Market Daily

Macro Update:

Wall Street tumbles amid tariff threats and inflation concerns

Markets declined on Friday after reports suggested President Trump was considering reciprocal tariffs, which could lead to higher rates on US trading partners. On Sunday, Trump also talked about imposing tariffs on all steel and aluminium imports. Meanwhile, expectations of a Fed rate cut were delayed as the jobs report continued pointing to a solid labour market, supporting the Fed’s stance to keep interest rates steady for now. Unemployment rate unexpectedly fell to 4%, and wage growth accelerated to 0.5%, offsetting the slowdown for payrolls which came in below expectations at 143K. Adding to investor anxiety, the Michigan Consumer Sentiment unexpectedly dropped and inflation expectations for the year ahead soared. Looking ahead, this week's CPI and PPI reports should provide further insight into inflation trends.

Main Upcoming Macro Indicators

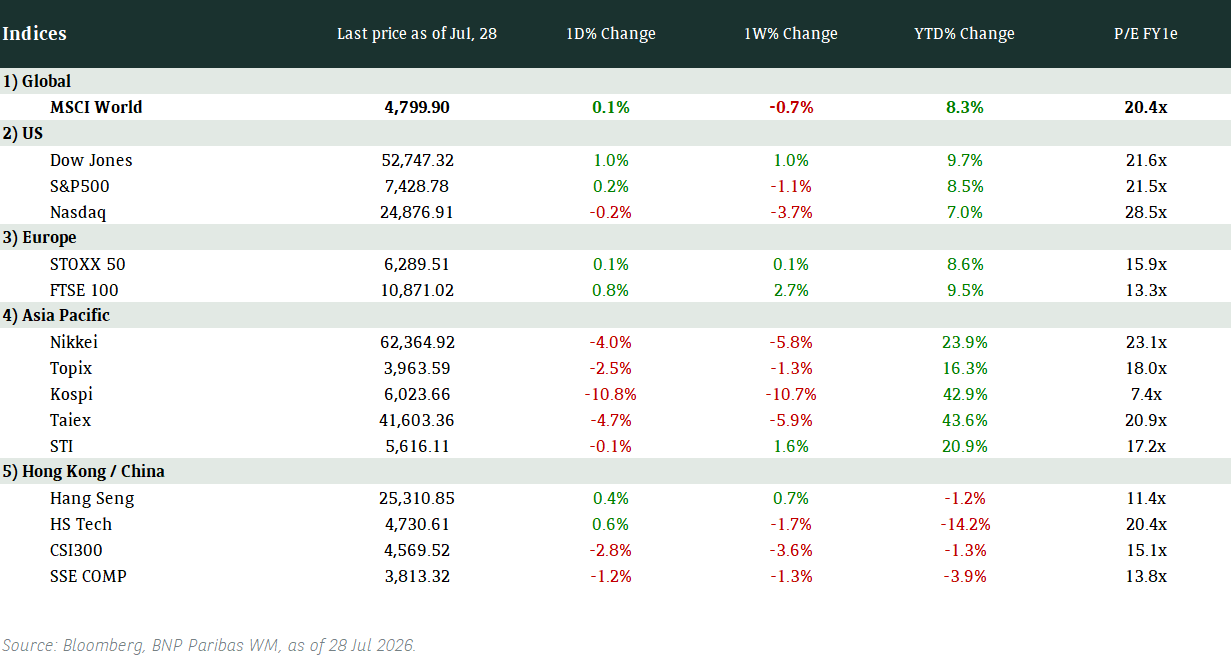

Equity Market Updates

US EQUITIES

US stocks closed lower on Friday as investors digest the latest developments on US trade policy.

We nevertheless remain positive on US equities in the medium term.

EUROPE EQUITIES

Stocks in Europe also fell on Friday, with automakers among top decliners as investors grew skittish on worries of a global trade war escalating.

HK EQUITIES

Hong Kong stocks rose on Friday led by a strong performance in AI shares as home-grown startup DeepSeek's success boosted investor sentiment.

Apple (AAPL US)

The UK Office of the Home Secretary have reportedly issued a directive requiring Apple to provide unrestricted access to all user data uploaded to the cloud worldwide.

If Apple complies with the order, it would mark a major setback for tech companies striving to avoid being used as government surveillance tools against their users.

The directive would invoke the UK's Investigatory Powers Act of 2016, granting law enforcement the authority to compel tech companies to assist in collecting evidence when necessary. Apple will have the option to appeal the capability notice to a confidential technical panel, but the law does not allow the company to delay compliance while the process is underway. This could impact Apple's operations and reputation in Europe going forward.

MARKET CONSENSUS: 35 BUYS, 17 HOLDS, 6 SELLS, AVERAGE TP USD251.03

Stellantis (STLAP FP)

Stellantis on Friday said it deepened collaboration with Mistral AI to integrate AI across multiple areas, from vehicle engineering to in-car experiences.

The two firms have worked together for over a year on projects such as vehicle engineering, fleet data analysis, internal car sales, and manufacturing.

Stellantis said Mistral's expertise in large language models is helping quickly analyze large datasets to improve manufacturing quality and reduce development times. Meanwhile, Mistral's latest initiative is an AI-powered in-car assistant serving as a voice-enabled user manual for drivers.

Further innovations resulting from this collaboration could support Stellantis’ share price going forward.

MARKET CONSENSUS: 13 BUYS, 18 HOLDS, 4 SELLS, AVERAGE TP EUR14.54

Uber Technologies (UBER US)

Shares of Uber soared on Friday after billionaire hedge fund manager Bill Ackman disclosed a share stake of roughly USD2.3B in the company that started in early January 2025, calling it one of the "best-managed" businesses globally.

Ackman specifically stated that Uber is now trading at a massive discount to its intrinsic value, despite the company trailing the S&P 500 in 2024 amid worries about the threat of autonomous vehicles. How Uber navigates this competitive landscape will be key to its share price trajectory.

MARKET CONSENSUS: 51 BUYS, 9 HOLDS, AVERAGE TP USD88.82

DBS Group (DBS SP)

Singapore’s largest bank, DBS, on Friday reported 4Q24 results that met analyst expectations, buoyed by wealth fees and gains in lending as the bank also announced a capital return plan.

The bank’s 4Q24 revenue stood at SGD5.5B vs. SGD5.48B expected, while adjusted net income was at SGD2.62B vs. SGD2.63B expected. It is also set to pay SGD0.15 per share in dividends per quarter throughout 2025 while expecting payouts of around the same amount in the subsequent two years. This is likely to support DBS’ share price in the near term.

MARKET CONSENSUS: 11 BUYS, 9 HOLDS, AVERAGE TP SGD46.1

Lenovo (992 HK)

Shares of personal computer maker Lenovo jumped to its ten-year high as media on Friday reported the company is exploring more in-depth cooperation possibilities with DeepSeek.

Tech companies are on hopes that incorporating DeepSeek's AI model into their offerings would fuel business growth, Lenovo is possibly set to benefit as consumers replace PCs with AI PCs.

While the optimism over China's AI development has largely helped shrug off the impact of Trump's additional 10% tariff on Chinese imports, this will remain the key to watch going forward.

MARKET CONSENSUS: 30 BUYS, 2 HOLDS, AVERAGE TP HKD12.41

Earnings Announcements

US Market

McDonald's, ON Semiconductor, Rockwell Automation

European Market

-

HK - China Market

-

Global Indices Changes (%)

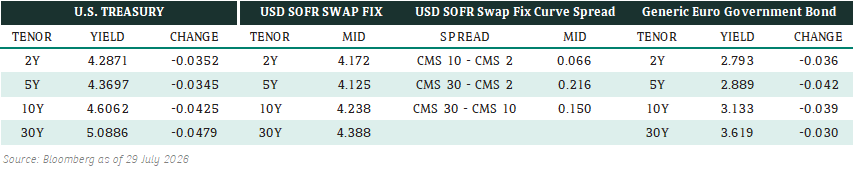

Fixed Income Market Updates

Expect rates volatility with Powell's testimony, CPI and PPI data this week. We would be extending duration if yields are higher on the back of these, which is likely the case. We also like AT1s with strong technicals.

EUROPEAN BANK COCO (AT1)

AT1 close the day about unchanged. UBS were weaker as loose hands sold their new 7% and 7.125% At1 with some switching on its curve. Over the week, we are closing about 0.25pts higher, with French names outperforming thanks to the move on Socgen (up 0.875pts on the week) with its good earnings results. Canadians underperformed, thanks to ongoing tariff worries and recent issuance. The large size of the UBS books (28.5bn for a 3bn deal) and the pricing they achieved helped remind the market how deep the bid is for GSIB AT1 paper. Expect to see more issuance next week after the slew of results this week.

ASIA INVESTMENT GRADE (IG)

Flows in the Asia IG markets were mixed following the rally in rates. Investors continued to add risks within 5-10 year bucket while some took profit on longer dated bonds. Asia IG sovereign and quasi’s was generally muted with players sidelined ahead of key data. Spreads are unchanged to a touch wider while flows were slightly skewed to better selling. Activity has been mostly on 10y paper and benchmarks while long ends continue to see bidding interest albeit in a more cautious fashion. Valuations are stretched especially for pockets such as Korean IG but the market bias is to remain long. Macro will be the biggest driver of IG credit given the spread levels.

ASIA HIGH YIELD (HY)

Risk tone in Asia HY markets remained firm. Vedanta bonds trade marginally better, while Adani complex was offered in the short end and better bid in the belly. Among peripheral sovereign, Sri Lanka continues to be better bid and Pakistan bonds also marked slightly higher on overnight demand. In China HY, Vanke is up 1-2pts (points) in the morning session as better buying from real money and fast money. Rest of the complex generically unchanged to slightly higher with flows relatively light.

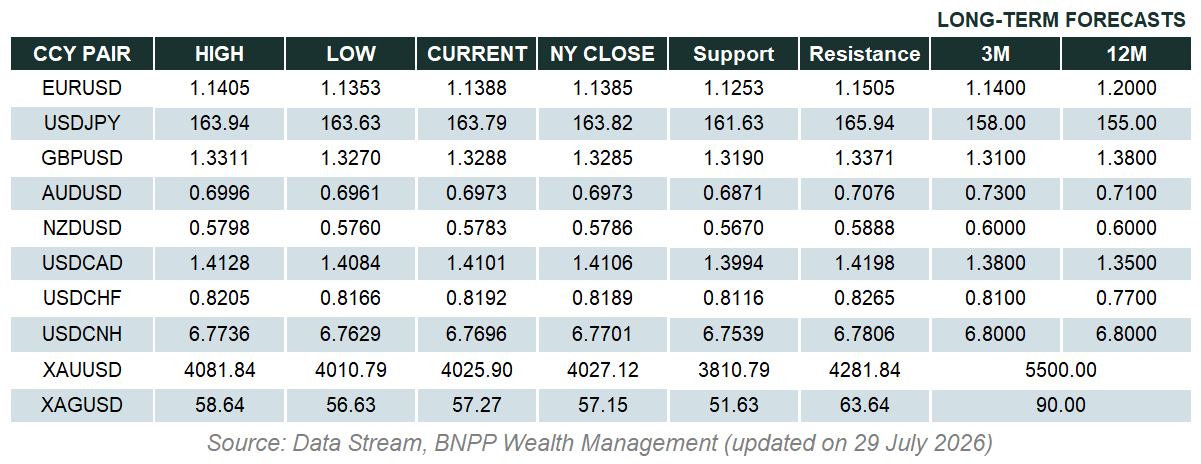

Forex Market Updates

The US Dollar posted gains to close the week on mixed US employment data and fresh tariff threats from US President Trump.

USD

The US Dollar rose against a basket of other major currencies in choppy trading on Friday after a mixed US payrolls report that showed slower employment growth in January but also a drop in the unemployment rate to 4.0%, which markets anticipate should allow the Fed to hold off on rate cuts until at least June. Following the data, Fed officials said that the US jobs market is solid and noted the lack of clarity over how US President Trump’s policies will affect economic growth and still-elevated inflation, underscoring their no-rush approach to policy easing. Elsewhere, investor nerves about global trade wars returned on Friday after Trump pledged to impose more tariffs as part of a broad effort that he said could also help solve US budget problems.

The Dollar Index could see some near term consolidation between 107.00 and 109.00.

GBP

The British Pound fell for the second straight day to close the week, although losses were limited after BoE Governor Bailey commented that markets should not read too much into a switch by some policymakers to vote for deeper rate cuts at last Thursday’s policy meeting. Following the central bank’s latest set of forecasts which projected inflation would now peak at 3.7% this year, some analysts say that the BoE “has a tough road ahead if it is to avoid potential stagflation”. On the data front, UK house prices rose more than expected last month as some buyers rushed to complete sales before an increase in property purchase taxes at the start of April, although the figures did little to move Sterling.

Sterling is poised to see some more weakness moving forward with immediate support around 1.2325.

CAD

The Canadian Dollar strengthened against its US counterpart on Friday to record its best weekly performance in 23 months, thanks in large part to domestic employment data that came in much stronger than expected. Canada’s economy added 76k jobs in January, comfortably eclipsing forecasts for a gain of 25k, with the unemployment rate also unexpectedly falling to 6.6%. Analysts say that while this should, on paper, lower the likelihood of the BoC cutting rates again in March, the central bank could still choose to err on the dovish side of caution thanks to tariffs that are still scheduled to kick in next month.

Given the strength of the recent retracement, USDCAD could be due for a near term rebound towards 1.4360.

XAU

Gold prices notched their sixth consecutive weekly gain as escalating trade tensions between the US and China fueled safe haven demand for the precious metal, with uncertainty in regard to the Trump administration’s tariff policies likely to be the central focus of the gold market for the foreseeable future. According to some analysts, the gold market also seems to have been buoyed by both continued growth in the PBoC’s holdings of bullion and a new Chinese program allowing insurance funds to invest in the precious metal.

Given ongoing uncertainties in the global trade environment, gold prices look likely to test the 2900 handle moving forward.