Market Daily

Macro Update:

US stock market suffers from inflation and tariff fears

The higher-than-expected February US core PCE inflation, the Fed’s preferred inflation measure, coupled with Trump’s tariff threat weighed on US stock market last Friday. Gold hit another fresh record high of $3085/oz on safe haven demand. Investors are looking to embrace a volatile market this week as all eyes are on Trump’s tariff “Liberation Day” on 2 April. This Friday’s non-farm payroll data will also help investors to assess the recession risk in the US.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

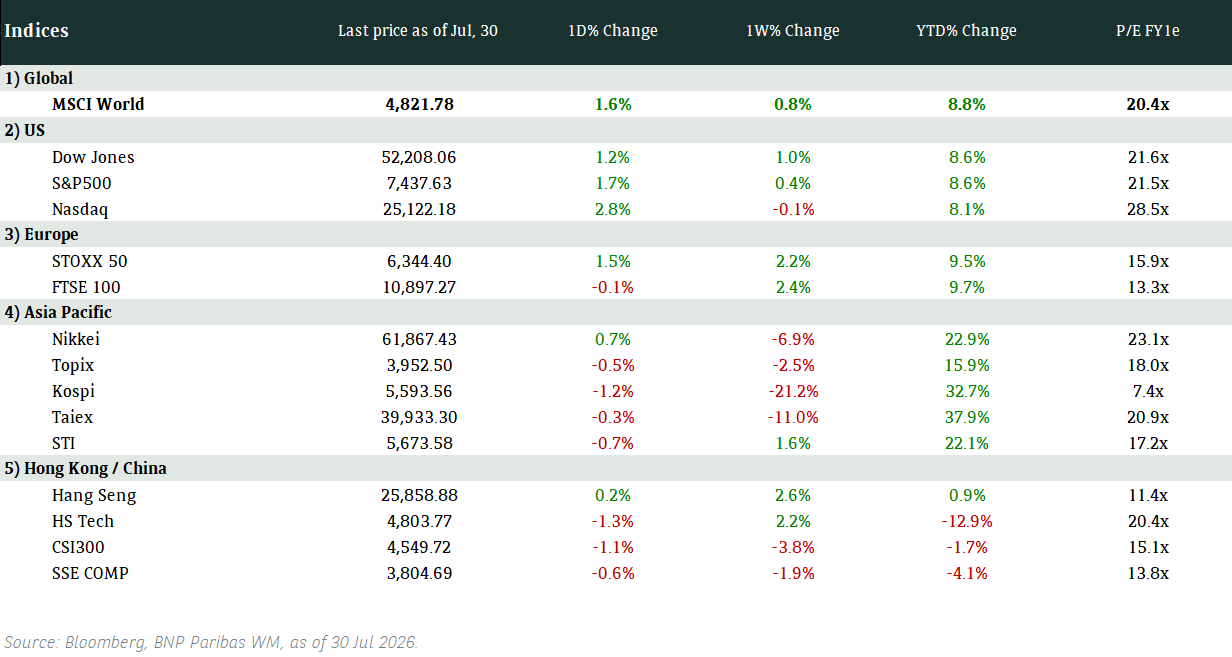

US stocks continued to trade lower on Friday as hot PCE inflation report turned investors' focus on the price impact of tariffs.

EUROPE EQUITIES

European shares also closed lower on Friday as global investors digested this week's tariffs announcements and weighed fresh economic data out from the US.

HK EQUITIES

Hong Kong stocks dropped on Friday as investors sentiment cooled due to concerns that new US tariffs could shake the global economy.

We remain positive on HK/China equities in the medium term.

Stellantis (STLA US)

Stellantis, Europe’s second largest carmaker, said on Saturday that it will buy credits from a pool led by Tesla in 2025 in order to meet European Union’s carbon dioxide reduction requirements, despite Brussels has given carmakers three years to comply.

Carmakers facing tougher EU emissions rules this year agreed to pool their emissions and avoid hefty fines by having firms with lower EV sales to buy carbon credits from segment leaders including Tesla and Polestar.

Although the extension to 2027 has given Stellantis a breather, a tangible solution will likely be needed for the company to comply with the requirements in the medium to long term.

MARKET CONSENSUS: 11 BUYS, 20 HOLDS, 4 SELLS, AVERAGE TP USD14.03

Li Ning (2331 HK)

Chinese sportswear company Li Ning's shares rose after it released its annual results and recommended a higher final dividend for the year.

Net profit in 2024 fell 5.45% to RMB3.01B. The profit was weighed by factors including higher selling and distribution expenses as well as finance expenses. Meanwhile, full-year revenue rose 3.9% to RMB28.68B.

Looking ahead, Li Ning expects consumer spending to grow substantially with strong domestic policy support, potentially supporting the company’s top line in the medium term.

MARKET CONSENSUS: 35 BUYS, 10 HOLDS, 3 SELLS, AVERAGE TP HKD19.99

Longfor Group (960 HK)

Chinese property developer Longfor Group's net profit and revenue declined in 2024 amid a continued sector downturn in China.

Its net profit fell 19% to RMB10.40B, while its revenue dropped to RMB127.5B from RMB180.7B in 2023.

Revenue from Longfor's core property development business fell 35% to RMB100.8B. Revenue from its investment property operation and property service segments rose 7.4% to RMB26.7B.

Longfor said it will focus on reducing inventory in its property development business while replenishing land and improving its land bank structure. How this translates into its top- and bottom-line is key for the share price going forward.

MARKET CONSENSUS: 26 BUYS, 5 HOLDS, AVERAGE TP HKD11.96

EQT (EQT SS)

EQT has raised EUR21.5B for its latest infrastructure fund, EQT Infrastructure VI, which had targeted EUR20B. It includes EUR21.3B in fee-generating assets under management.

The fund will invest in digital infrastructure as well as assets generating, storing, and distributing energy. It will also focus on investments tied to the decarbonization and electrification of industrial processes and social infrastructure, among other areas, the firm said.

Looking ahead, EQT’s fundraising momentum and fund performance will be of investors’ focus.

MARKET CONSENSUS: 9 BUYS, 5 HOLDS, 2 SELLS, AVERAGE TP SEK382.94

MUFG (8306 JP)

Mitsubishi UFJ Financial Group (MUFG) expects a revenue boost in its China corporate and investment banking business as more local firms are planning to expand outside their home country.

Outbound investment from China is growing as trade-policy tension and weak domestic demand prompted more local firms to examine opportunities abroad.

Moreover, inbound flows into China’s onshore securities rose to a record pace in February with improving sentiment on sectors such as tech and consumption.

MUFG, which currently has 14 branches in China, will focus on servicing Chinese corporate clients in areas including EVs, smartphone parts, and solar energy going forward.

MARKET CONSENSUS: 12 BUYS, 5 HOLDS, 1 SELL, AVERAGE TP JPY2177.31

Earnings Announcements

US Market

-

European Market

-

HK - China Market

-

Global Indices Changes (%)

Fixed Income Market Updates

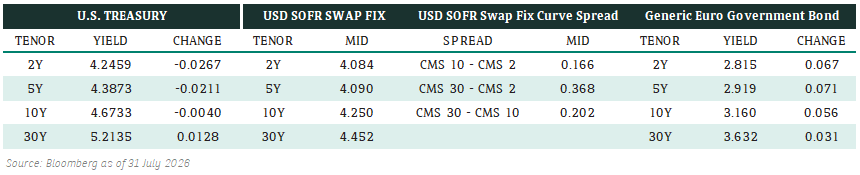

US Treasury yields fell sharply last Friday on the back of inflation data and certain tariffs are set to take effect on April 2nd. This week is set to be choppy and reversal of yields is a good opportunity for low beta, high quality credit. Unsurprinsgly, high beta has been softer, but more in terms of trimming risk, especially high yield, and we expect this to continue to be the case.

EUROPEAN BANK COCO (AT1)

Market for European Bank AT1 moved lower in general in response to tariffs but there was no panic selling. Investors were trimming risk positions. Prices were stable on Friday and slightly wider on spread. The recently issued EUR-denominated AT1 bond by Deutsche Bank was the first to be hit with the bonds down more initially but recovered to trade more in line with market. USD-denominated AT1 bonds traded lower as well..

ASIA INVESTMENT GRADE (IG)

We saw material risk-off in New York to finish the week. IG widened 3-7 bps (basis points wider) and we expect a soft tone to start the week in Asia as well. As mentioned, Bloomberg reported that China had told State-Owned Enterprises to hold off on any new collaboration with businesses linked to Li Ka-Shing and his family, which led CK Hutchison and Hutchison Ports to trade 10-20bps wider and FWD traded 1.5-2points lower.

ASIA HIGH YIELD (HY)

In Asia HY space, Macau gaming and India HY caught a bid but we expect spreads to be wider this week given the weak macro tone. Away from China, Mongolian Mining's 8.44% 5-year non-call 3-year newly issued bond traded 1point lower at market opened and went even lower before bottom fishers came in.

Forex Market Updates

The U.S. dollar declined on Friday amid growing stagflation concerns, ahead of an anticipated announcement from President Donald Trump on reciprocal tariffs on April 2nd.

USD

The US Dollar weakened on Friday on growth concerns ahead of a planned announcement next week by U.S. President Donald Trump on reciprocal tariffs. Traders have had bouts of optimism that the trade levies will not be as severe as feared, but concerns remain that new tariffs could slow growth and reignite inflation. Higher-than-expected core inflation data announced on Friday also amplified the fears of stagflation. The lack of clarity over exactly which tariffs will be implemented has added to investor caution. Analysts didn’t expect a sustained rally in the U.S. dollar despite the new tariffs, given ongoing concerns about a potential economic slowdown. Moreover, the logistical complexity of implementing new tariffs could delay enforcement, leaving room for further negotiations.

The Dollar Index could see near-term push higher toward immediate resistance around 104.67 as the deadline for reciprocal tariffs approaches.

CAD

The CAD edged lower against its U.S. counterpart on Friday but held on to a weekly gain as investors weighed disappointing U.S. economic data and awaited the next round of Washington's trade tariffs. Markets increasingly doubt the U.S. economy can avoid fallout from a widening global trade war, supporting the Canadian dollar earlier in the week. However, analysts expect limited movement in the near term until the scope of the reciprocal tariffs is known. Meanwhile, Trump announced on Wednesday a 25% tariff on imported vehicles, which is Canada’s second-largest export after oil. Trump and Canadian Prime Minister Mark Carney had a conversation on Friday that both men described as productive, although Carney said Ottawa would be imposing retaliatory tariffs next week as promised.

The USDCAD looks to be range trading for now, fluctuating between 1.4235 and 1.4400.

CNH

The Chinese Yuan hovered near a three-week low against the dollar on Friday and looked set for a second weekly loss, as concerns over worsening trade relations between the world's two largest economies continued to dampen sentiment. Meanwhile, prospects of a widening yield gap between the U.S. and China also dragged the yuan lower after senior officials at the central bank repeatedly talked about further monetary stimulus. Analysts said although the PBOC has kept the yuan relatively stable in recent months despite the additional 20 percent tariffs on Chinese exports, this stability may be short-lived. Further escalation of tariffs is expected to prompt a response in the currency. Markets now focus on upcoming economic data including China's March manufacturing activity data due on Monday for more clues on the health of the broad economy.

Renminbi may consolidate around the current level and fluctuate between 7.2500 and 7.2800 in the short term.

XAU

Gold prices surged to a record high at $3,086.70 on Friday, as investors flocked to the safe-haven asset amid fears of a global trade war triggered by U.S. President Donald Trump's latest tariffs. Bullion is up 1.7% this week and is on track for a fourth straight weekly gain. Markets are now bracing for Trump's plans for reciprocal tariffs, which he intends to lay out on April 2. Trump's policies are perceived as inflationary, posing a risk to economic growth and escalating trade tensions, analysts say. Therefore, gold’s fundamentals remain strong, as it is traditionally seen as a hedge against economic and political instability, tends to thrive in a low-interest rate environment.

The precious metal is eyeing a new all-time-high level around 3,100 as the next target.