Market Daily

Macro Update:

Trump slaps tariffs on Canada, Mexico and China

President Donald Trump on Saturday signed an executive order imposing a 25% tariff on imports from Mexico and Canada and 10% on imported Chinese goods. The tariffs will cover all imports from the three countries, although oil and gas imports from Canada will see a smaller duty of 10%. Canadian Prime Minister Trudeau retaliated by slapping tariffs on C$155 billion ($107 billion) of US goods, while China vowed to take the case to WTO. Following the start of a new global trade war, risk of higher and stickier inflation heightened, which diminishes the prospect of more interest rate cuts from the Federal Reserve. Sentiment fell, evident from the sharp drop in US futures on Sunday evening. Volatility can be expected, and we continue to view them as opportunity.

Main Upcoming Macro Indicators

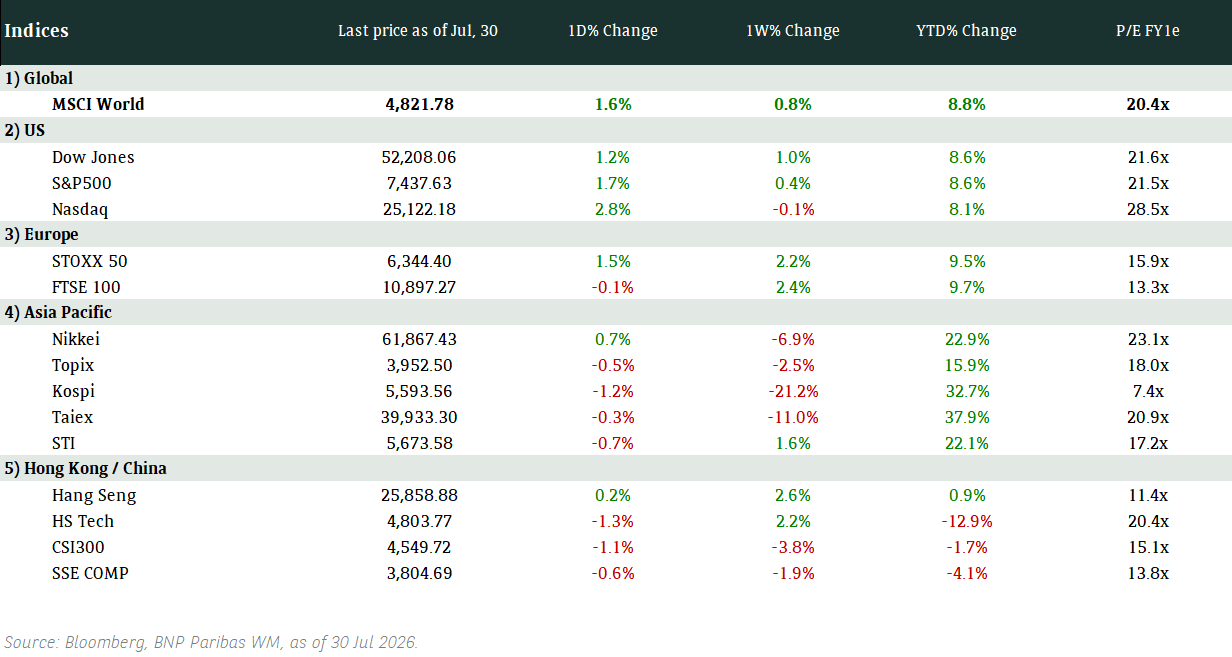

Equity Market Updates

US EQUITIES

US stocks closed lower on Friday, paring earlier gains after an announcement stating that President Donald Trump will start implementing tariffs on Saturday.

We remain positive on US equities in the medium term.

EUROPE EQUITIES

European shares closed at a record high on Friday, led by technology stocks, as robust earnings announcements overshadowed concerns over economic recovery.

HK EQUITIES

The Hong Kong stock market remain closed on Friday for Chinese New Year holiday.

Abbvie (ABBV US)

Shares of Abbvie rose on Friday after it posted 4Q24 results that beat analyst expectations, with revenue at USD15.1B vs. USD12.9B expected, and adjusted EPS at USD2.16 vs. USD2.12 expected. The company’s newer immunology drugs successfully delivered growth needed to offset declining sales of its blockbuster Humira.

Abbvie also announced an upbeat outlook of 2025, expecting adjusted EPS to come in between USD12.12 and USD12.32 for the year. CEO Rob Michael also mentioned that the company has no significant negative events for the rest of the decade, giving it a "clear runway to growth for at least the next eight years.“ This is likely to support share price going forward..

MARKET CONSENSUS: 19 BUYS, 10 HOLDS, AVERAGE TP USD204.19

Starbucks (SBUX US)

Starbucks and its union representing over 10,000 baristas have agreed to withdraw lawsuits filed against each other on Friday.

Talks between the two parties, which began in April 2024, were halted in December 2024 before a final round, with the union saying the coffee chain had yet to bring a comprehensive package to the table. Friday's decision brings the two parties a step closer to reaching a contract.

The union went on a five-day strike ahead of Christmas last year, which closed Starbucks stores in multiple cities in the US. The cooling relationship between Starbucks’ management and its union is likely to be a positive for the company.

MARKET CONSENSUS: 19 BUYS, 14 HOLDS, 6 SELLS, AVERAGE TP USD107.2

Chevron (CVX US)

Chevron stocks fell on Friday after a disappointing 4Q24 earnings report. It lost money in its refining business for the first time in four years and missed analysts' earnings expectations, with adjusted EPS coming in at USD2.06 vs. USD2.48 expected. Refining margins fell partially because Chinese drivers have been switching to EVs.

Looking ahead, the company expects its cash flow to grow by USD10B over the next two years, assuming the international oil prices are around USD70 per barrel.

Nevertheless, the hit to profitability is likely put pressure to Chevron’s share price going forward.

MARKET CONSENSUS: 19 BUYS, 10 HOLDS, AVERAGE TP USD178.04

AstraZeneca (AZN LN)

AstraZeneca has reportedly cancelled plans to invest GBP450M in a UK vaccine manufacturing plant in Liverpool, citing reduced government support as the main reason for the cancellation.

The decision reverses an announcement made by then-chancellor Jeremy Hunt at last year’s March budget that would have seen the pharmaceutical company expand its existing facility in Speke.

Further cuts in government support to the British pharmaceutical company may put downward pressure to its share price going forward.

MARKET CONSENSUS: 25 BUYS, 6 HOLDS, AVERAGE TP GBp13520.89

Samsung Electronics (005930 KS)

Shares of Samsung traded lower on Friday as earnings at its core semiconductor business weakened sequentially for a second consecutive quarter, despite posting an overall 4Q24 earnings beat at KRW7.75T.

The world's largest maker of memory chips and smartphones has said it faces challenges from sluggish demand for conventional chips and information-technology devices amid intensified market competition. It is also trying to catch up with rivals in supplying advanced artificial-intelligence chips.

How Samsung will navigate the highly competitive semiconductor market going forward will be key in determining its share price trajectory.

MARKET CONSENSUS: 34 BUYS, 6 HOLDS, AVERAGE TP KRW71578.95

Earnings Announcements

US Market

McDonald’s, Caterpillar, Palantir

European Market

-

HK - China Market

-

Global Indices Changes (%)

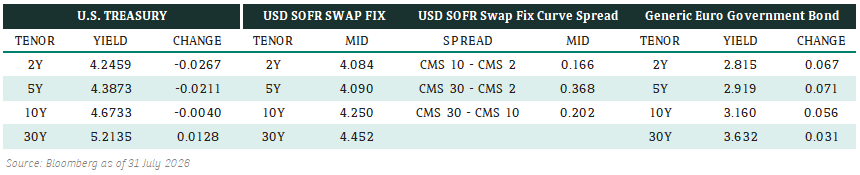

Fixed Income Market Updates

Volatility is to be expected with the recent tariff announcements. We would be adding fixed income on any dips that we expect to be short-lived.

EUROPEAN BANK COCO (AT1)

It was a firm session in European Banks AT1 space driven by rates move. Prices were up 0.25 point . Deutsche Bank also announced results and the AT1 bonds were up except for the lower reset. With the continuation of spread tightening (~5 basis points last week), we expect any further performance mainly to be driven by rates and continue to view 2028 / 2029 maturities as the sweet spot.

ASIA INVESTMENT GRADE (IG)

Trading was muted during the Chinese New Year holidays. Although credit spreads have compressed, we think spreads can continue to remain tight, driven by favourable technicals. We prefer Investment Grade bonds over High Yield and looking at how rates have rallied after the global technology stocks' sell-off, we prefer to stay in the 5-7-year duration bucket. We would be selective on Hong Kong property and bank risk.

ASIA HIGH YIELD (HY)

We are cautious of idiosyncratic risks in the High Yield space. Moreover, we do not see any near-term turnaround in the property sector in China although recent news of government support for Vanke had buoyed sentiments.

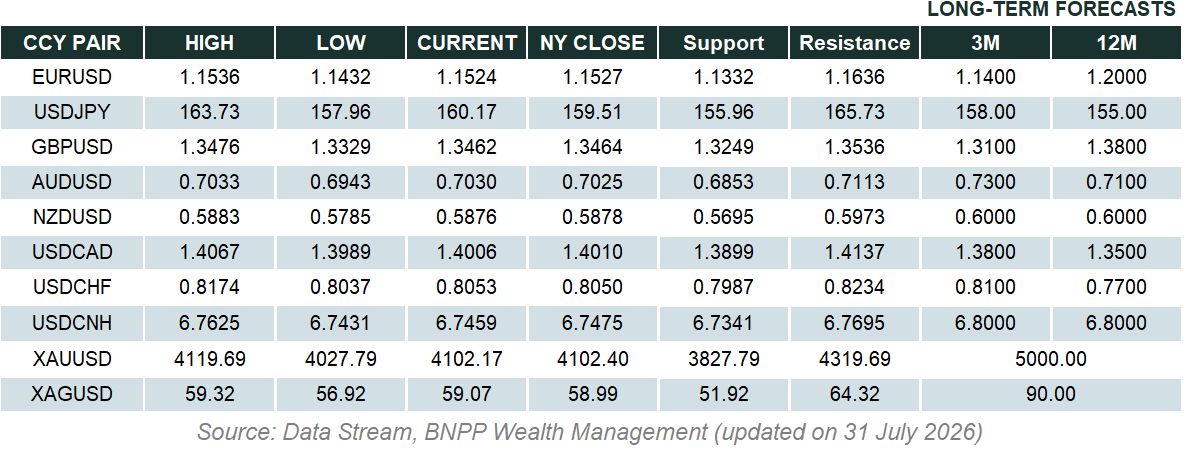

Forex Market Updates

The U.S. Dollar surged across the board, driven by safe-haven demand, fuelled by Trump's announcement of tariffs on Canada, Mexico and China.

USD

The US Dollar advanced against major currencies on Friday, while the Canadian dollar weakened and the Mexican peso edged higher after the White House reiterated that Trump will impose tariffs on Saturday. Earlier on Friday, U.S. Commerce Department data showed that the Personal Consumption Expenditures (PCE) Price Index rose 0.3% last month, the largest increase since last April, amid a surge in consumer spending, suggesting the Federal Reserve would probably be in no hurry to resume cutting interest rates.

The Dollar Index could see a another push higher on safe-haven demand, with the previous high of 110.17 as potential resistance.

CAD

The Canadian Dollar added to its monthly decline against its U.S. counterpart on Friday in volatile trading as investors braced for the expected start of U.S. tariffs on Canadian goods, including on oil which some expected to gain an exemption. For the month, the currency was down 1%, its fifth straight month of declines. That is the longest monthly losing streak since 2016. The Bank of Canada on Wednesday said that most of the loonie's decline in recent months was due to rising uncertainty around trade policies as it cut its benchmark interest rate by 25 basis points to 3% to support the economy.

The Loonie will likely weaken, with USDCAD's highest level of 1.4667 in 2020 as the next target level.

GBP

The British Pound headed for a fourth monthly loss on Friday, increasingly under pressure from investor concern about the outlook for the British economy, following January's bond market turmoil and in light of weakening UK data. Earlier last month, a selloff in global government bonds hit the UK market particularly hard, sending long-term gilt yields to their highest in decades, heaping pressure on finance minister Rachel Reeves. Yields have since retreated and sterling has recovered some stability, but a recent run of macro data has pointed to an economy that is slowing rapidly, with unemployment rising, falling consumer spending and weakening business activity. The Bank of England is expected to deliver another quarter-point rate cut next week and may indicate it has room to lower borrowing costs further, if inflation continues to moderate.

The Sterling may again test the resistance level of 1.2300 as the dollar strength continues.

XAU

Gold prices surpassed the key $2,800 mark for the first time on Friday, fueled by a rush to safety following U.S. President Donald Trump's tariff threats, which heightened concerns about global economic growth and inflationary pressures. Bullion, a preferred asset during times of economic and geopolitical turmoil, is on track to record its best monthly performance since March 2024, rising nearly 7% so far. The metal surpassed multiple record peaks last year.

The precious metal is again reaching new highs and should find some consolidation around the 2800 level before strengthening further.