Market Daily

Macro Update:

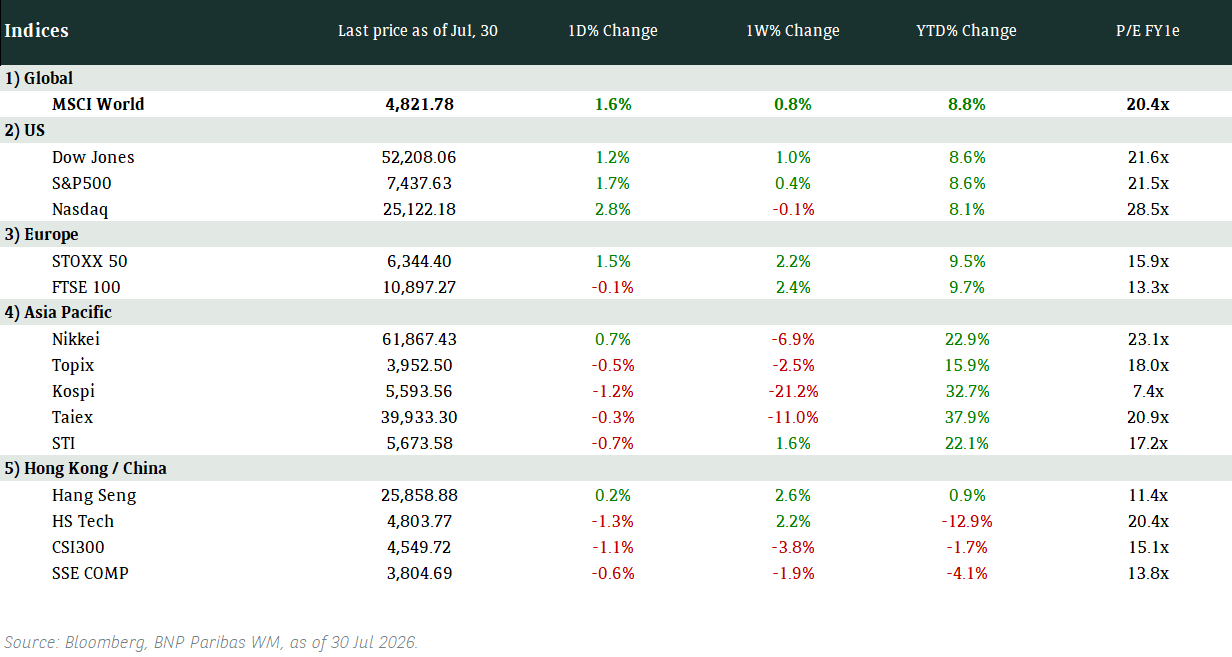

US stocks trim losses after some easing of trade tensions

Market selloff extended on Tuesday, amid global trade policy uncertainty which is reigniting fears of a global economic slowdown. US equities recovered slightly from initial losses, but investors continue to be cautious of the current trade situation. This was after US President Trump reversed his earlier threat to double tariffs on steel and aluminum from Canada to 50%, following Ontario Premier Doug Ford suspension of a retaliation move of 25% surcharge on power exports, as a meeting between Ontario Premier Ford and US Commerce Secretary Howard Lutnick on Thursday was announced. We think volatility is likely to remain high, particularly in the US due to policy uncertainty, hence we switch to view from positive to neutral on US equities.

Main Upcoming Macro Indicators

Equity Market Updates

US EQUITIES

US stocks closed lower on Tuesday, adding to its biggest selloff in months, as concerns surrounding trade policy continue to subdue investor sentiment.

EUROPE EQUITIES

European equities moved lower on Tuesday as developments in the US also damped the mood in the region.

HK EQUITIES

Hong Kong stocks ended flat on Tuesday, defying a regional gloom after the US market’s sharp declines, in a sign of growing confidence in China’s economy following the rise of Deepseek.

We are positive on Hong Kong / China equities in the medium term.

CrowdStrike (CRWD US)

Shares of CrowdStrike traded higher on Tuesday after announcing an expansion to its Accelerate partner program, aimed at enhancing collaboration and profitability in the cybersecurity industry.

The program, which unites a wide range of partners to deliver cybersecurity solutions through the CrowdStrike Falcon platform, now offers new opportunities to maximize revenue, including discounts, rebates, training credits, and more predictable pricing models.

This improvement is likely to provide CrowdStrike a sizeable edge over its competitors and support its share price going forward.

MARKET CONSENSUS: 40 BUYS, 14 HOLDS, 1 SELL, AVERAGE TP USD409.2

Verizon (VZ US)

Shares of Verizon fell by the most since 2023 on Tuesday after its chief revenue officer acknowledged "a challenging quarter from a competitive intensity standpoint" at a Deutsche Bank investor conference.

The company now expects postpaid phone gross additions to be unchanged to slightly down in 1Q25 on the back of recent pricing actions in the industry. Verizon nevertheless remains confident in its full year forecast, stating that it will generate more consumer postpaid phone net additions later in the year.

The market will closely watch Verizon’s top-line figures in the next few quarters.

MARKET CONSENSUS: 12 BUYS, 17 HOLDS, 1 SELL, AVERAGE TP USD46.45

Domino Pizza (DPZ US)

Domino's Pizza reported a rise in underlying annual core profit of about 4% on Tuesday, citing increasing orders boosted by discount offerings.

The pizza chain reported an underlying EBITDA of GBP143.4M for the 52 weeks ended 29 December 2024, compared to GBP138.1M in the year prior.

The company has been actively expanding both its store network and digital platform as part of its target to reach GBP2B in sales from more than 1,600 stores by 2028.

Looking ahead, Dominos said it expects its underlying EBITDA for 2025 to be in line with current market expectations.

MARKET CONSENSUS: 20 BUYS, 12 HOLDS, 2 SELLS, AVERAGE TP USD489.13

Volkswagen (VOW3 GR)

Volkswagen, Europe's top carmaker, expects an operating margin of 5.5-6.5% in 2025 from 5.9% in 2024, joining rivals in giving a muted outlook for the year ahead as the sector battles weak demand, high costs and simmering trade tensions.

Volkswagen's shares have fallen by over 40% in the past four years, also hit by a slower-than-expected ramp-up of EV production, major pricing pressure in top market China and Asian rivals entering the European market.

The outlook for 2025 does not factor in the possible impact of trade tariffs threatened by US on imports from Mexico or Europe, the company said.

How the challenges in the global economy and the industry will alter the top and bottom line of the company will be key to watch going forward.

MARKET CONSENSUS: 15 BUYS, 8 HOLDS, 3 SELLS, AVERAGE TP EUR115.87

Partners Group (PGHN SW)

Partners Group on Tuesday posted better-than-expected full year 2024 results. The Swiss investment management company's 2024 revenue stood at CHF2.14B, up 10% from CHF1.95B a year earlier while also beating expectations at CHF2.09B. The company's EBITDA increased 10% to CHF1.36B from CHF1.23B last year, also beating the CHF1.32B expected.

The company said that its guidance is confirmed and the performance fee outlook is positive. It also will propose a dividend of CHF42 per share, 8% higher compared to last year. This is likely to provide some support to its share price in the short term.

MARKET CONSENSUS: 11 BUYS, 5 HOLDS, 3 SELLS, AVERAGE TP CHF1351.87

Earnings Announcements

US Market

-

European Market

-

HK - China Market

Ping An Healthcare

Global Indices Changes (%)

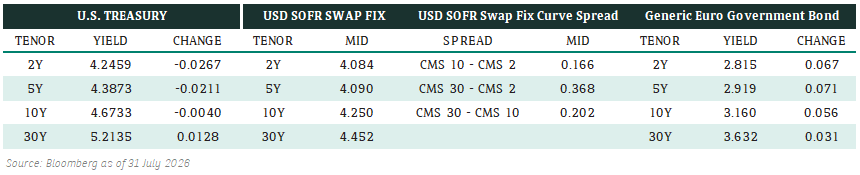

Fixed Income Market Updates

Bond market has been relatively stable as sentiment goes risk-off . Market is gradually pricing in an US economic slowdown scenario. We thus expect to see more fund flow into the fixed income space as investors are turning more defensive due to rising geopolitical tension and recession worries.

EUROPEAN BANK COCO (AT1)

European bank coco was weaker. Bond prices were generally 0.125-0..375 points lower. USD coco held up relatively better than EUR coco, but we also started to see some selling. We remain cautious on coco’s expensive valuation and would suggest to take profit after recent rally.

ASIA INVESTMENT GRADE (IG)

It was a slightly weaker session for Asia IG. Credit spread was 1-5 basis points wider and we saw particularly weaker sentiment in China telecommunication. Names like Alibaba and Xiaomi were 5-7 basis points wider but we saw quickly some speculative investors bottom fishing after sell-off. Overall, we feel investors demand on Asia IG bonds is still strong and expect the strong momentum to continue on the back of rising geopolitical tension.

ASIA HIGH YIELD (HY)

China HY held up quite well relative to the rest of Asia HY. China HY property were largely stable with bond prices unchanged to 0.25 points with limited selling. However, we noticed some selling from hedge fund investors on China HY industrial such as Fosun and Macau gaming. Outside of China, India and Indonesia HY were weaker and top underperformer was the Adani complex which was 0.5-1 points lower. We remain cautious on HY bonds and expect to see some more weakness.

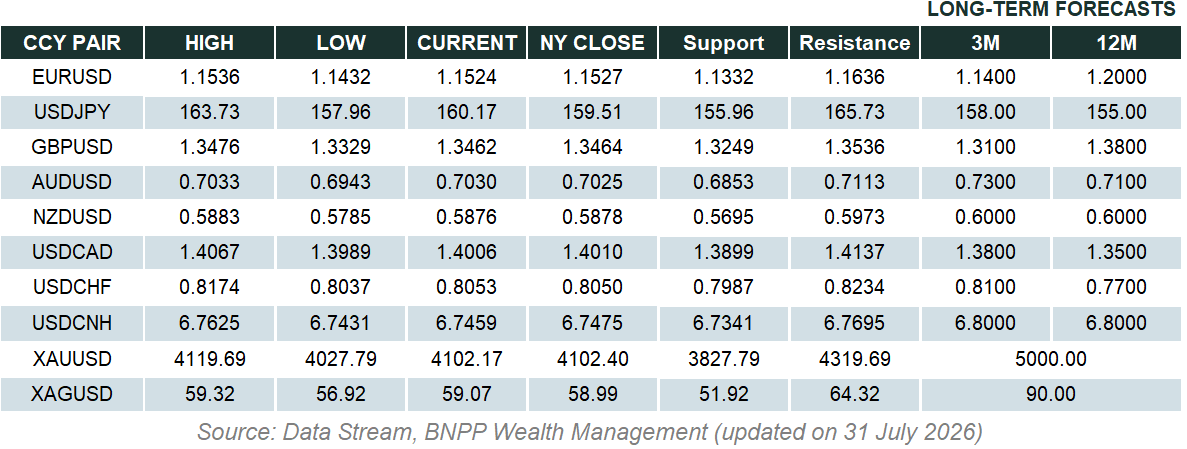

Forex Market Updates

The US Dollar fell to fresh 2025 lows on Tuesday as US recession fears continued to dominate market sentiment.

USD

The US Dollar fell on Tuesday to five-month lows against a basket of other major currencies amid growing worries about the potential impact of US President Trump’s trade war on the global economy. In tandem with the selloff in equity markets around the world, the Dollar Index slipped to an intraday low of 103.23, a level not seen since last October, due to fears that the world’s largest economy could slip into a recession. Elsewhere, Trump fired another salvo in his trade war against Canada, saying that he would add an additional 25% tariff on all Canadian steel and aluminum coming into the US, but later added that he may “look at backing down on the 50% duties on Canada” after speaking to Ontario Premier Doug Ford.

The Dollar Index looks poised to see more near term weakness, with USD bears likely to target 102.50.

AUD

The Australian Dollar edged higher yesterday to halt a run of three straight days of losses, but gains were capped as risk-off sentiment continued to dominate markets. Analysts say that the Aussie has been caught between opposing forces of late – fears of a sharp US economic slowdown have hit the high-beta currency, but a broadly weaker USD on the back of lower yields has offered some breathing room that has kept the Aussie well-supported above the multi-year lows seen in January. Elsewhere, thanks to waning inflation and last month’s RBA rate cut, the latest survey of consumer confidence Down Under saw a significant rise from 92.2 to 95.9, a three-year high.

Ongoing trade war concerns are likely to keep a lid on Aussie gains moving forward, with stiff resistance expected around 0.6370.

GBP

The British Pound regained its footing yesterday after the previous day’s losses, notching a fresh 2025 high against the USD as fears of a US recession drove traders away from the greenback, although Sterling weakened against the resurgent Euro for the seventh consecutive session. Analysts say that recent GBP strength has been supporting by a steepening UK yield curve that shifts UK-US relative rate differentials in Sterling’s favour. On the data front, as a survey favoured by the BoE showed that wages for new hires had risen at their slowest pace in four years, in line with recently deteriorating UK labour data.

Sterling’s 7% rally since the start of the year could run into strong resistance around the key 1.3000 handle.

XAU

Gold prices rose roughly 0.9% on Tuesday amid a broadly weaker USD and worries of a global economic slowdown due to tariff wars as markets looked ahead to key US inflation data that could shed further light on the trajectory of US interest rates. Some analysts say that from a technical perspective, bullion’s sharp rise is starting to show tentative signs of exhaustion as it approaches the psychological 3000 level. From a macro standpoint, any positive developments in this week’s Russia-Ukraine negotiations could see a reduction in risk premiums, although the precious metal is likely to remain supported due to safe haven demand given ongoing market uncertainties.

Bullion is likely to be well supported above 2835 in the near term.