Market Daily

Macro Update:

Wall Street extends selloff

Wall Street extended their recent poor momentum into the first trading day of 2025 as markets continued to assess the impact that tighter monetary policy may have on corporate returns. The case for restrictive policy by the Fed was further strengthened by strong labour data, as initial unemployment claims unexpected drop to an eight-month low, while outstanding claims fell by more than 50,000.

China’s manufacturing sector slowed in December, falling short of expectations for a faster expansion. The Caixin Manufacturing PMI edged down to 50.5 in December 2024 from November's 5-month high of 51.5. Although this was the third straight month of growth in factory activity, the data echoed earlier official reports, highlighting the limited impact of Beijing’s stimulus measures thus far while further stimulus can be expected.

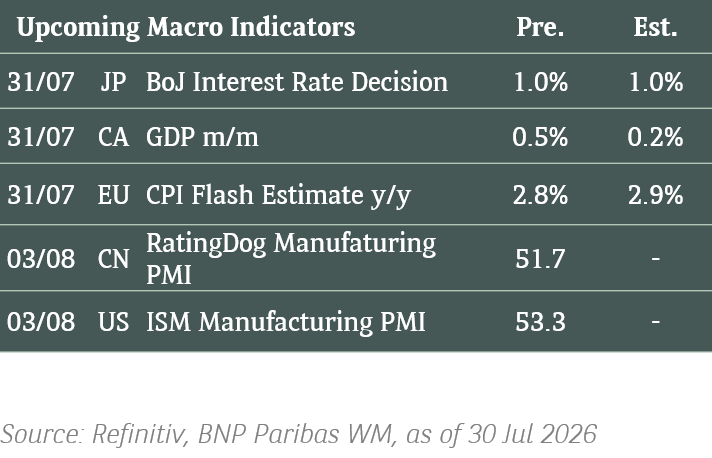

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks closed lower on Thursday amid choppy trading as well as the cross-currents of solid labour market data and a rising USD.

We nevertheless remain positive on US shares in the medium term.

EUROPE EQUITIES

European shares kicked off the first trading session of 2025 on a high note on Thursday, buoyed by a strong performance in the energy sector, while investors analysed fresh economic data from the US.

HK EQUITIES

Stocks in Hong Kong closed lower on Thursday as uncertainties on Chinese growth and US tariffs continue to subdue sentiment.

Tesla (TSLA US)

Tesla announced on Thursday that its deliveries in 4Q24 stood at 495,570 units, missing estimates at around 500,000 despite hitting a record high. This also marked Tesla’s first annual vehicle sales drop in more than a decade.

Tesla’s delivery results offer a reminder of the challenging landscape for EV makers, even as hype around driverless cars and Elon Musk’s closeness with president-elect Donald Trump have sent the company’s shares soaring in recent months.

Tesla’s stock price dropped more than 6% yesterday and could face some further volatility in the near term.

MARKET CONSENSUS: 28 BUYS, 16 HOLDS, 16 SELLS, AVERAGE TP USD294.53

Apple (AAPL US)

Apple is reportedly going to offer rare discounts of up to RMB500 on its latest iPhone models in China, a potential sign of fierce competition from rivals such as Huawei as the US tech giant moves to defend its market share in the world’s second largest economy. This could potentially hurt Apple’s China sales numbers in the near term.

The promotion, which will run between 4 to 7 January 2025, applies to several iPhone models when purchased using specific payment methods.

MARKET CONSENSUS: 39 BUYS, 18 HOLDS, 3 SELLS, AVERAGE TP USD245.95

Constellation Energy (CEG US)

Shares of Constellation Energy surged on Thursday after it has been awarded a record USD1B in contracts to supply nuclear power to the US government over the next decade, enough to fund upgrade projects that will boost capacity at the country’s biggest nuclear fleet.

This is likely to be supportive for Constellation’s top-line and thus its share price going forward.

The deal also demonstrates a growing demand for clean energy from nuclear, which should be supportive for Constellation’s peers as well.

MARKET CONSENSUS: 13 BUYS, 7 HOLDS, AVERAGE TP USD282.92

IBM (IBM US)

IBM and GlobalFoundries announced on Thursday that they have reached a settlement in their ongoing lawsuits, inclusive of breach of contract, trade secrets, and intellectual property claims between the two companies. Both firms also looked towards future collaboration.

The details of the settlement are confidential and both parties have expressed satisfaction with the outcome.

Nevertheless, the unwinding of uncertainties surrounding litigations should be supportive to both companies’ share prices in the near term.

MARKET CONSENSUS: 9 BUYS, 9 HOLDS, 5 SELLS, AVERAGE TP USD214.1

Cathay Pacific (293 HK)

Cathay Pacific announced on Thursday that it has now hit 100% of pre-pandemic flights. This applies to both its main airline as well as Hong Kong Express, providing evidence of its strong recovery since the COVID-19 pandemic.

Cathay Pacific CEO Ronald Lam also added that the group aims to operate passenger services to around 100 destinations around the world within 2025.

These developments could be supportive for Cathay Pacific’s stock price going forward.

MARKET CONSENSUS: 11 BUYS, 2 HOLDS, 1 SELL, AVERAGE TP HKD9.7

Earnings Announcements

US Market

-

European Market

-

HK - China Market

-

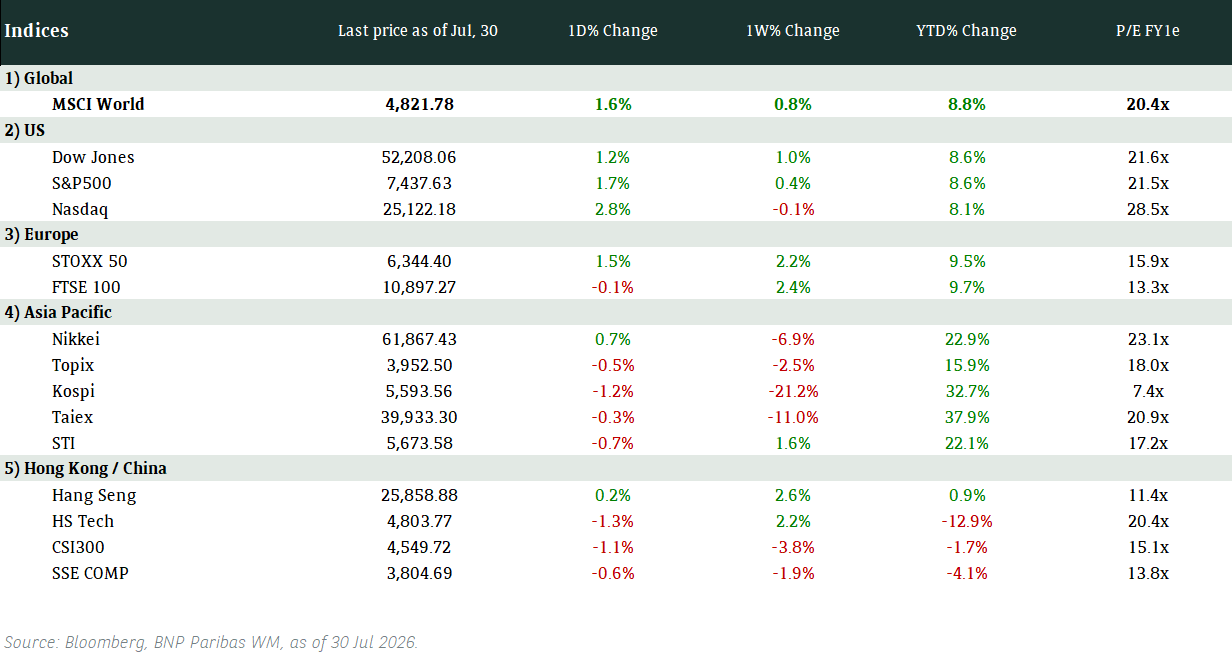

Global Indices Changes (%)

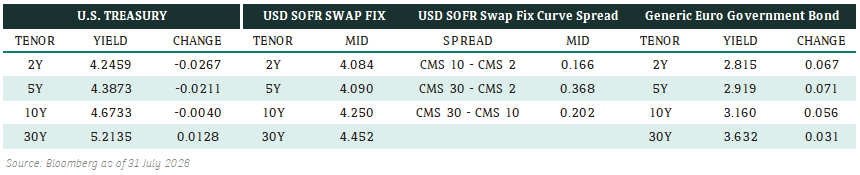

Fixed Income Market Updates

We expect 2025 returns in the fixed income space to be driven by carry. We view high beta bonds in the financials space favourably and our sweet spot is 4-7 years.

EUROPEAN BANK COCO (AT1)

European AT1 space was unchanged to 0.125 point lower in general. Risk sentiment pickup in the afternoon with a few European asset managers buying EUR-denominated AT1 bonds across the curve. Some of the AT1 bonds were already trading 30-50bps tighter month-on-month. We expect to see new issuances as soon as next week, hearing a few deals are in the pipeline according to some syndicates.

ASIA INVESTMENT GRADE (IG)

It was a slow with Japan still on holiday and no US Treasury market. However, trading picked up after London came in. Investors were picking up bonds in the 5-year bucket. In Korea, there were small buying in high beta financials and corporate bonds from both onshore and offshore asset managers. While in China, buying was largely in bonds of Chinese asset management companies such as Huarong and Cinda, as well as Chinese Central SOEs.

ASIA HIGH YIELD (HY)

It was reported that NWS Holdings is in early-stage discussions with China’s Yuexiu Group and other buyers to sell a bundle of roads in Mainland China worth about USD2bn. Market perceived this as a signal of potential support to New World Development, leading the bonds to trade up across the curve. Vanke's bonds also traded up on the day as news of some successful debt rollover helped sentiment.

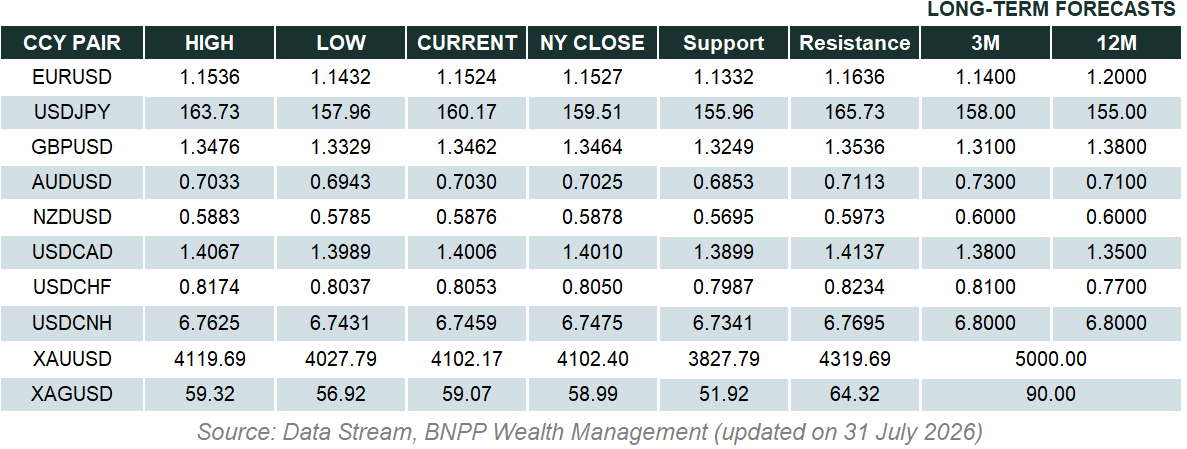

Forex Market Updates

The US Dollar soared to its highest level in two years as markets bet on a slower pace of interest rate cuts versus its global peers.

USD

The US Dollar jumped to a two-year high on Thursday in the first day of 2025 trading, building on last year's strong gains on expectations U.S. growth will beat peers and keep U.S. interest rates relatively elevated. The Federal Reserve has indicated that it will be more cautious in cutting interest rates as inflation remains stubbornly above its 2% annual target and the economy remains strong. Policies by U.S. President-elect Donald Trump are also expected to boost growth and potentially add to upward price pressures.

The Dollar Index is likely to remain well supported above 107.50 for the time being.

CNY

The Chinese Yuan hit a 14-month low on the first trading day of the year while Chinese stocks and bond yields plunged, underscoring growing worries about China's economy and a looming trade war before Donald Trump begins his U.S. presidency this month. After sliding 2.8% against the greenback in 2024 in its third straight year of losses, the onshore yuan kicked off the new year on the back foot, briefly weakening below 7.3 per dollar for the first time since Nov. 3, 2023. Meanwhile, China's stock benchmark tumbled nearly 3% on Thursday to the lowest level in more than two months, while long-dated Chinese yields slid to record lows.

The Renminbi could see more near term weakness against the USD, although strong resistance is expected around the 7.4000 handle.

GBP

The British Pound dropped to a near-nine month low against the dollar on Thursday, hurt by the U.S. currency's relentless rise on expectations of dollar-supportive policies from incoming President Trump. The larger decline for the pound is a reversal of last year's trend, when it depreciated less against the dollar than any other G10 currency. Sticky inflation and better growth early in the year meant the Bank of England was more cautious about cutting rates than its peers. This may not be the case this year, however. If we were to see the economy in the UK continue to weaken early this year, and the Bank of England started to make noises about potentially being more active in terms of cutting rates in response to that, that could certainly open the door for a weaker pound.

Sterling looks poised for a period of consolidation between 1.2450 and 1.2600 moving forward.

XAU

Gold hit a more than two-week high on Thursday, fuelled by safe-haven buying, while the market took out positions ahead of the Federal Reserve's rate outlook and the potential impact of the President-elect's proposed trade tariffs. Bullion thrives in low-interest-rate environments and acts as a hedge against economic and geopolitical risks. Traders await next week's U.S. job openings data, the ADP employment report, the Fed's December FOMC meeting minutes and the U.S. employment report to gauge the interest-rate outlook for 2025.

The precious metal could see some near term consolidation around 2660.