Market Daily

Macro Update:

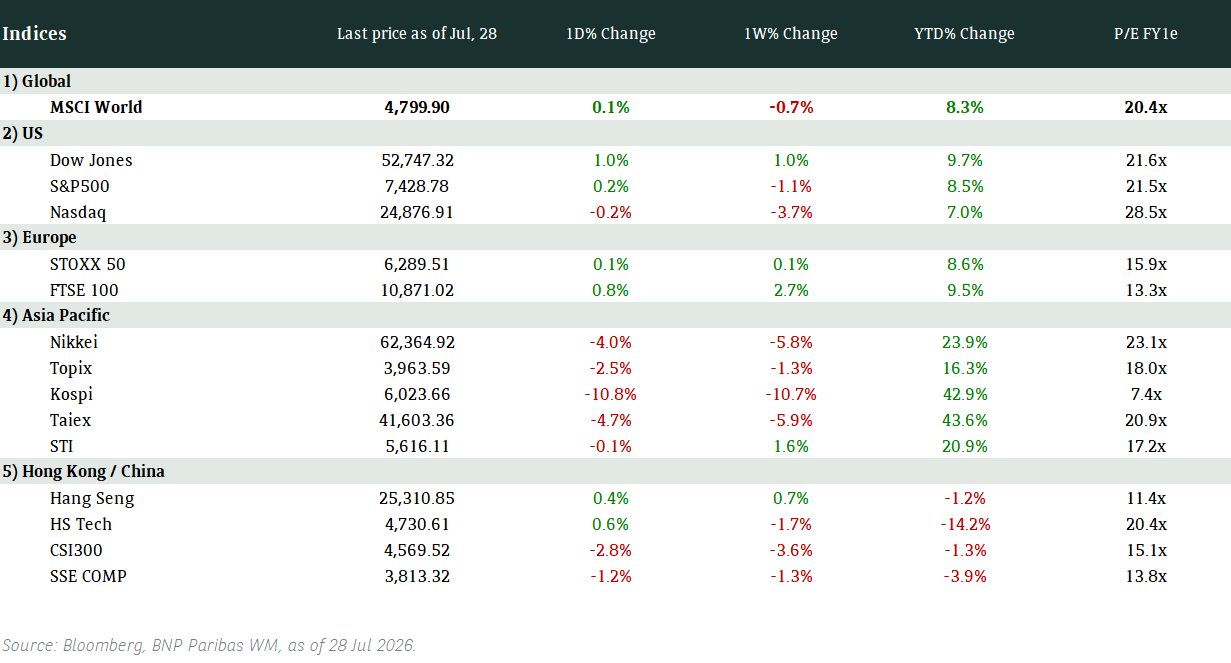

Equities tumble as yield rises after US CPI data

Inflation in the US came in hotter-than-expected for January, jeopardising the outlook that the Fed will cut rates this year. Headline inflation unexpectedly rose to 3% in January, while the core gauge was much higher than expectations at 3.3%. The market is now firmly pricing in a 25 bps reduction in the fed funds rate for 2025, while the 10-year Treasury yield surged to over 4.65%, which pressured the equity market. Nonetheless, we remain positive on global equities, and continue to like the US, with a preference for small/mid-caps as well as the non-megacaps and value sector.

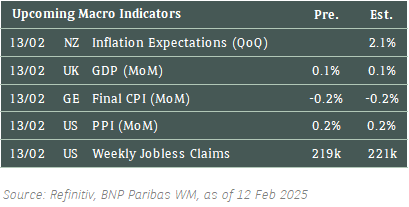

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US equities ended lower on Wednesday after a hotter-than-expected US inflation reading added to worries that the Fed would not cut interest rates anytime soon.

EUROPE EQUITIES

Shares in Europe continued to move higher on Wednesday as investors cheered upbeat earnings reports despite some caution around US inflation data.

Despite the rally so far, European equities still trade at reasonable valuations. We favour UK stocks in particular.

HK EQUITIES

Hong Kong stocks rallied on Wednesday, led by tech and property shares, as the market was fueled by AI-driven revaluation opportunities and optimism that China authorities may help indebted property developers.

CVS Health (CVS US)

CVS surged by almost 15% on Wednesday after it announced 4Q24 results that comfortably beat Wall Street estimates, boosted by lower-than-expected costs in its Aetna insurance unit. The company’s 4Q24 revenue stood at USD97.71B vs. USD97.21B expected, while EPS was at USD1.30 vs. USD0.53 expected.

CVS has recently been trying to turn around its drugstore chain and insurance business, where profit has been hit by underpricing of plans and cuts to quality ratings that help determine payments from US health programs. CEO David Joyner mentioned that this recovery will take years, but recent results show that it is moving in the right direction. This is likely to be supportive to the company’s share price.

MARKET CONSENSUS: 20 BUYS, 9 HOLDS, AVERAGE TP USD66.69

Cisco (CSCO US)

Shares of Cisco jumped in after-market trading on Wednesday after it provided an upbeat sales forecast for its current quarter, expecting revenue of between USD13.9B to USD14.1B, driven by accelerated spending on computing infrastructure and AI technology.

The company also posted top- and bottom-line beats in its FY2Q25 results, with revenue at USD13.99B vs. USD13.87B expected, while EPS stood at USD0.61 vs. USD0.56 expected.

This provides further evidence that momentum remains strong for Cisco, likely supporting its share price going forward.

MARKET CONSENSUS: 26 BUYS, 6 HOLDS, AVERAGE TP USD74.19

Siemens Energy (ENR GR)

Siemens Energy said on Wednesday that its net income for the FY1Q25 plunged, while revenue rose YoY.

Siemens Energy's order book has grown by more than a third over the past years, driven by global efforts to decarbonize power production as well as a surge in electricity demand to supply data centers needed to power AI.

The company anticipates an 8% to 10% growth in revenue in FY2025, while net income is expected to be at the break-even level.

MARKET CONSENSUS: 15 BUYS, 7 HOLDS, 5 SELLS, AVERAGE TP EUR54.58

Baidu (9888 HK)

Baidu reportedly plans to launch the next version of its AI model in 2H25.

The upcoming Ernie 5.0 model will reportedly feature big enhancements in multimodal capabilities, enabling it to process and transform diverse types of data more efficiently.

Baidu introduced its Ernie chatbot in Mar 2023, making it the first major Chinese tech firm to release a generative AI model for conversations. In late 2023, Baidu made Ernie publicly available through app stores and its website.

The company previously claimed that Ernie had outperformed OpenAI's ChatGPT in key tests, but interest in advancing AI models had only grown since.

MARKET CONSENSUS: 25 BUYS, 9 HOLDS, AVERAGE TP HKD103.81

Softbank Group (9984 JP)

Japanese technology investor SoftBank Group booked a surprising net loss of USD2.4B in 4Q24 as valuations at its Vision Fund investment arm fell.

In particular, SoftBank was hit by unrealised valuation losses for South Korean e-commerce platform Coupang, Chinese ride-hailing firm Didi Global and AutoStore Holdings.

Vision Fund 1 has had a gross gain of USD21.6B since its inception in 2017 while Vision Fund 2, which covers a broad suite of earlier-stage startups, has logged a USD22.2B loss since 2019.

The result will further raise questions about how SoftBank will fund one of its most ambitious undertakings - a hefty investment in OpenAI, which will be key to watch going forward.

MARKET CONSENSUS: 17 BUYS, 6 HOLDS, AVERAGE TP JPY11663.06

Earnings Announcements

US Market

Palo Alto, Datadog, Duke Energy, Applied Materials

European Market

Siemens, Unilever, Barclays, Commerzbank, Moncler

HK - China Market

Hua Hong Semiconductor

Global Indices Changes (%)

Fixed Income Market Updates

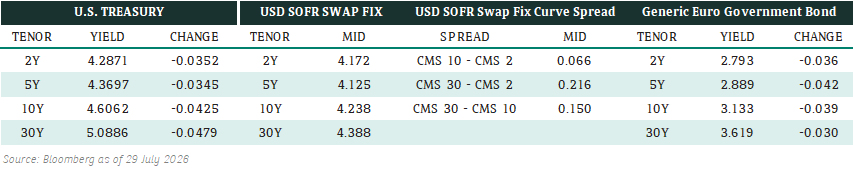

WWith a relatively steep yield curve and a healthy pullback in the 10-year Treasury following Powell’s speech, this present a good entry point to extend duration to 5 to 10-year IG bonds to lock in favourable all-in yields.

EUROPEAN BANK COCO (AT1)

European bank coco market flow was more balanced. Bond prices were generally unchanged. However, we expect the space will remain volatile as soon as there is any update on tariff around Mexcio, Canada and China. Any sell-0off would be a good opportunity to add exposure given our constructive view on Euroepan bank’s credit fundamental.

ASIA INVESTMENT GRADE (IG)

Asia IG was firm. China IG credit spread was 2-3 basis points tighter. South East Asia IG Was also firm with spread 2-4 basis points tighter. Japan had a quiet session due to local holiday but was also 1-2 basis point tighter. Overall, market sentiment has improved for IG after Bessent discussed his plan to lower the 10-year US Treasury yield. We expect the positive momentum will continue.

ASIA HIGH YIELD (HY)

Asia HY had a good day. Chian HY sentiment turned positive after Vanke secured USD 384 mil loan from its major shareholder Shenzhen metro. The entire curve weas 2-4 points higher. New World Development was also 1-2 point higher as we saw some hedge fund started to cover short. Overall, the China HY bond market has shifted back to a yield-chasing tone, but we remain cautious that the tone can change on the back of any negative tariff headline news.

Forex Market Updates

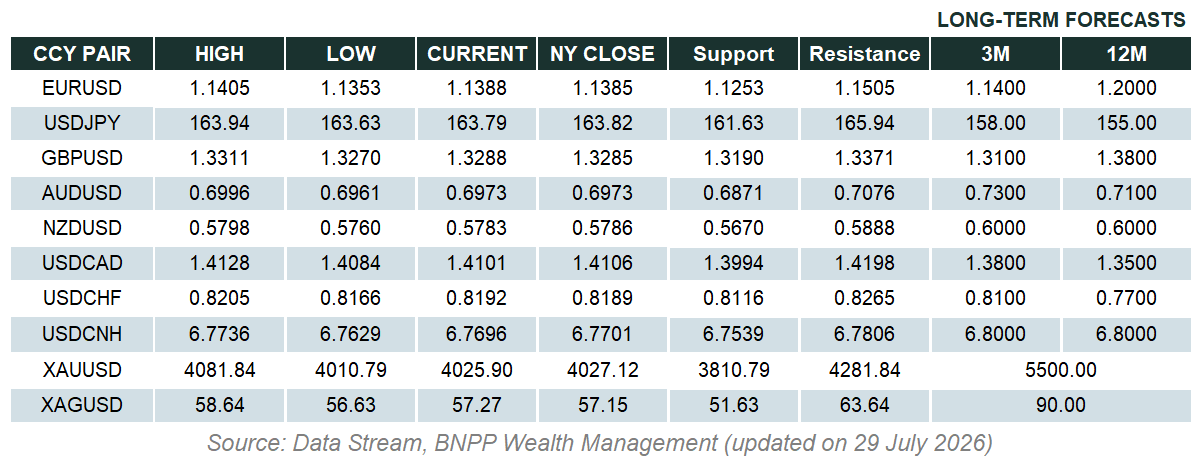

The US Dollar weakened as markets reassessed Fed policy despite strong inflation data, with traders scaling back rate hike bets and Powell emphasizing the 2% inflation target.

USD

The US Dollar weakened on Wednesday against a basket of other major currencies as markets adjusted expectations for the Fed’s policy path despite stronger-than-expected US inflation data. January’s consumer price index rose 0.5% month-on-month, while core CPI climbed 0.4%, both above forecasts. Annual inflation hit 3.0%, compared to expectations of 2.9%, while core inflation rose 3.3% versus a forecasted 3.1%. However, traders scaled back Fed rate hike bets, with interest rate futures now implying a more cautious outlook. Fed Chair Powell reiterated that inflation must trend closer to 2% before cuts are considered. Tariff risks also remain a key concern.

The Dollar Index could see some consolidation between 107.00 and 109.00 moving forward.

JPY

The Japanese Yen weakened yesterday, as markets reacted to BoJ Governor Ueda’s remarks. He warned that food price inflation could persist, influencing consumer expectations, while reiterating that future rate hikes would depend on economic conditions. Ueda confirmed a mid-year review of the BoJ’s bond tapering plan, with adjustments expected beyond April 2026. The central bank remains cautious, balancing inflation risks with economic stability. Meanwhile, Japan is seeking exemptions from US steel and aluminium tariffs, adding to trade uncertainties. Investors continue to watch for signs of policy shifts that could impact yen movements.

USDJPY’s recent rebound is likely to run into stiff resistance around 156.25 moving forward.

GBP

The British Pound weakened against the Dollar on Wednesday as markets reacted to National Institute of Economic and Social Research's (NIESR’s) latest forecasts. The think tank projected solid UK growth and easing inflation but noted limited scope for further BoE rate cuts. It expects inflation to average 2.4% this year, lower than the BoE’s forecast. NIESR also predicts fiscal challenges ahead, with the government facing long-term debt pressures. Meanwhile, UK growth is expected to pick up in 2025, supported by increased government spending. Investors remain cautious about the BoE’s monetary policy outlook, with markets closely watching economic data for signs of future rate adjustments.

Sterling looks to be facing a period of consolidation, above technical support around 1.2160 for now.

XAU

Gold surged on Wednesday, nearing record highs as U.S. tariff concerns fueled safe-haven demand. Gold closed at $2,903.96 per ounce, driven by investor fears over supply disruptions and economic uncertainty. Despite strong gains, some analysts warn of potential headwinds, including easing liquidity pressures and weakening physical demand in key markets like India and China. Gold’s Comex premium has narrowed, signaling potential stabilization. While some see room for a breakout toward $3,200, others expect a pullback if risk appetite diminishes. Market focus remains on tariff developments and central bank demand, which could shape gold’s next move.

The bullion outlook continues to point upward, with gold prices likely to be well-supported above 2780 for the time being.