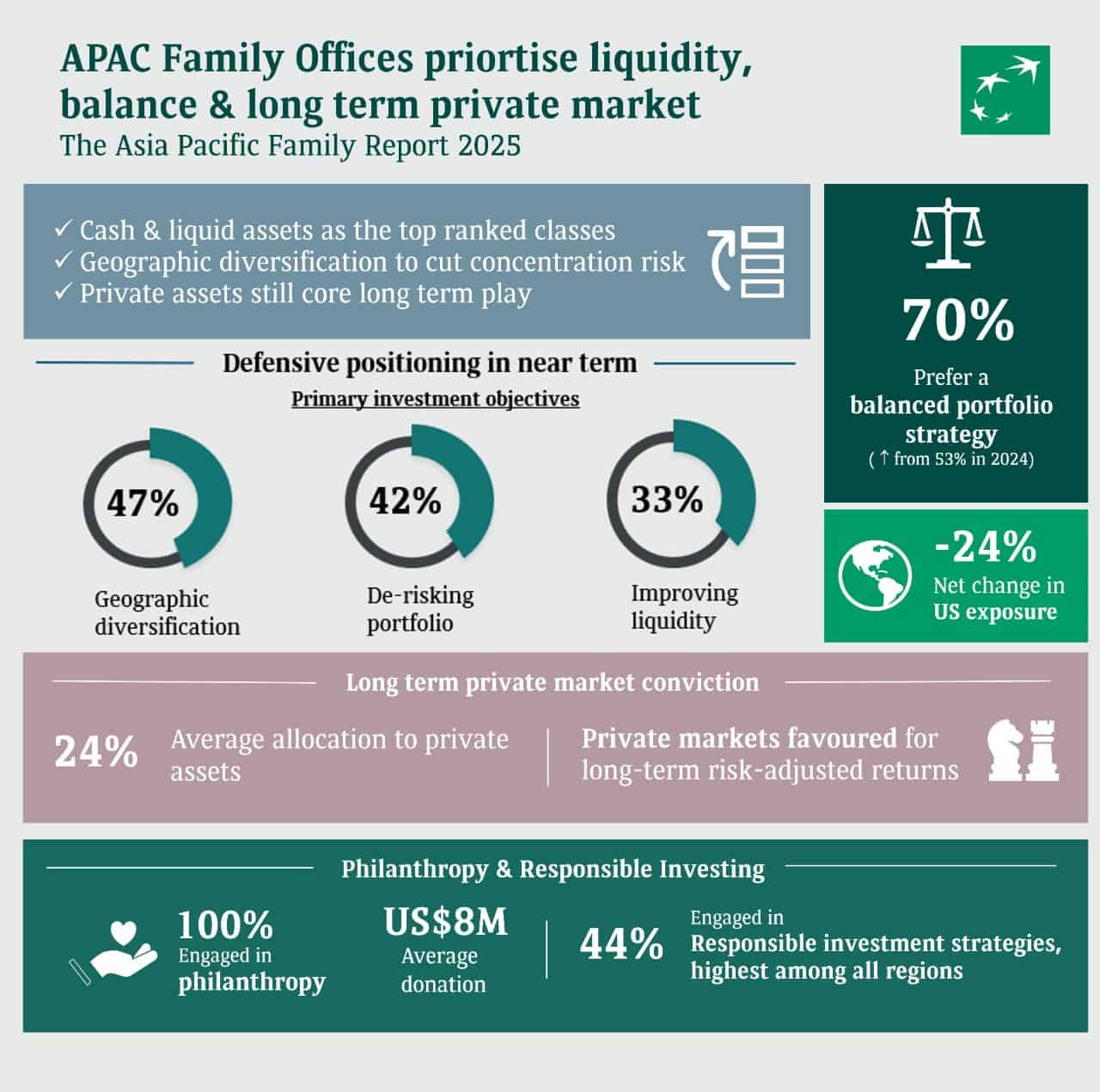

Asia-Pacific family offices prioritise liquidity and balance, with a long-term conviction in private markets

- Cash and liquid assets top the 12-month outlook with increasingly balanced portfolio

- Philanthropy is universal, with a shift toward structure and governance

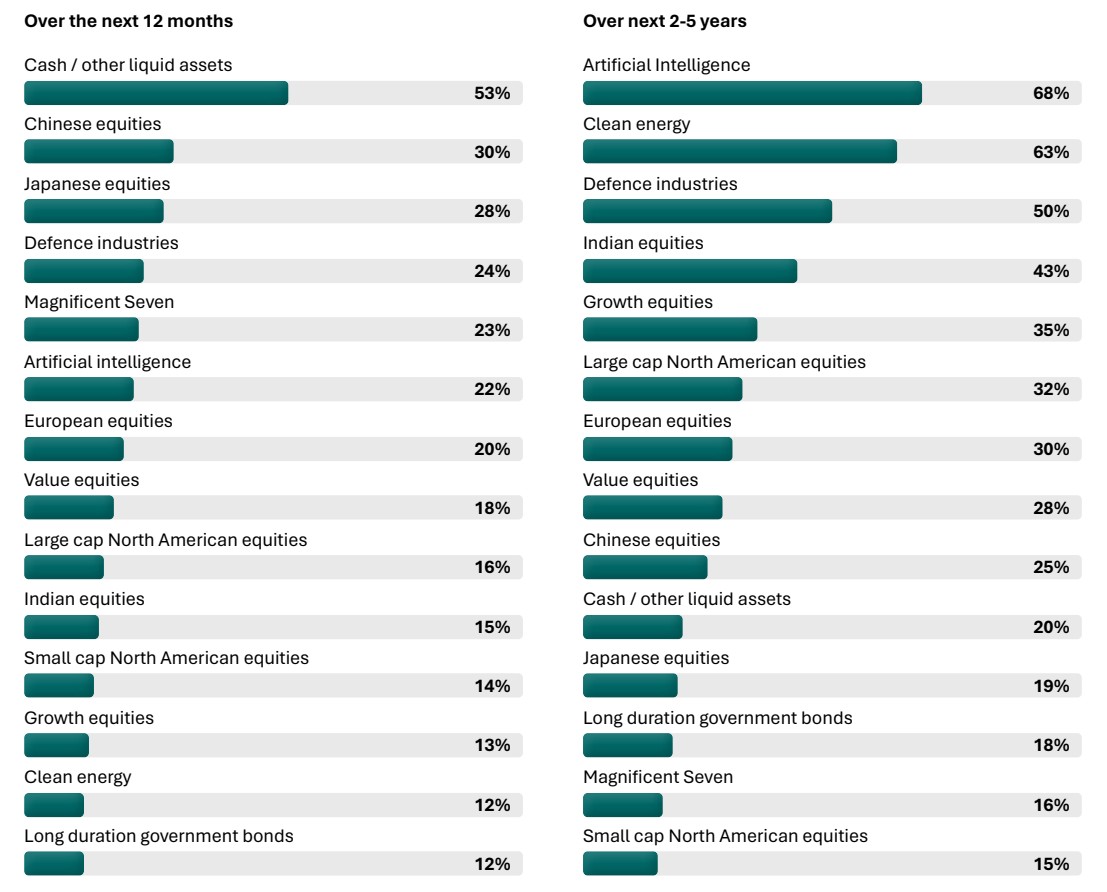

The report, sponsored by BNP Paribas Wealth Management and produced by Campden Wealth reveals a more cautious approach compared to 2024, when growth equities was the dominant theme. In contrast, cash and liquid assets are the top-ranked asset class for the next 12 months (Fig. 1), alongside a clear shift toward balanced portfolio strategies, at the time of the survey, which took place between March and June 2025. Respondents’ average expected return for 2025 is approximately 6%, reflecting tempered expectations and a focus on resilience amid heightened market volatility.

Fig.1 Percentage of family offices selecting asset class/investment theme as likely to reward shareholders

“Recent geopolitical events have served as a reminder that markets can reprice unexpectedly across various assets. Although the report provides a snapshot of intentions for 2025, its message remains timely: building resilience through diversification, preserving flexibility through strategic asset allocation, and ensuring portfolios remain aligned with the family's broader objectives, including philanthropy."

Arnaud Tellier, CEO Asia

BNP Paribas Wealth Management

Near-term stance: liquidity, balance, and diversification

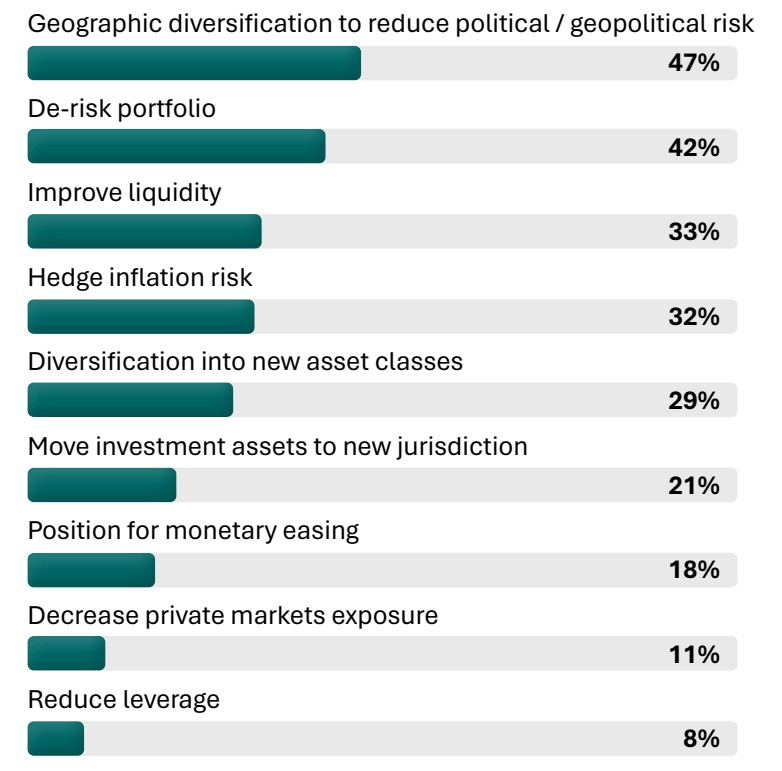

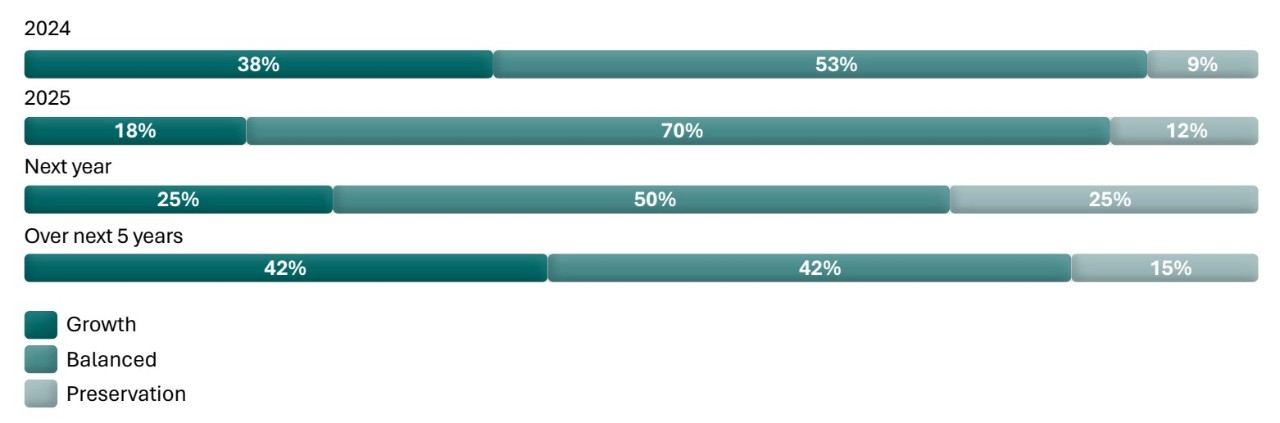

Family offices cite portfolio construction goals that emphasise risk management and flexibility. The report finds that the respondents’ primary 2025 objectives were: geographic diversification to reduce concentration risk (47%), de-risking portfolios (42%) and improving liquidity (33%) (Fig. 2). This is reflected in strategy choices with balanced strategies rising to 70% in 2025, up from 53% in 2024. (Fig. 3).

Fig. 2 Primary investment objectives for 2025

Fig.3 How family offices describe their investment activity

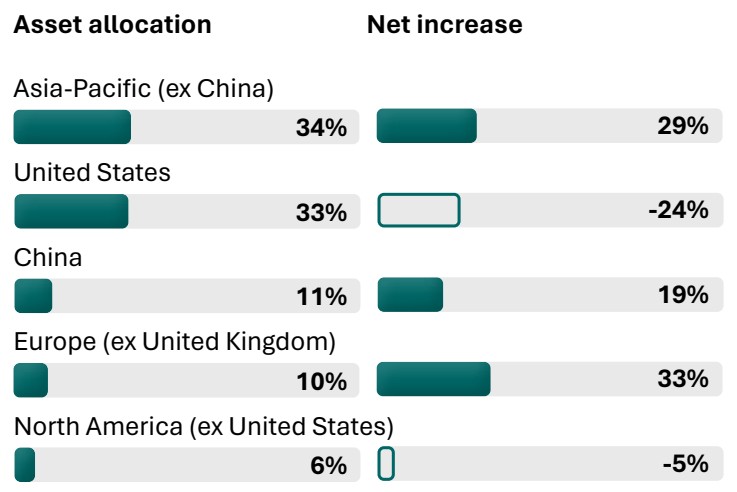

While the United States remains a significant allocation at 33% of current geographic exposure (Fig. 4), the report indicates a net intention to reduce US exposure (−24%) (Fig. 5) consistent with broader diversification and risk management objectives. These intentions align with the respondents stated objectives around diversification and risk management.

Fig. 4 Geographic asset allocation and percentage of family offices

intending to increase holding less percentage intending to decrease

Long-term conviction: private markets remain core

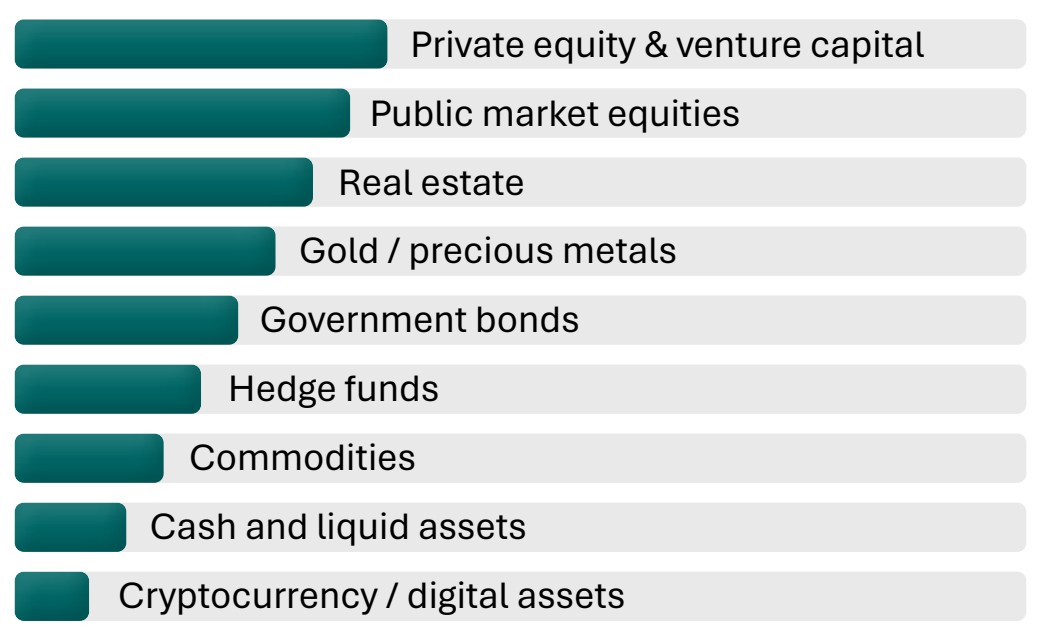

Despite a cautious near-term stance, the respondents maintain meaningful exposure to private assets. The report finds private assets represent 24% of the average portfolio and continue to be viewed favourably for long-term risk-adjusted returns (Fig. 5), even as recent performance has been mixed.

Fig.5 Ranking of asset classes by expected risk-adjusted return

Dominic Samuelson, CEO, Campden Wealth, said: “Family offices in Asia-Pacific are balancing short-term caution with long-term conviction. While liquidity and resilience are front of mind, they continue to view private markets as a key driver of multi-generational wealth and are applying increasing discipline to succession planning, governance, and philanthropy.”

Chung Kah Yi, Head of Private and Alternative Investments for Asia, BNP Paribas Wealth Management, said: “Private markets remain a strategic allocation for many families. The focus is increasingly on disciplined manager selection, pacing, and structures that can improve flexibility, so families can stay invested across cycles.”

Philanthropy: universal participation, with a shift toward structure and governance

Alongside investment strategies, family offices across the region are also prioritising philanthropy, with 100% of the respondents in Asia-Pacific engaged in philanthropy (Fig. 6), and an average philanthropic donation of US$8 million (equivalent to 0.8% of family office AUM on average).

Fig. 6 Percentage of families engaged in philanthropy

Philanthropy is becoming an increasingly important aspect of family office activity. The report also highlights a governance gap: only half of the offices have a formal succession plan. Those that do are far more likely to embed their charitable activity inside a family foundation or purpose‑trust.

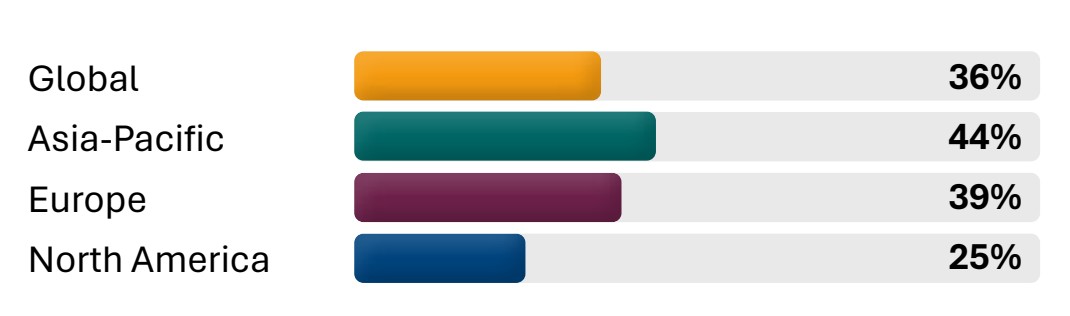

Responsible investing is also gaining traction, with 44% of the respondents in Asia-Pacific actively engaged in responsible investment strategies (Fig. 7), and 91% of them agreeing that responsible investing does not necessarily require sacrificing return. Unlike other regions, Asia-Pacific has maintained consistent momentum in responsible investing, demonstrating a stable and enduring commitment to sustainable investment practices.

Fig. 7 Percentage of family offices engaged in responsible investing

Mae Anderson, Head of Philanthropy Services Asia, BNP Paribas Wealth Management, said: “In Asia we see philanthropy evolving from episodic giving into a strategic governance tool. By routing charitable giving through purpose trusts and family foundations, families are creating legal and operational scaffolding that not only safeguards their legacy but also accelerates next generation education. The data shows that offices with formal succession documents are far more likely to run structured impact investment workshops for heirs, reinforcing the idea that giving and governing are now two sides of the same legacy building coin.”

Read more about the report here