Equity Market Updates

S&P 500 futures plunged more than 3% after President Trump outlined his tariff plans that spark fears of a full-blown global trade war and raise the risk of a US recession. Trump will apply a minimum 10% tariff on all US imports. China and Europe will face a 34% and a 20% rate respectively. Some countries such as Vietnam will see a 46% duty. Some analysts estimated that the weighted-average tariff rate will be at 29%, almost doubled market expectations of around 15%. Market will remain highly volatile and is looking for clues on any countries’ retaliation plans or any signs of concessions.

Equity Market Updates

US indices closed Wednesday higher but dipped into red during afterhours trading after President Trump unveiled reciprocal tariffs that were more aggressive than expected

European equities fell as investors awaited US president Trump’s announcement of sweeping tariffs. Market assessed the risks related to the European Union potentially responding to the new tariffs with countermeasures, which could have an additional impact on economic conditions

Hong Kong stocks traded near the flatline to close the day down 2bps ahead of US tariff announcement.

The board is mixed, with weakness led by Materials, Info Tech, Healthcare, and Energy, while Consumer Staples outperformed significantly.

Xiaomi (1810 HK)

Xiaomi shares slid another 4.2% to close at the lowest level since mid-Feb after Chinese policy launched a probe into an accident involving on of its EVs. Shares are down for a 5th straight session, with shares now more than 20% below a record high last month.

The extended weakness came after Xiaomi confirmed Tuesday that one of its SU7 EVs was involved in an accident on an expressway in China. Xiaomi’s CEO Lei Jun promised to keep working with the police in the investigation.

Accidents like such is expected to put pressure on car makers, especially as the market expects autonomous driving to be the next big catalyst.

MARKET CONSENSUS: 51 BUYS, 3 HOLDS, 1 SELL, AVERAGE TP HKD62.39

City Developments (CIT SP)

Singapore Exchange Regulation has questioned City Developments about corporate governance issues and disclosures related to a public dispute within the family owner of the developer. The inquiry comes after a feud broke out between the patriarch of the country’s richest family and his elder son, leading to an abrupt cancellation of a press briefing and a 3 days’ trading halt.

The company disclosed that the board will continue to work together to focus on CDL’s strength in accordance with good corporate governance and maximising shareholder value. While the announcement is a step in the right direction, in our view, it remains to be seen whether the current board can continue to work together seamlessly.

MARKET CONSENSUS: 6 BUYS, 5 HOLDS, 3 SELLS, AVERAGE TP SGD5.93

Uber (UBER US)

Uber and WeRide jointly partnering with Dubai's Road and Transport Authority (RTA) to bring autonomous vehicle (AV) services to the United Arab Emirates city, Uber announced.

"The partnership paves the way for Uber to make AVs an accessible and reliable part of everyday life in Dubai, beginning with WeRide as the first technology partner," the company remarked.

As part of the deal, Uber and RTA are collaborating on pilot programs leveraging Uber's technology to match riders with AVs. The agreement also includes looking into data insights, safety protocols, and regulatory frameworks.

MARKET CONSENSUS: 49 BUYS, 11 HOLDS, AVERAGE TP USD89.454

Tesla (TSLA US)

Tesla’s vehicle sales fell 13% last quarter to 336,681, its worst showing since 2Q22. The figures speak to the extent of the disruptions to Tesla’s business early this year. the company retooled factories around the globe to produce the redesigned Model Y, leading to lost output that’s common when carmakers transition from one vehicle generation to another.

The extraordinary factor was Musk’s involvement in global politics that sparked protests across the US and Europe. Shares tumbled 6.4% before turning positive on a report that Musk might likely be stepping back from his government advisory role in the coming weeks.

Recent accident with Xiaomi’s EV has also put a spotlight on autonomous driving.

MARKET CONSENSUS: 39 BUYS, 7 HOLDS, 1 SELL, AVERAGE TP USD384.08

Amazon (AMZN US)

Amazon has reportedly presented a bid to purchase TikTok as the company is nearing the deadline to be banned from US unless it changes ownership.

Previously, it was reported that companies such as Microsoft, Oracle, Reddit and Andreessen Horowitz Capital Management were interested in acquiring TikTok. Later, it was alleged that Trump will consider the final proposal for that on Wednesday.

MARKET CONSENSUS: 78 BUYS, 4 HOLDS, AVERAGE TP USD267.51

Earnings Announcements

-

Global Indices Changes (%)

Fixed Income Market Updates

Moody’s downgraded West China Cement’s senior unsecured rating to Caa2 from Caa1 with outlook remaining on negative. West China Cement’s liquidity is still weak and the lack of concrete progress in refinancing its 2026 USD bond is worrying. We think refinancing conditions remain challenging for most Chinese High Yield companies.

EUROPEAN BANK COCO (AT1)

Trading activity was lighter in European Bank AT1 space as investors were on the sides awaiting Trump's tariffs announcement. There were small flows from asset managers rebalancing portfolios and net buying from European hedge funds. We think valuations look rich for some AT1 bonds and would refrain from adding positions until we see meaningful correction in this space.

ASIA INVESTMENT GRADE (IG)

In South-East Asia IG space, selling from asset managers picked up after lunch as spreads went wider and investors adopted a more cautious tone. Overall, spreads widened 2-10bps. Long duration bonds of ThaiOil were back to year-to-date wides as both asset managers and retail were selling. India IG space started the date trading tighter but widened as well as the day progressed. IG names with solid credit fundamentals remain our preferred picks.

ASIA HIGH YIELD (HY)

Sentiment was weak in Asia HY space. In India, Biocon Biologics was down around 1point after headline news of CEO leaving to join a subsidiary and indefinitely postponing the IPO. Other Indian HY names like Vedanta and non-bank financials names were down on average 0.125-0.25point.

Forex Market Updates

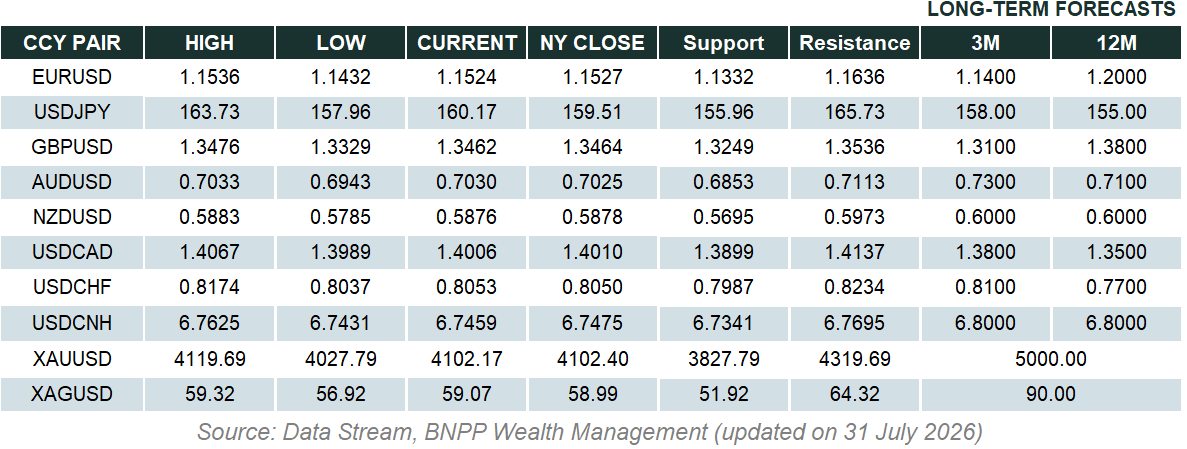

The US Dollar weakened as Trump announced new tariffs, increasing trade tensions. IMF data showed a decline in the dollar’s global reserves share, with stagflation risks looming.

USD

The US Dollar weakened against a basket of other major currencies on Wednesday as President Trump announced new tariffs, escalating trade tensions. Trump confirmed 25% tariffs on foreign-made autos and introduced a 10% baseline tariff on all US imports. This sparked volatility in the markets, raising concerns about inflation and potential economic slowdown. Meanwhile, International Monetary Fund (IMF) data showed a continued decline in the dollar’s share of global FX reserves, although its dominance remains intact. Investors are now closely monitoring the Fed’s response to the growing risks of stagflation and how it could impact the dollar’s future performance.

The Dollar Index could see further near term weakness, with USD bears likely to be well supported above 103.20 for the time being.

GBP

The British Pound strengthened on Wednesday as markets reacted to US President Donald Trump’s tariff announcement, which could have broader trade implications. Sterling gained against the dollar, reflecting cautious optimism as traders assessed potential risks. The UK has yet to announce a response, hoping for exemptions or a broader agreement with the US. Meanwhile, slowing wage growth has reinforced expectations of a potential BoE rate cut later this year. With ongoing uncertainty over tariffs and economic policy, investors remain focused on how these factors will shape the pound’s outlook.

Sterling could see some near term consolidation between 1.2860 and 1.3000 for now.

AUD

The Australian dollar strengthened on Wednesday as market sentiment improved despite concerns over US tariffs. While the Aussie’s role as a risk proxy has been evolving due to structural changes—such as increased offshore investments and reduced reliance on commodities—it found support amid shifting global dynamics. Analysts noted that AUD/USD trading volumes remained subdued, reflecting this changing relationship with risk. Meanwhile, Australian Prime Minister Anthony Albanese and opposition leader Peter Dutton reaffirmed their commitment to protecting national interests, particularly in response to potential US tariffs on beef and technology, as policymakers navigate ongoing trade uncertainties.

Ongoing trade war concerns are likely to keep a lid on potential Aussie strength moving forward, with stiff resistance expected around 0.6400.

XAU

Gold prices extended gains on Wednesday, reaching an all-time high, driven by safe haven inflows after US President Donald Trump’s announcement of reciprocal tariffs, escalating the trade war. Spot gold rose and closed at 3133.57. The tariffs, which include a 34% levy on China and 20% on the European Union, caused the US Dollar to weaken, making gold more attractive to holders of other currencies. With a bullish outlook, gold’s near-term target is seen at $3,200, as markets brace for heightened volatility amid ongoing political and financial uncertainty.

Given the array of supportive factors, gold bulls are likely to target the 3,200 level going forward.

Please read carefully the disclaimer here:

Asia Disclaimer:

https://wealthmanagement.bnpparibas/asia/en/disclaimer1.html

Europe Disclaimer:

https://wealthmanagement.bnpparibas/ch/en/disclaimer.html