A market undergoing transformation

We are delighted to present our annual publication, which includes an analysis of the main trends in the French rural market, enriched with our experience on the ground.

In France and in other European countries, the agriculture, viticulture and forestry sectors are at a crossroads. Following years of continuous growth, the economic climate is redefining future prospects. The downturn in the markets and economic concerns are opening up new avenues for investors who are interested in these sectors and ready to capture the transformations underway. Indeed, these changes are necessary and relevant, particularly as one in two farmers will be retiring over the next decade. Needless to say, the renewal of generations and the transmission of farms will be a challenge.

The rural market offers some real advantages. More than ever, sector players and investors seeking alternative solutions should monitor market evolutions. By adopting a strategic vision and a longterm approach, it is possible to benefit from this uncertain period to seize fresh opportunities.

Indeed, rural land in France remains a prime asset. Its valuation, albeit fluctuating in the short term, is anchored in solid fundamentals, namely a growing need to source and secure food and non-food products, a greater interest in agricultural sovereignty and higher societal demand for sustainable practices.

When building an investment portfolio, rural land can be a strategic asset, if carefully selected. Besides, it is a relatively inexpensive, safe-haven and diversifying asset that is uncorrelated from other markets, as well as being an excellent vehicle for transmission purposes.

Finally, investors should have good advisers to help them identify emerging trends and participate in this sector transformation to grow wealth for future generations.

Head of Agrifrance – BNP Paribas Property SNC

Last year was one of the ten wettest since 1959, but also among the five hottest on record. A great deal of bad weather and downpours led to repeated pluvial and fluvial flooding in some regions. For eight months, soils remained wetter than normal, which had not been seen for more than 30 years.

The average temperature in France for 2024 was 13.9°C or 0.9°C higher than the normal temperatures in 1991-2020. Cold spells were rare throughout the year, the winter was mild, and the warm weather arrived earlier than usual, in March. Rainfall in France amounted to 69.76 millimetres per month in 2024 (+12% vs. 2023 which was an average year compared with the annual normal during the 1991-2020 period). Farms and vineyards faced several episodes of severe weather, including spring frosts, summer hailstorms, excessive rainfall causing mildew, as well as insufficient sunshine. These conditions not only affected yields, but also deteriorated crop quality. However, after two particularly dry years, the abundant rain spurred the growth of grass and forests between March and November 2024.

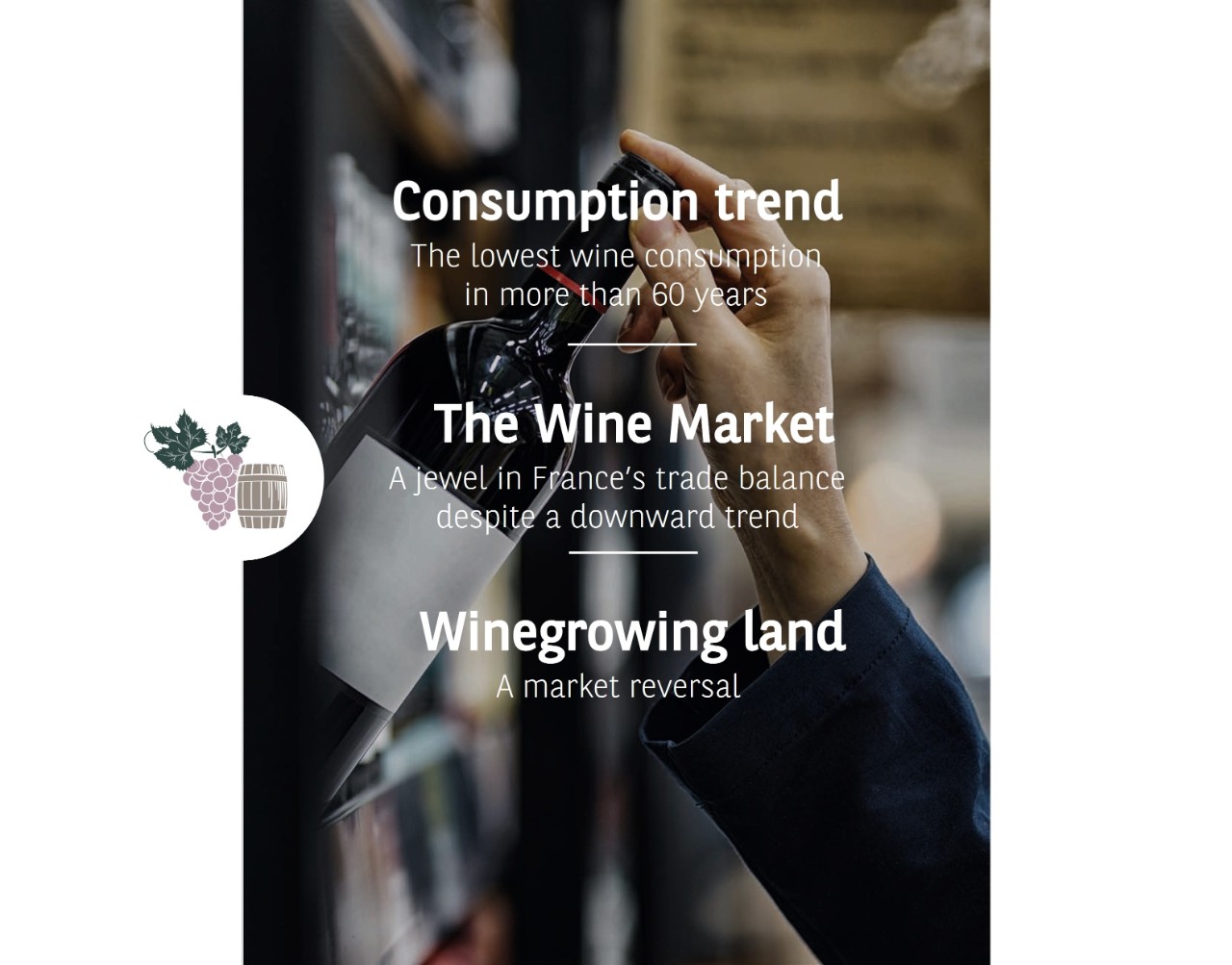

According to the International Vine and Wine Organisation (OIV), owing to adverse weather conditions, global wine production in 2024 reached its lowest level since 1961. It is estimated at 226 million hectolitres, representing a 4.8% decrease versus 2023, which was already a small harvest. The three main wine producers are Italy, France and Spain (49% of global wine production and 80% of European production) were affected differently.

Italy leads the way with production estimated at 44 million hectolitres (15% higher than 2023, which registered an exceptional low). This volume is nevertheless 6.2% lower than the five-year average, owing to adverse weather conditions, including hailstorms in the north of the country. France ranks in second position, with production estimated at 36.1 million hectolitres in 2024, representing a significant decrease of 23% versus 2023. The 2024 vintage was 17.9% below the five-year average. This decrease was mainly due to adverse weather conditions throughout the year affecting all regions, with particularly sharp declines in Champagne (-46%),

Burgundy (-38%) and Charentes (-37%) in addition to more moderate declines in the South of France. Spain maintains its third position with an estimated production of 31 million hectolitres in 2024, an increase of 9.3% versus the previous year. This increase was partly due to relatively satisfactory harvests in regions, such as Castilla-La Mancha and Extremadura, despite the country facing challenges related to water stress.

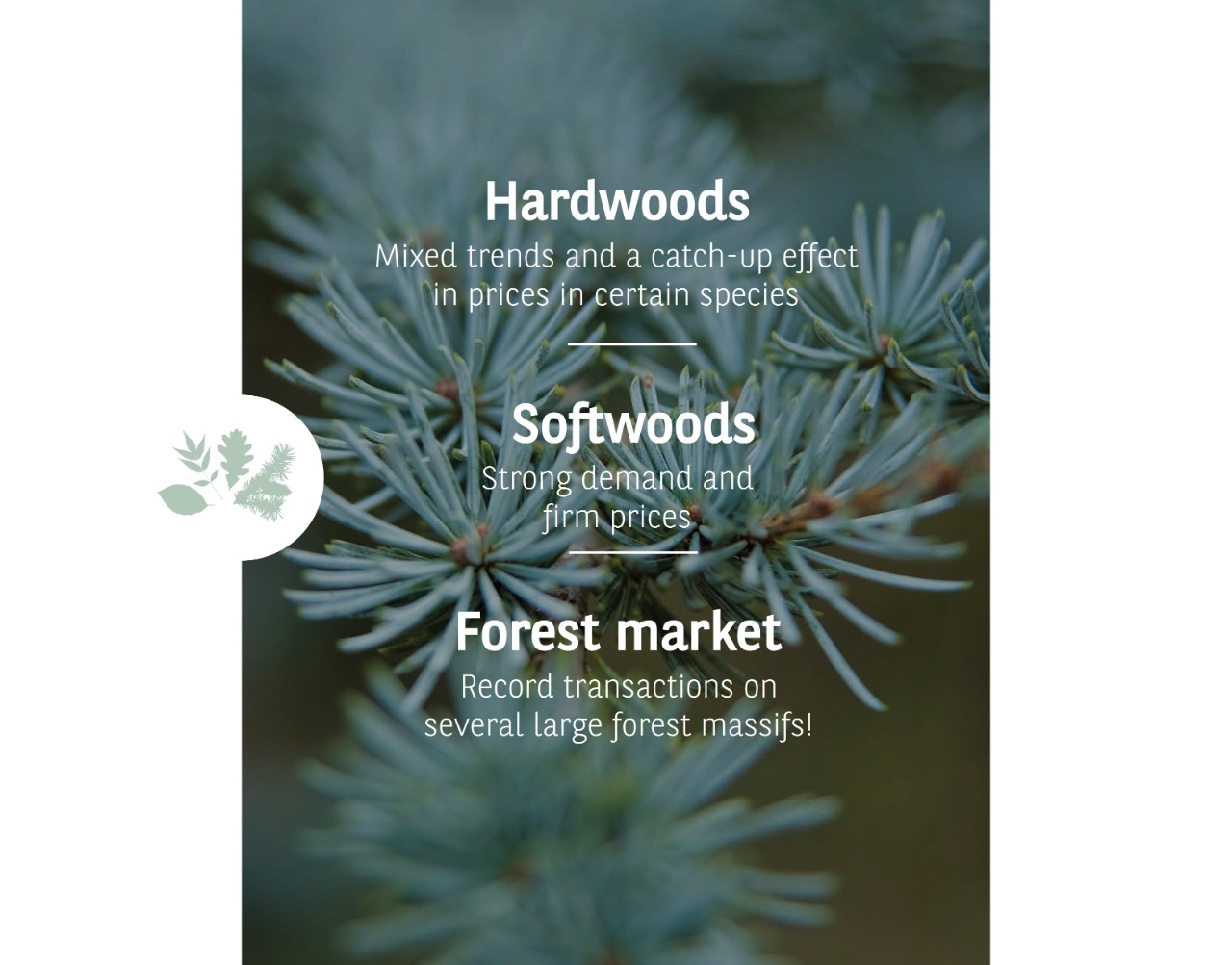

The trade war, begun by President Trump and confirmed by his “Liberation Day”, is disrupting international capital flows. This situation could significantly hurt the global timber trade. Moreover, America is one of the largest consumers of roundwood*, whereas China is the largest importer of roundwood, planks and residual chips/sawmill off-cuts used for pulp manufacturing.

Geopolitical tensions, the reversal of international alliances, as well as rising inflation in the US are fuelling instability on the market. According to the Fédération des Experts Forestiers de France, the timber market deteriorated substantially in the second half of 2024 amidst an uncertain political environment and a continued fall (-21%) in the number of housing starts over two years. These factors have dampened demand for wood in France and internationally.

However, exceptional rainy conditions delayed woodcutting, which reduced the available stocks on the market, and paradoxically created a new market momentum. This analysis was confirmed by the ONF, which indicated a 5% decrease in volumes sold in 2024 (1,160,311 m³). That said, the decline in hardwoods was partly offset by a greater supply of softwoods.

The long-term outlook for the timber market remains promising, especially thanks to the increasing demand for energy sources, which could durably drive the sector.