Market Daily

Macro Update:

Trump presses ahead with 25% auto tariffs

US President Trump on Wednesday announced plans to impose 25% auto tariffs, with the measures set to take effect on April 2. Markets tumbled in anticipation of this announcement, as rising fear of retaliation and broader economic fallout fuelled market volatility. Meanwhile, oil prices climbed following US threats of tariffs on nations buying Venezuelan crude, benefitting energy stocks. Copper futures also surged to a record high amid reports that President Trump could impose copper import tariffs within weeks, significantly earlier than the original timeline. Investors now await Friday’s PCE inflation report, a key factor in the Federal Reserve’s next policy decision.

Main Upcoming Macro Indicators

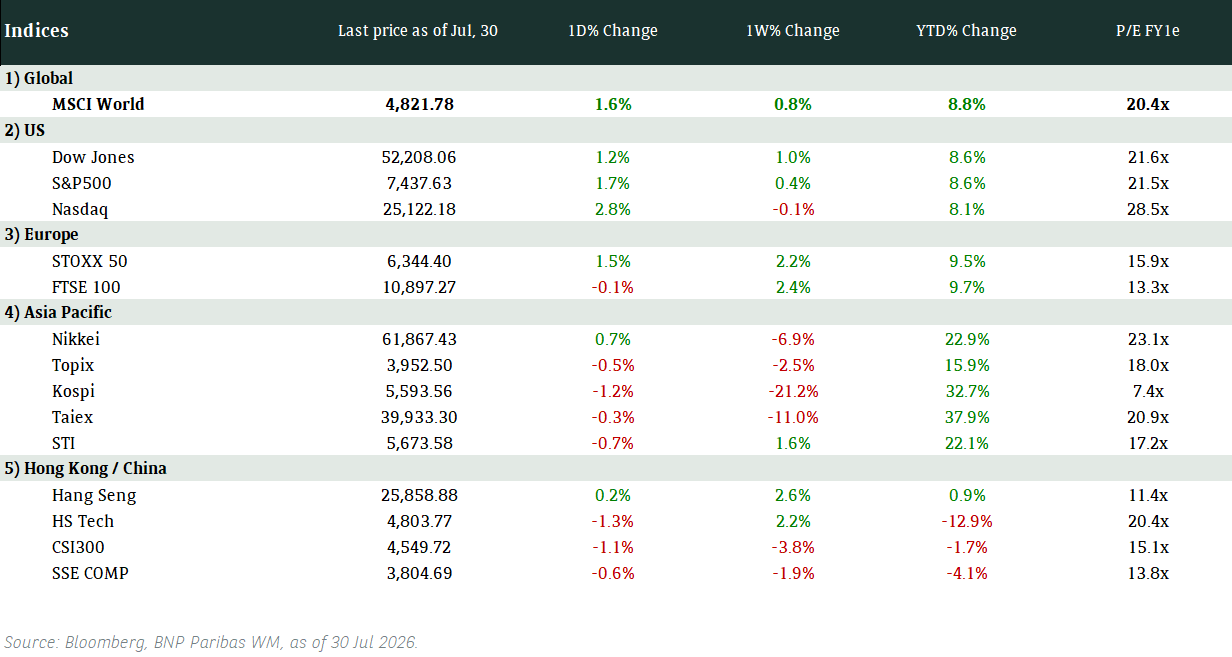

Equity Market Updates

US EQUITIES

US stocks ended sharply lower on Wednesday as an announcement of tariffs on automotive imports subdued sentiment.

Market volatility is likely to remain in the short term.

EUROPE EQUITIES

European shares also traded lower on Wednesday, dragged by technology and healthcare stocks while investors remained concerned about impending US tariffs set to take effect next week.

HK EQUITIES

Hong Kong stocks traded higher on Wednesday, led by auto shares, even as worries over a possible escalation in global trade tensions put a cap to gains.

Nvidia (NVDA US)

Nvidia is reportedly in advanced talks to buy Lepton AI, a two-year-old startup that rents out servers powered by its AI chips, in a deal worth several hundred million USD.

The move is part of Nvidia’s push into the cloud and enterprise software market, in competition with major providers such as Amazon and Google. The company has recently felt increasing pressure to diversify out of hardware because the cloud providers, which are its largest customers, are trying to undercut it by developing and renting out their own chips for a lower price.

Looking ahead, how Nvidia will navigate this competitive landscape is key to its share price trajectory.

MARKET CONSENSUS: 70 BUYS, 6 HOLDS, AVERAGE TP USD172.28

Pop Mart (9992 HK)

Chinese toy maker Pop Mart posted sharply higher annual profit as revenue surged due to strong sales growth.

The Beijing-based company said on Wednesday that its net profit nearly tripled to RMB3.13B last year, while total revenue more than doubled to RMB13.04B.

Sales from Hong Kong, Macau, Taiwan and overseas markets rose nearly fivefold, accounting for 38.9% of its total revenue. Meanwhile, sales across all channels in China rose 52%.

Looking ahead, the company said it will continue to expand its global business footprint, focusing on the North American, Southeast Asian and European markets.

MARKET CONSENSUS: 37 BUYS, 2 HOLDS, AVERAGE TP HKD136.49

CK Hutchison (1 HK)

CK Hutchison’s plan to sell two Panama ports to a BlackRock-led group is reportedly moving ahead as scheduled, in a sign that negotiations have not yet been disrupted by China’s anger over the transaction.

The parties involved are currently working on finalizing due diligence, tax, accounting and other deal terms, and are still aiming to sign an agreement as planned by 2 April. The sale will net USD19B in cash proceeds for the company if completed.

Earlier this month, while the ports to be sold are not in China or Hong Kong, senior Chinese leaders have nevertheless directed officials to start looking into the deal for potential national security and antitrust violations.

MARKET CONSENSUS: 7 BUYS, AVERAGE TP HKD57.4

ENN Energy (2688 HK)

ENN Energy on Wednesday received a take-private offer from its biggest shareholder, ENN Natural Gas, valuing the company at HKD90.5B or HKD80 per share, representing a nearly 35% premium to its last closing price on 18 March.

This deal is part of ENN Natural Gas’ reorganisation plan ahead of its own proposed listing in the Hong Kong Stock Exchange in 2026.

Shares of ENN Energy will resume trading today and will likely see support from the potential take-private transaction.

MARKET CONSENSUS: 22 BUYS, 3 HOLDS, AVERAGE TP HKD69.89

DBS (DBS SP)

DBS Group, Southeast Asia's top bank by assets, is reportedly the frontrunner to buy a controlling stake in Indonesia's Panin Bank.

The Singapore lender was competing with Malaysia's CIMB Group in the second round of the bidding process. The binding bids will be due end-April or early May 2025.

Panin Bank’s net profit climbed 8.2% last year as interest income rose and it provisions for bad debt fell. Its shares have however plunged by about a fifth for the year to date, sliding along with other Indonesian stocks and the rupiah as investor jitters over government policy and the country's fiscal health grow.

If successful, DBS’ acquisition of the Panin Bank stake would make DBS one of the Indonesia’s top ten banks.

MARKET CONSENSUS: 11 BUYS, 8 HOLDS, AVERAGE TP SGD48.63

Earnings Announcements

US Market

-

European Market

CTS Eventim, Jungheinrich, Symrise

HK - China Market

People’s Insurance, Haier Smart Home, Flat Flass, Jiangxi Copper

Global Indices Changes (%)

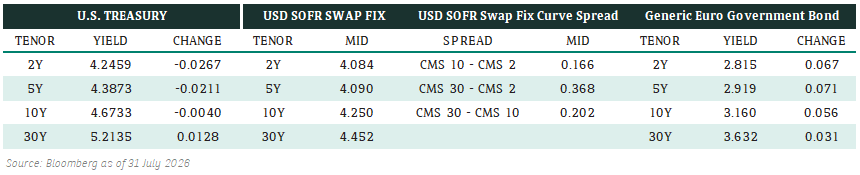

Fixed Income Market Updates

Markets were in the mood for Fried Chicken as Jollibee's new 5y USD paper traded up more than 50bps in the secondary market despite a healthy new issuance market. Within new issues we note that non-financials carry better new issue premium and this tends to support prices.

EUROPEAN BANK COCO (AT1)

Trading activity was relatively muted in the morning with prices stable but activity picked up in the afternoon and prices moved lower with US equities. EUR-denominated AT1 bonds of Deutsche Bank was most impacted with the recent new issue down 0.25-0.625point while the rest of the market was down 0.125-0.25point. Some of the new issues had been priced tight and we do not see much value there.

ASIA INVESTMENT GRADE (IG)

Indonesia sovereign curve was up around 0.125-0.25 point even as flows continued to be skewed towards selling from asset managers and Exchange-Traded-Funds. Asset managers in Asia seem to be still reducing Indon risk. However, we think markets are overreacting as Indonesia's inflation is still low and growth stable. Most of the trading activity had been focused on new issues such as HK's MTR, Korea's LG Energy Solution. We still see a healthy pipeline in the primary market which will provide good entry opportunities for investors.

ASIA HIGH YIELD (HY)

With not much activity going on in China HY space, prices of Vanke and Longfor's bonds were quoted unchanged. There were better buying flows in China Industrials space with West China Cement up around 0.25point as the company mulls USD bond issuance as an option to help refinance half of the USD$600mio due 2026 bonds. Outside of China, India HY space traded 0.125-0.375point lower as asset managers continued to trim positions.

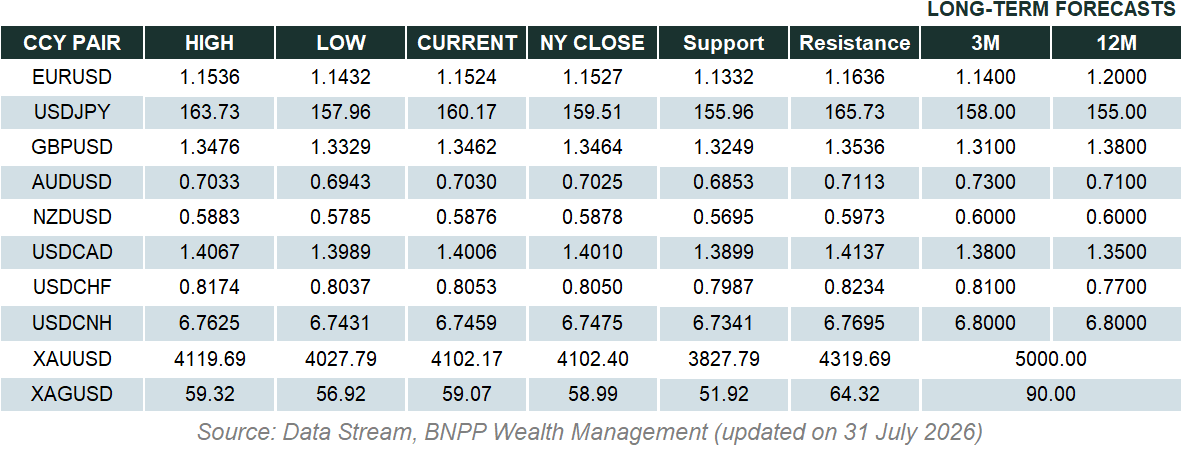

Forex Market Updates

The US Dollar strengthened on Wednesday, supported by tariff concerns, strong durable goods orders, and ongoing inflation fears, with markets eyeing upcoming data and Fed signals.

USD

The US Dollar gained on Wednesday against a basket of other major currencies, as markets assessed the potential impact of tariffs expected to be announced next week by President Donald Trump. Investors are weighing whether these measures will be less severe than anticipated and how they could affect economic growth and inflation. Meanwhile, the dollar found additional support from a stronger than expected rise in US durable goods orders for February, reinforcing signs of economic resilience. With markets focused on upcoming data releases and Fed signals, expectations for interest rates remain a key driver of dollar strength, as markets position for potential shifts in policy outlook amid ongoing inflation concerns.

The Dollar Index could see some near term strength towards 104.95 ahead of the deadline for US reciprocal tariffs.

AUD

The Australian dollar weakened on Wednesday, pressured by a stronger US Dollar, despite softer domestic inflation data. CPI showed signs of slowing, reinforcing expectations of rate cuts from the RBA later in 2024. The government's pre-election budget introduced tax cuts and cost-of-living relief, pushing the fiscal outlook into deficit, though with limited inflationary impact. With inflation cooling, markets are now focused on the upcoming first-quarter inflation report in April for further policy signals. The RBA is expected to keep rates steady in April, with potential easing later in the year.

Ongoing trade war concerns are likely to keep a lid on Aussie gains moving forward, with stiff resistance expected around 0.6400.

GBP

The British Pound weakened on Wednesday as UK inflation came in softer than expected, with CPI rising below forecast. This fuelled expectations of a potential BoE rate cut in May, sending the pound lower to test Monday's two-week low. Additionally, the UK’s downgraded growth forecast and rising public borrowing projections raised concerns over fiscal stability. Chancellor Rachel Reeves announced spending cuts to meet fiscal targets, but analysts warned that tax hikes could be needed if economic conditions worsen. Markets are now focused on upcoming BoE comments and economic data for further direction.

Sterling looks to be range trading and fluctuating between 1.2860 and 1.3000 for now.

XAU

Gold prices eased on Wednesday, with the dollar climbing, but concerns over fresh tariffs from the Trump administration kept prices above $3,000 per ounce. Spot gold was down and closed at $3,019.49 an ounce. Gold continues to benefit from haven demand amid tariff uncertainties and geopolitical risks. Peter Grant, senior metals strategist at Zaner Metals, noted that gold could hit $3,150 if record highs continue. Gold has risen over 15% this year, reflecting its appeal as a hedge. Investors are also watching the upcoming U.S. personal consumption expenditures data for signs of a potential rate cut, which would provide ongoing support for gold.

Bullion is likely to see some near term consolidation between 3000 and 3033 moving forward.