Third (Plenum) Time’s The Charm?

Time’s The Charm?")

Key takeaways

China’s four-day Third Plenum meeting, which typically takes place twice a decade concluded on Thursday, 18th July 2024, and it signaled high degree of policy continuity. Historically, the Third Plenum focusses primarily on medium to long-term goals rather than addressing short-term issues. Unsurprisingly, the meeting this time round was a reform-focused meeting of China’s Communist Party Central Committee, and yielded a communique long on commitments albeit short on specifics.

The key themes were deepening reform and pursuing Chinese-style modernisation, as China aims to establish a high-level socialist market economic system by 2035. Specific goals include giving a bigger role to market mechanisms, creating a fairer and more dynamic market environment, opening up to the outside world, and expanding international cooperation via reform of foreign trade and investment. The government continues to present a solid long-term vision where unsurprisingly, innovation, green development, and consumption are keys to modernisation and growth drivers.

These policies will be rolled out successively, although President Xi Jinping and his team have promised to complete some reforms by 2029 when the People’s Republic of China marks the 80th anniversary of its founding. Crucially, policy specifics on how these goals can be achieved will be more important to convince markets.

CPC pledged to hit near term economic targets

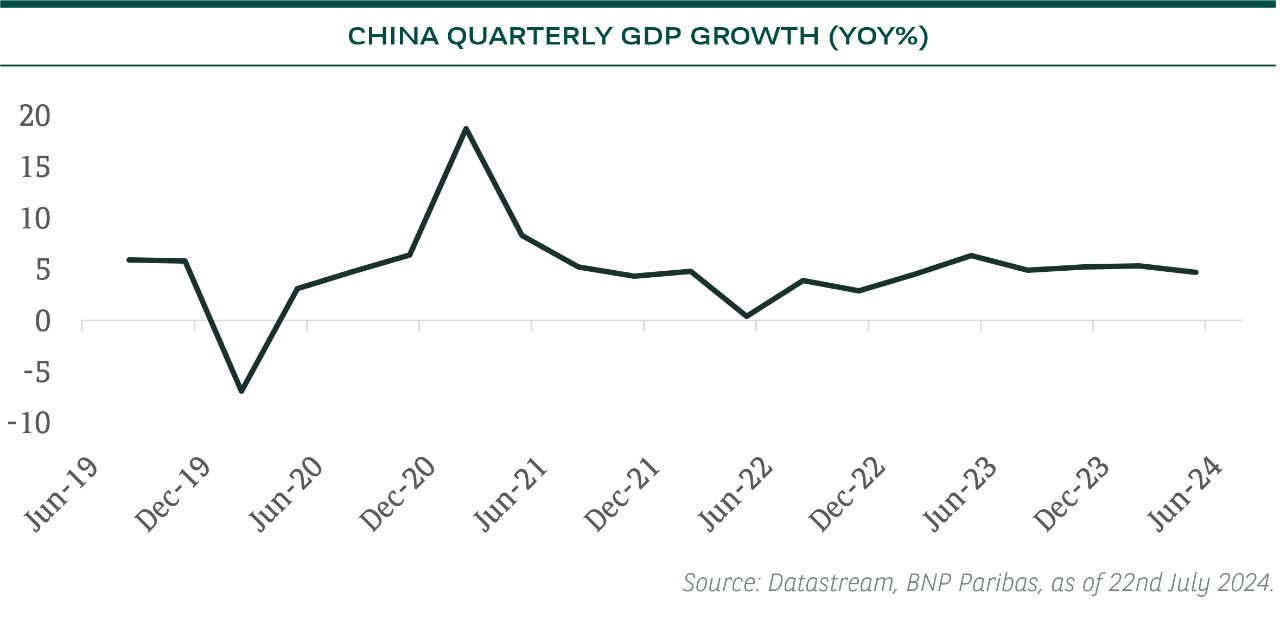

The meeting commenced on 15th July 2024, coincidentally (or perhaps non-coincidentally) after the release of a worse than expected GDP growth. Real GDP growth decelerated to 4.7% YoY in Q2, missing market expectations by 0.4ppt. The data seriously put the official 5% GDP growth target for full year 2024 in doubt. The industrial sector growth remained strong, partly due to stronger exports, but the growth drag came mainly from the services sector, which slowed to 4.2% in Q2 on the back of softer domestic demand and an underperforming property sector.

The GDP data sparked demand for more stimulus measures specifically for the property sector and consumption. Perhaps due to the increasingly troubled domestic and external landscape, the party did discuss achieving this year's growth target of 5%, keep growth on track, and implement macro policies that support domestic demand during the meeting. This raises hope for possibly more support measures near-term. Nonetheless, the level of details so far do not yet point to more than a gradualist approach to economic stimulus. Given recent weakness in economic data the market will wait for more details on these important topics.

PBoC sang the same tune

Following the conclusion of the Third Plenum, the People's Bank of China (PBoC) announced a 10bp cut in the 7-day reverse repo rate (to 1.7% from 1.8%) on Monday morning, 22nd July 2024. 1-year and 5-year loan prime rates were also slashed by 10bp (1-year LPR to 3.35% from 3.45%; 5-year LPR to 3.85% from 3.95%). The central bank acknowledged that the economy faces insufficient demand and weak market expectations, and hence is committed to adopting countercyclical tools to boost domestic confidence.

Although unexpected, the PBoC’s decision to cut policy rate is in line with the policymakers’ strong determination to fulfil the 5% growth target conveyed by the Third Plenum. We think the PBoC is likely to stick to small and gradual pace of interest rate cuts. Growing conviction that the Fed is going to embark on an easing cycle in September also provides more maneuverability for the PBoC to cut rates earlier.

Looking ahead

Policymakers may need to rethink their near-term policy mix to achieve the 5% annual growth target. In particular, a budget revision is maybe necessary to keep up the pace of spending against a continued decline in local government revenues. The latest end July Politburo meeting offered little new stimulus, but policy guidance for 2H24 maintained pro-growth. The Politburo emphasized on boosting consumption, albeit the pace and timing of measures remain unclear. The target of 5% GDP growth was again reiterated, hence falling below that pace in Q3 could result in new stimulus in Q4 (such as another RMB1trn China Government Bond quota).