Strategic-A is about strategic asset allocation and strategic asset allocation is the first critical step when building your portfolio allocation. The past 5 years have been a roller coaster ride in financial markets and higher uncertainty is likely to be a permanent feature of the market for years to come. To cope with such an environment, it is not sufficient to buy and hold stocks or bonds in an opportunistic manner to weather market shocks. No, first, before thinking of investing in single products, investors should step back, think long term (5-10 years) and define and build, at the asset class level, the most appropriate portfolio allocation, according to their investor profile. This is called strategic asset allocation and provides an efficient framework to preserve capital over the long term. Efficient strategic asset allocation is indeed a critical source of portfolio performance stabilization in the long-run: 80% to 91% of the variability of a portfolio returns can be explained by the strategic asset allocation policy(1).

To go through the strategic asset allocation process, you will have to ask yourself upfront several key questions: what is my performance target, what level of loss can I accept, what are my liquidity needs, do I have specific deadlines (like retirement) or projects (an investment in real estate, the financing of my children’s studies, the sale of my private company, etc.)? Then, according to these objectives and constraints, the next step will be to define the right asset classes’ mix, covering all asset classes whether listed or non-listed.

The fundamental idea behind strategic asset allocation is to use diversification in the most efficient way possible.

More precisely, this is about leveraging three key parameters: first, understanding the specific risk-return profile of each asset class. Long term expected returns and volatilities are defined by asset class with a LT investment horizon based on the Investment Strategy publication. Secondly, assessing each asset class sensitivity to economic factors. Typically, equities do well during times of growth, but commodities do better during times of inflation. And, finally, measuring the intensity of connections between the different asset classes, including the non-traditional ones such as Private Equity, Real Estate, Hedge Funds, to combine them in the most efficient way. This is called correlation.

Of course, depending on the initial long-term requirements, the most relevant strategic asset allocation may vary. For example, let’s say you are about to retire, after investing for 30 years. In such a context, your major worry will be to clarify and optimize your portfolio allocation to pass it on smoothly to your children. Your “ideal” allocation will be completely different from that of a young entrepreneur who has just sold his company and envision creating a new business and launching important real estate projects. However, for both of you, the SAA process will help you take a step back, get a holistic view and answer key questions to eventually build the most efficiently diversified portfolio by asset class. This will be the backbone, the strong foundations of your asset allocation!

To conclude, Strategic-A, by defining the most relevant strategic asset allocation, acts as a cornerstone in a wealth management strategy. But other critical steps do come afterwards!

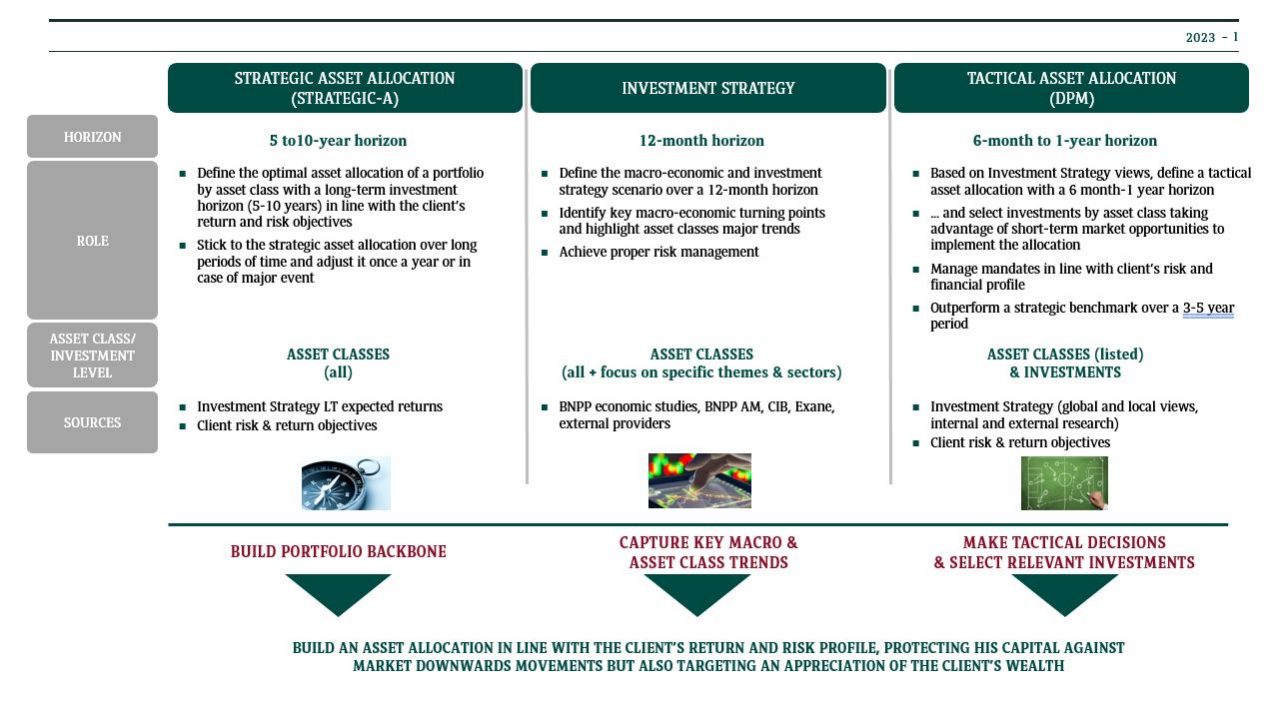

Strategic-A sets the long-term direction of diversified multi-asset portfolios for the long term according to a client’s risk and return profile.

The Investment Strategy team works more on a 12-month investment horizon. They set investment recommendations by asset class, investment theme and geography, industry sector and other factors for our clients with this investment time horizon in mind.

Academic research demonstrates that asset allocation remains a key driver of multi-asset investment portfolios over time, more so than stock picking or currency hedging for example. Effective asset allocation on a 12-month investment horizon can deliver risk-adjusted outperformance when done in a rigorous manner, by identifying key asset class trends and also by identifying key macroeconomic turning points.

On the one hand then, we look to capture the major uptrends in the various asset classes such as stocks, government bonds, corporate bonds and alternative assets in our published recommendations. In this way, we seek to improve client investment portfolio returns over time by capturing the bulk of these positive trends.

But on the other, we also look to actively manage risk over this time horizon for clients, notably by taking a more cautious stance in our recommendations when necessary. This typically occurs at key macro turning points as signaled by economic recession, major geopolitical events or even times of acute financial stress. Effectively, avoiding the bulk of the resultant negative trends for asset classes to reduce portfolio drawdowns is just as important in protecting long-term portfolio performance as is capturing positive asset class trends.

Discretionary portfolio management offering is covering a large range of mandates with different level of risks (from low to high). These levels of risk are related to the weight of assets from the less risky (as cash or bonds) to the riskier one (as equities for example): we calibrate the weight of each asset class according to the client’s desired level of risk.

In order to structure a mandate a so-called strategic benchmark is designed with defined assets classes’ weight. This benchmark is a mock-up of expected risk/return of the mandate on a medium to long term horizon (3-5 years).

With Discretionary Portfolio Management, the client delegates the analysis, selection of the best investments and constant monitoring of his portfolio to a team of portfolio managers.

The objective of the portfolio manager is to beat the strategic benchmark’s performance by taking allocation (asset classes, countries, and duration for bonds) and selection (stock, funds and bond picking) decisions. In order to beat the benchmark those decisions are of 3 types: be underweight, in line or overweight the different asset classes’ weight of the benchmark.

For example, if the conviction is that equities will over-perform the other asset classes, then the portfolio manager will overweight this asset class compared to benchmark. If the portfolio manager is right, for the equity part, the mandate will register an added value on top of the benchmark return.

This is what we call a tactical asset allocation as this decision is made for a shorter-term horizon (6 months to 1 year) than the strategic benchmark.

BNP Paribas Wealth Management has defined a global asset allocation process in order to make sure there is a consistency between the Investment strategy scenario as defined by the Investment Strategy and the tactical asset allocation decisions made by the local Asset Allocators. The objective is to ensure clients’ comprehension regarding the global communication of the strategic scenario of Wealth Management and what he sees in his personal mandate.

For clients who have had performed a Strategic-A analysis on their global wealth, a discretionary mandate can be implemented and managed on a part of their strategic asset allocation in line with the client’s objectives.

Finally, whether Strategic-A, Investment Strategy, or Discretionary Portfolio Management (DPM), they all aim at building the most relevant asset allocation for the client, in line with his objectives and risk profile. But while targeting the same goal, each of them plays its own critical part, being complementary to each other! In a nutshell Strategic-A defines the framework at the asset class level with a long-term horizon, the Investment Strategy adjusts it with a shorter time horizon and finally DPM, with a view to outperform the reference index at the end of the management mandate, applies tactical moves on investment products with short term views.

- (1) ”A global approach to Strategic Asset Allocation and a review of country specificities”, Vanguard Research - August 2016. The observation period runs from January 1990 to September 2015. Calculations were based on monthly net returns, and policy allocations were derived from a fund’s actual performance compared with a benchmark using returns-based style analysis (as developed by William F. Sharpe) on a 36-month rolling basis. Only funds with at least 48 months of return history were considered, and each fund had to have a greater-than-20% long-run domestic and international equity exposure (based on the average of all the 36-month rolling periods) and a greater-than-20% domestic and international bond allocation over its lifetime.