higher on Thursday, erasing earlier gains after US data reinforced market expectations that the Federal Reserve will take a cautious approach to policy easing in the year ahead. Gold slipped more than 2% to a one-month low earlier in the session after Fed officials dialed back projections for future easing given stubborn inflation. The drop attracted investors to buy, sending prices as much as 1.5% higher earlier in the session.

The precious metal should remain range-bound, staying between 2560 and 2720.