Market Daily

Macro Update:

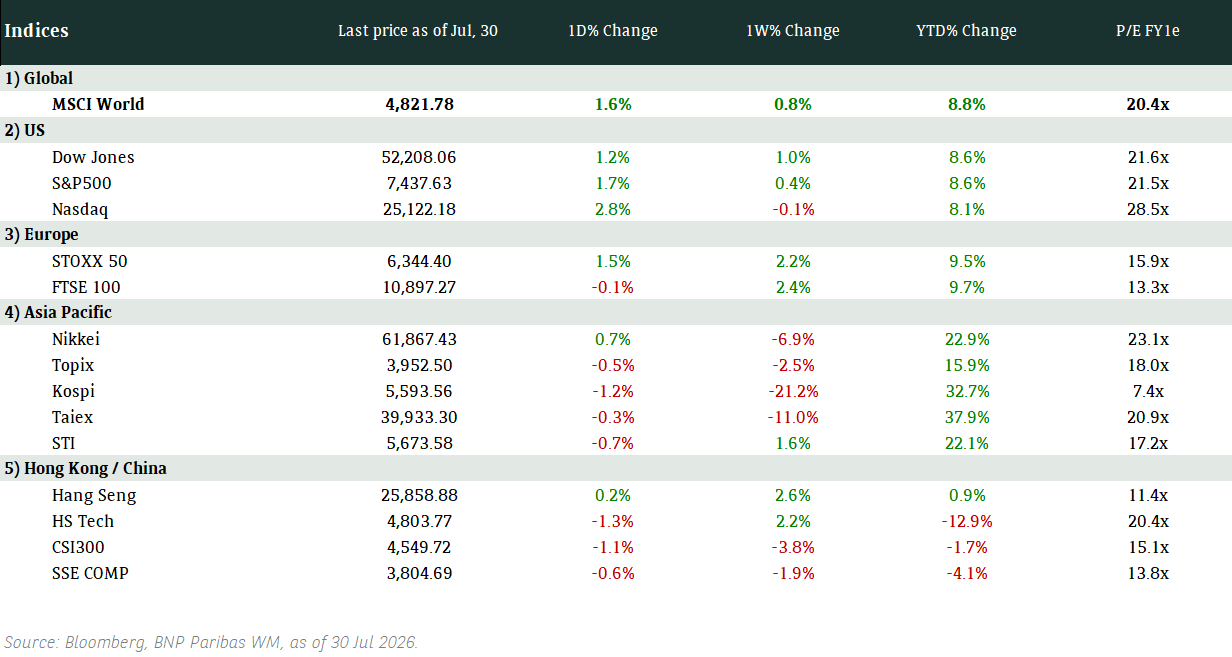

US stocks rally after the Fed keeps two rate cuts projections for 2025

The Fed held rates steady, but slowed the pace of its balance sheet run-off (quantitative tightening). It also lowered its growth projections and lifted its inflation projections slightly. Chair Powell said in a press conference that he expects inflation impacts from tariffs will likely be “transitory” while recession risks remain low. US stocks closed higher after the Fed signalled two rate cuts are still in the cards for 2025, which is in line with our forecast.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US equities rebounded on Wednesday after comments from the Fed fuelled optimism around interest rate cuts this year.

EUROPE EQUITIES

European stocks were slightly higher on Wednesday after logging gains in the previous session when Germany inched closer to plans for a massive spending surge, while investors kept a close eye on the Fed’s interest-rate decision.

HK EQUITIES

Hong Kong stocks closed flat on Wednesday as investors weighed profit-taking from the recent tech rally against the potential effects of Beijing’s measures to stimulate consumption.

We remain positive on HK/China equities in the medium term.

Tencent (700 HK)

Chinese technology giant Tencent posted on Wednesday a 11% rise in 4Q24 revenue, driven by growth in its gaming business.

Tencent, the world's largest video game company and operator of the WeChat messaging platform, reported revenue of RMB172.4B for 4Q24, vs. RMB168.7B estimate from analysts.

Tencent's domestic gaming business has shown robust recovery since mid-2024, bolstered by successful launches including "Dungeon & Fighter Mobile" and "Delta Force".

For the quarter, domestic gaming revenue rose by 23% to RMB33.2B, while international gaming revenue climbed 15% to RMB16B.

The resilience is likely to provide support to the company’s share price in the near term.

MARKET CONSENSUS: 70 BUYS, 3 HOLDS, AVERAGE TP HKD547.37

Anta Sports (2020 HK)

Shares of Anta fell on Wednesday after it reported lower-than-expected operating profit margin for 2024, narrowing by 2.3 ppts YoY to 21.4% in 2H2024 vs. 22.1% expected.

The company’s margin drag can mostly be attributed to steeper-than-expected selling expenses, which could potentially ease going forward as the cessation of its Chinese Olympics Committee sponsorship spurs related cost savings throughout 2025.

Anta’s 2024 revenues beat market estimates at RMB70.8B vs. RMB69.4B expected. It also raised its final dividend amount to HKD1.18 per share for 2H2024.

MARKET CONSENSUS: 53 BUYS, 3 HOLDS, AVERAGE TP HKD112.11

HSBC (5 HK)

HSBC is reportedly in advanced talks to sell its German fund administration business, which has about EUR400B in assets under administration, to BlackFin Capital Partners as part of its recent corporate restructuring push. The potential deal came after a string of sales by HSBC Europe and North America as it seeks to focus on its core operations in Asia.

How HSBC’s recent corporate strategy adjustments will translate to its financial performance will be closely watched by the market in the coming quarters.

Fund servicing businesses like HSBC’s Inka help clients including pensions and insurance companies manage their investment mandates across asset classes while helping to monitor performance and sustainability.

MARKET CONSENSUS: 15 BUYS, 8 HOLDS, 3 SELLS, AVERAGE TP HKD96.05

Ping An Insurance (2318 HK)

Chinese insurer Ping An on Wednesday reported solid 2024 results with operating profit after tax growing by 9.1% throughout the year, led by strong P&C and Asset Management recovery. The company’s new business value was also 29% higher in 2024, driven by solid margins.

Ping An’s 2024 revenue stood at RMB1.14T vs. RMB1.11T expected, while adjusted EPS was at RMB7.16 vs. RMB7.33 expected.

Looking ahead, a potential recovery of the Chinese economy and stock market should be supportive for the company’s performance.

MARKET CONSENSUS: 23 BUYS, 1 HOLD, AVERAGE TP HKD60.61

Pfizer (PFE US)

Drugmaker Pfizer has sold its entire stake in Haleon for about GBP2.5B to institutional investors and the consumer healthcare firm at GBp385 per share, a bookrunner for the deal said on Wednesday.

Under the deal, Sensodyne maker Haleon has agreed to buy back 44M shares from Pfizer, currently its largest shareholder, with 618M shares being sold to institutional investors.

The total sale represents 7.3% of the issued share capital of Haleon, which was created by the merger of GSK and Pfizer's consumer healthcare businesses in 2019.

Following Pfizer’s disposal, Blackrock will become Haleon’s largest shareholder with a more than 5% stake.

MARKET CONSENSUS: 13 BUYS, 12 HOLDS, 1 SELL, AVERAGE TP USD31.09

Earnings Announcements

US Market

Accenture, Lennar

European Market

Prudential

HK - China Market

Henderson Land, CK Hutchinson, CK Asset

Global Indices Changes (%)

Fixed Income Market Updates

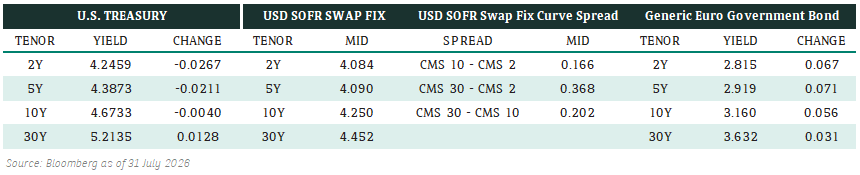

Indonesia’s Finance Minister Indrawati has said she is not resigning from her role and that Indonesia’s state revenues are showing improvement as of March 2025. Price movements of Indonesia sovereigns and quasi-sovereigns bonds were more measured compared to equity markets.

EUROPEAN BANK COCO (AT1)

European Bank AT1 space closed the day relatively unchanged with decent flows in Asia and Europe. Trading volume was decent especially in AT1 bonds with shorter call dates as well as AT1 bonds with low reset spreads. We remain of the view that some AT1 bonds' valuations are on the expensive side and would be profit-takers on those bonds.

ASIA INVESTMENT GRADE (IG)

Pressure was off in Indonesia sovereign and quasi-sovereign space as the stock market stabilised and the finance minister came out assuring markets. There were better buying flows from the US overnight. Bonds across the Indonesia sovereign and quasi-sovereign curves were unchanged to 0.25point higher. Main activity in Asia IG space was trading the Bangkok Bank new issue where the existing tier 2 bonds widened 5bps after Bangkok Bank printed a larger size and tighter spread than expected. The new issue initially traded wider when market open before private banks came in to bring spread back to reoffer level.

ASIA HIGH YIELD (HY)

China HY property space traded unchanged to 1 point lower. There were selling seen on names such as Vanke from hedge funds. New World Development bonds were 1-1.5point higher while the perpetuals outperformed compared to bullets. Outside of China, there was some bottom fishing in Indonesian HY names as equity market stabilised. In India, Adani complex traded broadly unchanged although there was slight underperformance in longer-dated bonds.

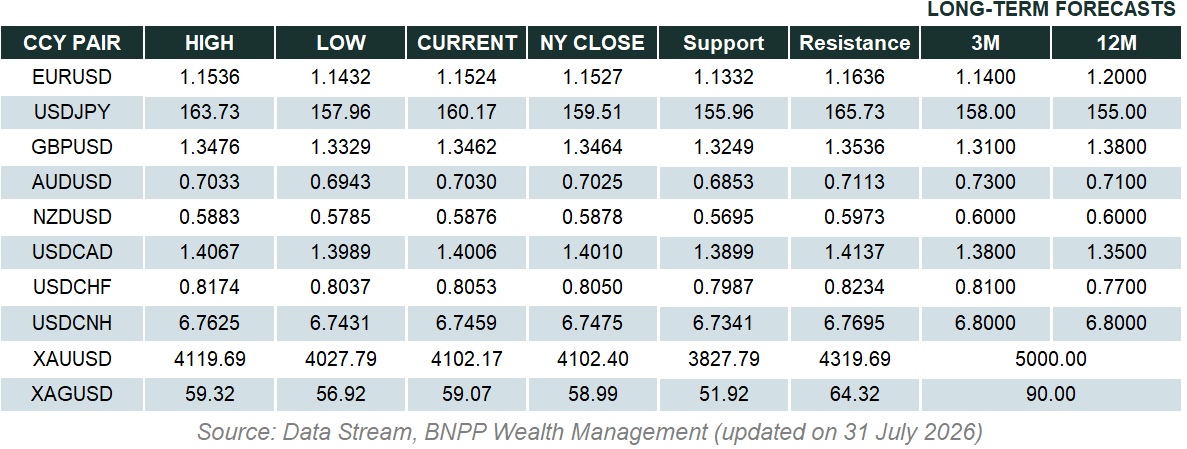

Forex Market Updates

The dollar trimmed gains after the Fed maintained its policy rate at the current level but signaled potential 50 bps rate cuts later this year, while also projecting slower growth and rising inflation.

USD

The US Dollar pared gains against the euro on Wednesday, after the Fed held interest rates steady as expected, but indicated policymakers expect to cut borrowing costs by half a percentage point by the end of this year while they also forecast slower economic growth and higher inflation. The Fed also plan to slow the ongoing drawdown of its balance sheet, known as quantitative tightening. Analysts expect the dollar to be trading within a range until the announcement of first-quarter GDP data, which can indicate whether the economic weakness is fully materializing.

The Dollar Index could see some consolidation between 103.20 and 104.00 moving forward.

AUD

The Australian Dollar took a breather on Wednesday, settling into the top half of recent ranges while traders waited on landmark data releases due later in the week. Improving prospects for China's economy have also been supportive because of the strength in dairy prices and promises in China of childcare subsidies - an encouraging sign for milk powder demand. Australia employment data on Thursday and another strong reading is expected. That is likely to reinforce bets on the central bank taking rate cuts slowly and lend support to the currency. Markets have priced in about 60 basis points of interest rate cuts in Australia.

The AUD may see near term push higher towards immediate resistance around 0.6382.

CAD

The Canadian dollar edged lower against its U.S. counterpart on Wednesday as the greenback posted broad-based gains, but the move for the loonie was limited as the Federal Reserve marked down its outlook for growth in the world's largest economy. Canada's population in the fourth quarter increased at the slowest pace since the COVID-19 pandemic as a government crackdown on immigration announced last year takes shape. Canadian Feb’s inflation also heated up more than expected. Markets are now focused on Bank of Canada Governor Tiff Macklem’s speech on Thursday about tariff-related uncertainty.

The Loonie looks to be range trading for now, fluctuating between 1.4270 and 1.4380.

XAU

Gold prices soared to an all-time high on Wednesday, following remarks from Powell and as the U.S. Fed held interest rates steady as anticipated, but signaled a possible reduction in borrowing costs. Analyst said Gold is in a bull market now and will continue to move higher on 'elevated' uncertainty and fear of higher inflation. Traders now see a 66% chance of the Fed resuming rate cuts in the June meeting. Gold is expected to be more attractive when interest rates are low. Russia and Ukraine accused each other of violating a new agreement to refrain from attacks on energy targets, with rising geopolitical risk boosting the safe-haven appeal of gold.

The precious metal is eyeing the new all-time-high level at 3080 as the next target.