Market Daily

Macro Update:

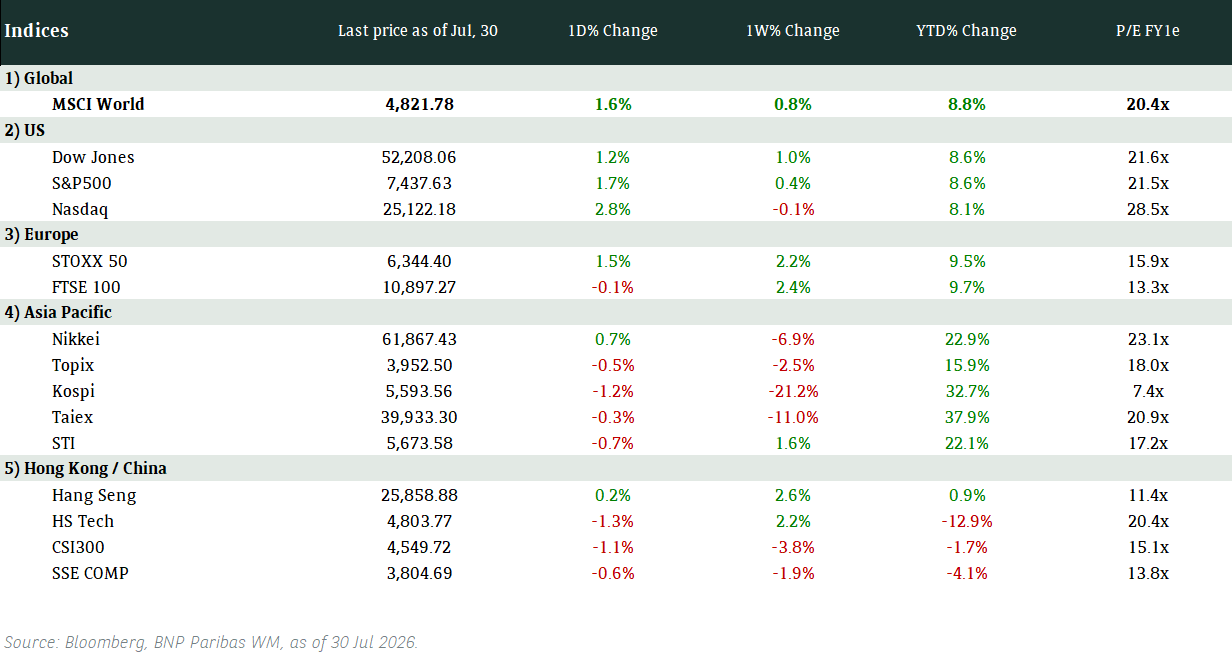

US stock markets fluctuate amid mixed economic data

US initial jobless claims held steady at low level, suggesting a solid labour market. Existing home sales unexpectedly surged 4.2% in February, while Philadelphia Fed manufacturing index fell to its lowest reading since May 2023. A US recession is not our base case scenario, though we have revised down our 2025 US GDP growth forecast from 2.3% to 1.8%.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks traded lower on Thursday as investors digest mixed economic data and some notes of caution about trade from world central bank leaders.

EUROPE EQUITIES

European shares also closed lower on Thursday, after four straight sessions of gains, as investors booked some profits and assessed interest rate decisions by major central banks across the region.

HK EQUITIES

Hong Kong stocks fell on Thursday after investors booked some profits and turned cautious of short-term volatility amid global uncertainties.

We remain positive on HK/China equities in the medium term.

Nike (NKE US)

Nike on Thursday reported FY3Q25 results that beat analyst estimates, with revenue at USD11.27B vs. USD11.03B expected, while EPS was at USD0.54 vs. USD0.29 expected.

The company’s shares still fell in after-market hours, however, as it warned that the current quarter could take the biggest hit from its turnaround efforts, with challenges surrounding inventory clearance and a growing trade war.

In the fiscal fourth quarter, Nike expects revenue to be down in the “low mid-teens” range while gross margins will be lower by four to five percentage points.

In recent years, Nike has been refocusing on sports and rebuilding relationships with retail partners in a bid to maintain its position in the industry. How this turnaround effort will impact the company’s top- and bottom-line will be key to watch going forward.

MARKET CONSENSUS: 23 BUYS, 19 HOLDS, 2 SELLS, AVERAGE TP USD86.6

Microsoft (MSFT US)

Microsoft will launch its first cloud region in Malaysia with three data centers by mid-year, the tech company said on Thursday, nearly a year after it announced a USD2.2B investment in the Southeast Asian country.

The data centers, known as the Malaysia West cloud, will be located in the greater Kuala Lumpur area and will start operations in 2Q25. Microsoft estimated its commitments in Malaysia over the next four years would generate USD10.9B in revenues and create more than 37,000 jobs. This could be supportive to the company's share price.

MARKET CONSENSUS: 66 BUYS, 5 HOLDS, AVERAGE TP USD505.26

FedEx (FDX US)

Shares of FedEx fell in after market hours on Thursday after it lowered its full-year guidance for the third consecutive quarter due to inflation and uncertain demand for shipments.

The company expects adjusted EPS to be in the range of USD18.0 to USD18.6 this fiscal year, while revenue may also be slightly down. The muted guidance may put downward pressure to its share price in the near term.

For the latest quarter, FedEx reported revenue at USD22.16B vs. USD21.90B expected, while adjusted EPS stood at USD4.51 vs. USD4.57 expected.

MARKET CONSENSUS: 22 BUYS, 14 HOLDS, 2 SELLS, AVERAGE TP USD310.77

Eli Lilly (LLY US)

Eli Lilly has launched its blockbuster diabetes and weight-loss drug Mounjaro in India following approval from the country's drug regulator, it said on Thursday.

Mounjaro, chemically known as tirzepatide, is currently sold in the UK and Europe under the same brand name for both diabetes and weight-loss. It is also sold as Zepbound for obesity in the US.

Global demand for Lilly's diabetes and weight-loss drugs has soared in recent years, and the launch in India presents a big opportunity for US-based drug company. India, currently the world's most populous country, is seeing increasing rates of obesity and diabetes.

MARKET CONSENSUS: 28 BUYS, 6 HOLDS, 1 SELL, AVERAGE TP USD1001.48

Volkswagen (VOW3 GR)

The Italian carmaker, Lamborghini, part of the Volkswagen group, said on Thursday that its revenues rose 16% last year to EUR3.09B while its operating profit was up 15.5% to EUR835M, topping the EUR800M threshold for the first time. Nevertheless, the company said potential US tariffs could add further uncertainty to an already contracting luxury market.

Lamborghini, which plans to launch its first fully-electric model in 2029, now has an entirely hybrid three-model line-up, with the Urus SE SUV, the Revuelto sports car and the new Temerario sports car, whose first deliveries are expected between the end of this year and early 2026.

MARKET CONSENSUS: 16 BUYS, 7 HOLDS, 2 SELLS, AVERAGE TP EUR122.1

Earnings Announcements

US Market

-

European Market

-

HK - China Market

NIO, Bank of Communications, Sinopec, Meituan, Sinopharm

Global Indices Changes (%)

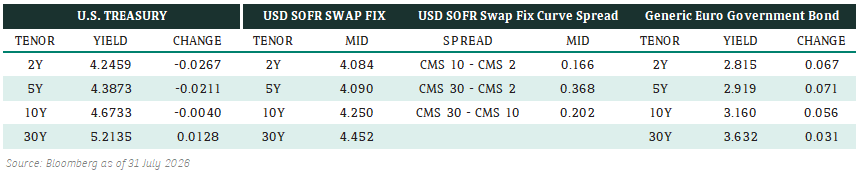

Fixed Income Market Updates

S&P upgraded Krung Thai Bank’s credit rating from BBB- to BBB, with stable outlook. Krung Thai Bank’s profitability has improved, and is comparable with that of large Thai banks, together with prudent management, warrants the upgrade. We think some large Thai banks’ Tier 2 bonds offer favourable valuations.

EUROPEAN BANK COCO (AT1)

European Bank AT1 space closed the day around 5-10cent higher with decent two way flows. Asian and US asset managers were mostly buyers, across various call dates and names. On the other hand, European asset managers were more cautious and were better sellers. We prefer a more conservative approach and will be profit-takers in any rally.

ASIA INVESTMENT GRADE (IG)

In South East Asia IG space, spreads were unchanged to 1bp tighter with better buying from regional asset managers after FOMC. Benchmark names such as Petronas were 1bp tigher while Khazanah Capital had demand from onshore investors. Bangkok Bank's new issue Tier 2 bond continued to see buying interest with private banks as well as asset managers, bringing spreads around 2bps tighter. In Hong Kong, there were more selling in CK Hutchison's bonds.

ASIA HIGH YIELD (HY)

China HY property was largely unchanged. Vanke traded slightly lower on continued selling pressure from hedge funds. New World Development curve traded 0.25-0.5point higher with private banks buying in lower cash price perpetuals. Away from China, India and Indonesia HY space traded around 0.125-0.25point higher as we saw some bottom fishing in Indonesia HY corporate names after the recent volatility in the equity market.

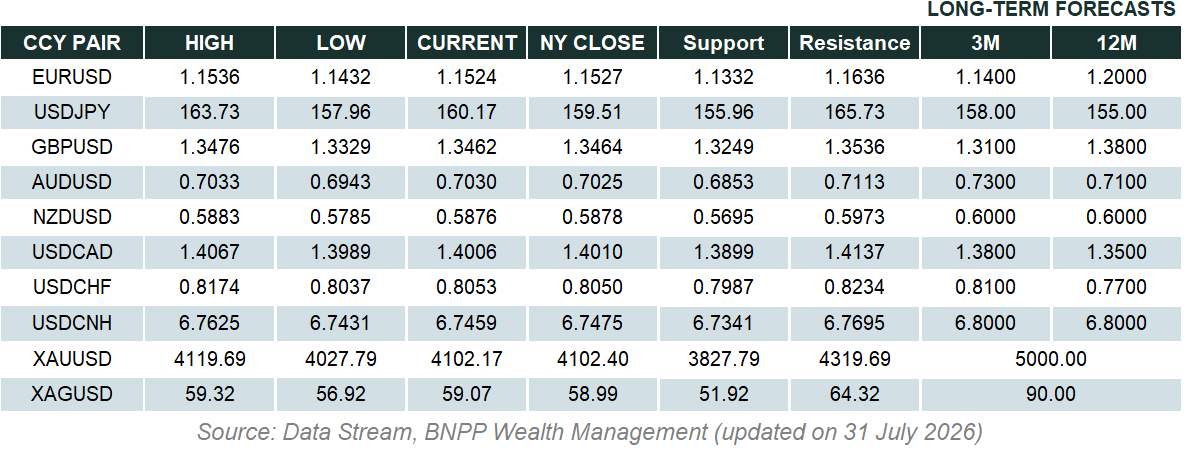

Forex Market Updates

The dollar recovered some of its losses from the week as the Fed remained concerned on the persistent uncertainty surrounding tariffs, stating they are not inclined to cut rates anytime soon.

USD

The US Dollar appreciated broadly on Thursday, a day after the Federal Reserve indicated it was in no rush to cut interest rates further this year due to uncertainties around U.S tariffs. "We're not going to be in any hurry to move," Fed Chair Jerome Powell said. Powell's comments and the Fed statement underscored the challenge faced by policymakers as they navigate President Donald Trump's plans to levy duties on imports from U.S. trading partners and the impact on the economy. Traders are pricing in about 63 basis points of Fed easing this year.

The Dollar Index could see some consolidation between 103.20 and 104.00 moving forward.

CNY

The Chinese Yuan eased against the U.S. dollar on Thursday after China sets its official midpoint rate at the weakest in two months, signalling authorities are keen to prevent quick or sharp gains in the currency against a declining greenback. Prior to the market opening, the People's Bank of China set the midpoint rate, around which the yuan is allowed to trade in a 2% band, at 7.1754 per dollar, its weakest level since U.S. President Trump's inauguration on January 20. Traders said the recent movements in the yuan suggested it is unlikely to strengthen beyond 7.22 per dollar without further market news, particularly regarding developments in trade negotiations between the world's two largest economies.

USDCNH looks to have found a bottom around 7.2200 and should likely be supported at that level.

CAD

The Canadian dollar clawed back its earlier decline against the U.S. dollar on Thursday as oil prices rose and investors weighed comments by Bank of Canada Governor Tiff Macklem for clues that the central bank might pause its interest rate cutting campaign. Macklem said the uncertainty over the effect of U.S. tariffs meant it had to change the way it conducted monetary policy to become less-forward looking than normal, adding that there could be no doubt about the bank's commitment to low inflation. Investors see a roughly 64% chance the BoC moves to the sidelines at its next policy decision on April 16.

The Loonie looks to be range trading for now, fluctuating between 1.4270 and 1.4380.

XAU

Gold prices eased on Thursday after hitting a record high earlier in the session, but retained a bullish outlook driven by potential rate cuts signalled by the Federal Reserve and continuing geopolitical and economic uncertainties. Federal Reserve Chair Jerome Powell said on Wednesday that Trump's initial policies, including extensive import tariffs, may have slowed U.S. economic growth and increased inflation. Trump, meanwhile, criticized the Fed's decision to hold rates, despite projections for two quarter-percentage-point rate cuts by year-end due to weakening economic growth and higher inflation. Traders are pricing in 69 basis points of easing this year from the Fed — at least two rate reductions of 25 bps each, with a cut in July fully priced in.

The precious metal is eyeing the new all-time-high level at 3080 as the next target.