Market Daily

Macro Update:

US nonfarm payroll comes in stronger than expected

The US economy added 227K jobs in November, compared to upwardly revised 36K in October. The figure was above market expectations, albeit an increase in the jobless rate to 4.2% reinforced market expectations of an 88% chance of a 25 basis point Fed rate cut this month. On the equities front, the S&P 500 and Nasdaq notched fresh highs following the upbeat payroll data on Friday. This echoes our view of strong US equities performance post US elections, and we continue to stay positive on US equities.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks rose to fresh record highs on Friday following upbeat forecasts from companies such as Lululemon and as the latest US jobs data fueled expectations for another Fed rate cut this month.

EUROPE EQUITIES

Stocks in Europe traded higher on Friday, logging a solid weekly gain, supported by a rise in luxury and auto stocks, while media and basic resources dragged.

HK EQUITIES

Hong Kong equities capped its best weekly performance in two months on Friday as investors gear up for the Chinese Economic Policy Meeting this week, hoping to see more stimulus measures from Beijing.

Lululemon (LULU US)

Shares of Lululemon jumped on Friday after it announced stronger-than-expected financial results for 3Q24, potentially signalling a turnaround for the company after experiencing its worst full-year share price performance since 2013.

Lululemon’s 3Q24 revenue was at USD2.40B vs. USD2.36B expected, while net income was at USD351.9M vs. USD335.6M expected.

The company also upgraded its full-year outlook on strong sales overseas, now seeing between USD10.45B and USD10.49B in revenue, up from between USD10.38B and USD10.48B previously.

MARKET CONSENSUS: 22 BUYS, 14 HOLDS, 4 SELLS, AVERAGE TP USD377.56

Apple (AAPL US)

Apple is reportedly preparing to launch its long-awaited series of cellular modem chips next year, which will replace components from longtime partner Qualcomm. This is a positive development to Apple’s strategy to use more in-house components in its products, which is likely to be supportive for its bottom line as well as competitive edge going forward.

Apple's new component is set to feature in the iPhone SE, the company's entry-level smartphone, which is scheduled for its first update since 2022 next year.

MARKET CONSENSUS: 39 BUYS, 18 HOLDS, 3 SELLS, AVERAGE TP USD243.25

Aviva (AV/ LN)

British insurance company Aviva announced on Friday that it reached a preliminary agreement to buy Direct Line Insurance Group for GBp275 per share, or GBP3.6B. The agreement came after Direct Line rejected a previous offer at GBp250 per share, or GBP3.3B.

The increased price of Aviva’s offer is a positive signal of management’s confidence on the amount of synergies Direct Line could bring.

The company now has until 25 December to make a firm offer which Direct Line's shareholders will have to vote on.

MARKET CONSENSUS: 10 BUYS, 3 HOLDS, AVERAGE TP GBp549.46

Airbus (AIR FP)

Shares of Airbus rose on Friday after announcing that it delivered 84 planes in November, marking a significant recovery toward its year-end goals after a slowdown in the summer months. This is likely to be supportive for the company’s share price going forward.

Airbus has now made 643 deliveries year to date, leaving it with 127 jets to deliver in December to reach its annual target of “around 770.”

MARKET CONSENSUS: 20 BUYS, 5 HOLDS, 2 SELLS, AVERAGE TP EUR162.6

SF Holding (6936 HK)

SF Holding on Friday obtained the Hong Kong Exchange’s approval regarding the spin-off of three of its projects and their respective underlying assets through an infrastructure REIT on the Shenzhen Stock Exchange.

The REIT is called Southern SF Warehouse Logistics Closed-end Infrastructure Securities Investment Fund, with China Southern Fund Management as its public fund manager.

SF’s projects planned for the spin-off include the SF Huanan Logistics Complex project located near the Shenzhen Bao'an Airport, the SF Fengtai Industrial Park project located in Wuhan, and the SF Fengtai Industrial Park project in Hefei, Anhui.

MARKET CONSENSUS: NONE

Earnings Announcements

US Market

Oracle

European Market

-

HK - China Market

-

Global Indices Changes (%)

Fixed Income Market Updates

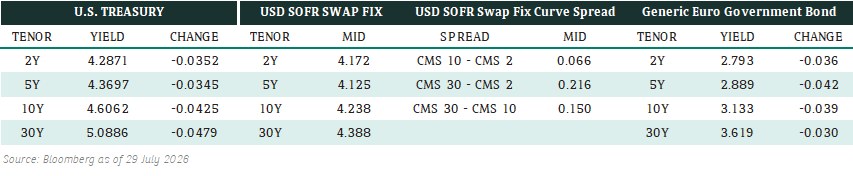

WWith the market just about cementing a 25 bps cut in December, we would be long bonds for carry going into the new year. The short-term bias is for Treasury yields to trend down and 4.1 to 4.2% for the US Treasury ten year yield. We would also be cautious on credit selection as the demand for high yield remains strong but spreads globally are at year tights.

EUROPEAN BANK COCO (AT1)

Strong week in European AT1 space which closed around 0.50 to 1 point higher on average for the week with short covering on French Banks' AT1 bonds. EUR and GBP denominated AT1 bonds were still more sought after compared to USD-denominated AT1. Although there were small profit taking towards market close, prices were largely unaffected. Valuations do not look cheap, and we would position more conservatively as we head towards year-end. However, we would not hesitate with AT1s from good credits and short dated calls.

ASIA INVESTMENT GRADE (IG)

Performance was mixed across Asia IG with flows skewed towards better selling. By the end of the week, tone turned weaker with longer duration underperforming. China and HK 5 year and shorter paper was in flavor by accounts. The focus in Korea IG last week was on the marital law. Spread initially went 15bps (basis points) wider, before stabilizing 1-4bps wider by end of the week after the reversal of the martial law order. Japan IG was 2-5bps better on the week. In the India IG space, there were better selling interest in ex-Adani names.

ASIA HIGH YIELD (HY)

In China, it was a relatively slow market, typical of December. Benchmark names such as Longfor and Vankegained 1-2 points, supported by a combination of short covering and retail demand, though overall liquidity remained thin. Outside of China, the market ended the week 25 cents higher on average, with sentiment improving as the Adani situation stabilized for now. Vedanta remained a key focus after the company’s recent $800 million issuance of new 28s and 31s, which continued to trade firm. Renewables and NBFCs (non-bank financial companies) also benefited from renewed RM demand, with benchmark names seeing steady flows.

Forex Market Updates

The US Dollar ended the week stronger on better-than-expected jobs data, but it wasn't able to fully recover its losses from the week.

USD

The US Dollar rose on Friday, amid the stronger than expected jobs report, although unemployment was slightly higher. Inflation report this week that could be pivotal on rate cut expectations later this month. This week's Consumer Prices Index will likely be the last piece of useful data for the December Fed meeting, and the path of least resistance remains for some U.S. dollar weakness, offering a great opportunity to buy the dip in early 2025.

The Dollar Index looks likely to be capped by technical resistance around 107.5 for the time being.

GBP

The British Pound was set for a third week of gains against the euro and a second against the dollar on Friday, ahead of key U.S. jobs data, and after political turmoil in France dominated market action during the week. The pound dropped from a 1-1/2-year high in October as the U.S. jobs market roared ahead and fell further in November as the re-election of Donald Trump boosted the American currency. Markets are largely pricing in that the Bank of England will hold rates unchanged at its next meeting on Dec. 19.

Sterling looks to be on an uptrend, which could continue should BoE decide not to cut rates this week and we may see GBP test the resistance of 1.2900.

CAD

The Canadian Dollar weakened against its U.S. counterpart on Friday, approaching a recent 4-1/2-year low, as a jump in Canada's unemployment rate bolstered expectations for another outsized interest rate cut this week from the Bank of Canada. Investors see a roughly 80% chance of a half-percentage-point rate cut from the BoC on Dec. 11, up from 58% before the data. It follows a cut of that magnitude in October. The threat of U.S. tariffs on Canadian imports has added to downside risk for the loonie, analysts say.

USDCAD is likely to trade upward, with previous high of 1.4177 as the next resistance level.

XAU

Gold prices inched up on Friday after an increase in expectations of a 25 basis point Fed rate cut this month following the jobs report on Friday. The prospect of rate cuts, starting with the half basis point reduction in September, has underpinned gold's record rally this year, as lower rates increase the appeal of holding non-yielding gold.

The precious metal should remain range-bound, staying between 2560 - 2700 for the time being.