Equity Perspectives - First Issue, 2026

📑HK / China Updates

📑US Updates

📑Europe/UK Updates

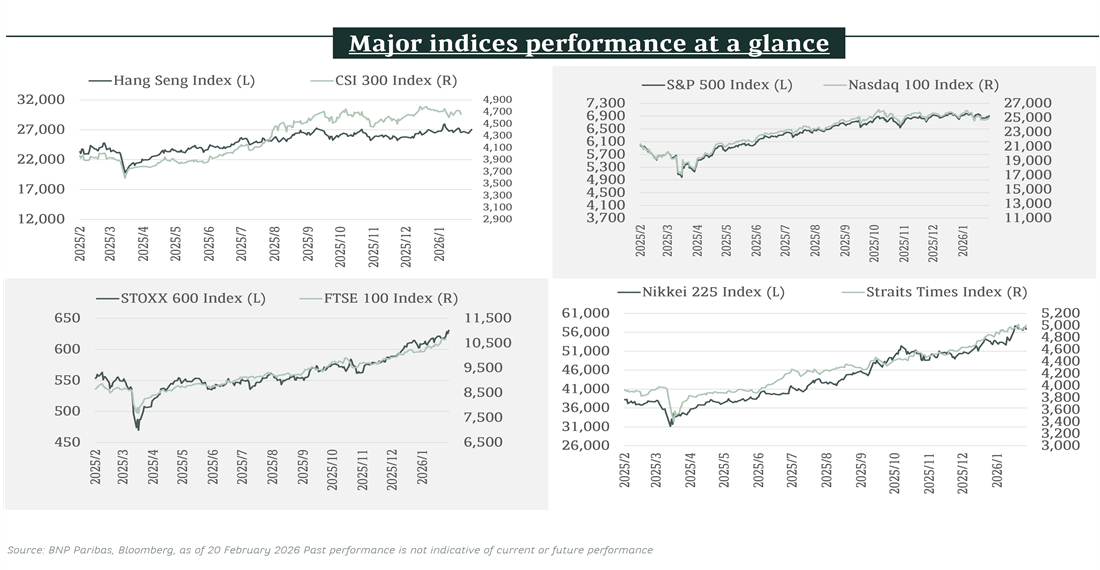

MARKET SNAPSHOT

- Global stock markets have been bumpy so far in 2026 amid a backdrop of geopolitical and economic uncertainties. Optimism surrounding AI also turned into concerns of industry disruption and overheated valuations. Defensive/real economy sectors gained, while technology pulled back.

- We still see AI as a multi-year theme. The recent pullback provides a solid entry opportunity into select leaders of the technology, in our view.

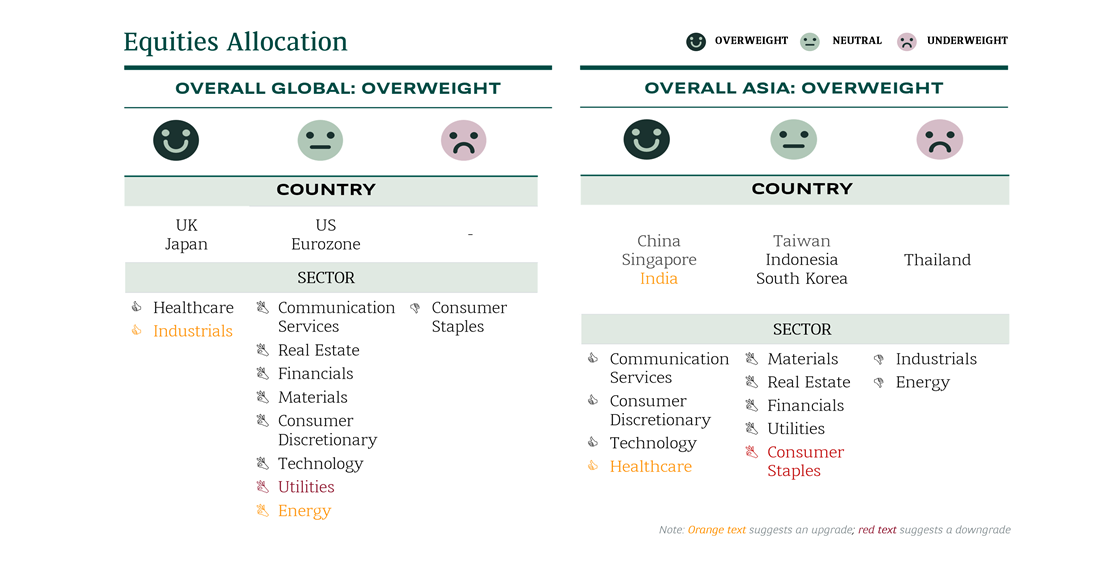

- We remain overweight HK/China equities, supported by pro-growth fiscal expansion and moderately loose monetary policies. All eyes are now on China’s Two Sessions kicking off in early March 2026.

- We are selective on US and EU stocks, with relative preference on quality leaders and strong balance sheets, as well as domestic European businesses geared towards the region’s supportive fiscal policies.

What happened?

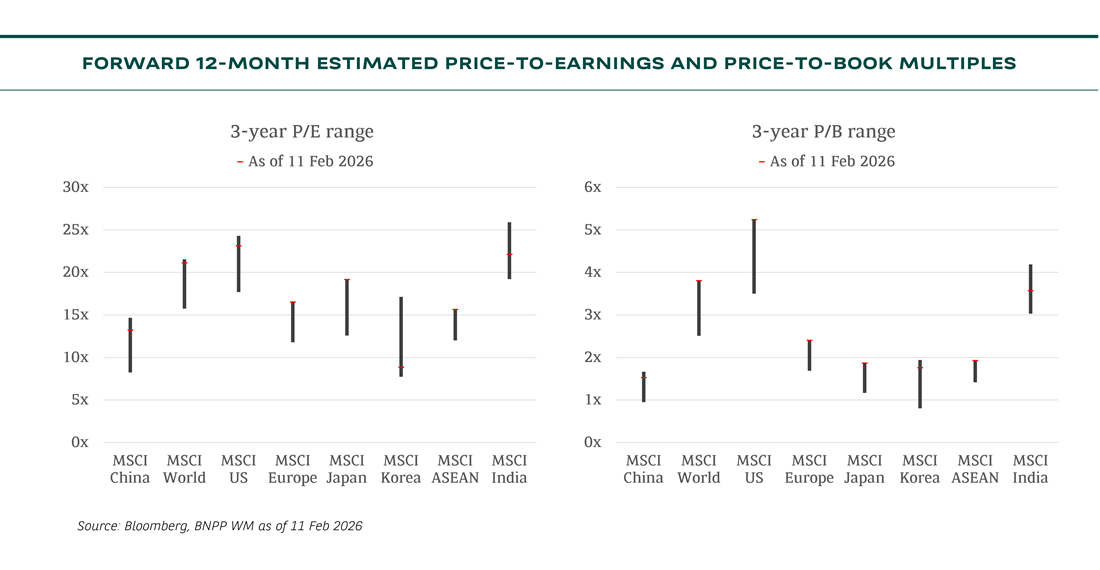

HK/China stocks had a spectacular run in 2025 with the MSCI China Index surging 28%, which outperformed MSCI US, Europe and Japan. However, valuations of HK & China stock markets remain undemanding against peers, though many markets are trading at or near 3-year high levels (see chart below).

Our thoughts

Looking ahead, all eyes are on China’s Two Sessions kicking off on 4 March 2026. Major national policies will be passed during the Two Sessions, whilst the country’s top leaders are expected to announce GDP growth target and fiscal stimulus. It is noteworthy that among the 31 municipal governments that have published local 2026 GDP targets, 18 are expecting slower growth, 12 are anticipating flat growth and only Jiangxi forecasts faster growth. Consensus China GDP growth for 2026 stands at 4.5%, representing a mild slowdown from 5% in 2025, according to Bloomberg. Details of upcoming fiscal stimulus to be released after the Two Sessions are likely to compel fund managers to rebalance their portfolios accordingly.

While pro-growth fiscal expansion and moderately loose monetary policies should be strong tailwinds for 2026, we are also mindful of a bumpy stock market in the near-term. Sharply heightened volatilities of other asset classes may disturb fund flows, which could have temporary knock-on effects on HK/China stocks.

How to play the game?

🎯Areas on our radar: The upcoming 15th Five Year Plan, amendments to the Pricing Law, fixed asset investments in Western China, and fiscal stimulus.

🔎Investment implications: China’s Five-Year Plan is the blueprint for economic policies that often determine winning and losing industries. For example, the current 14th Five Year Plan unambiguously supports transition to new energy vehicles and curb housing speculation, which led to distinctive performances in these two sectors in 2021-2025. Investors are advised to reconstruct their portfolios according to the 15th Five Year Plan.

Notable Developments in Selected Sectors

- Platform economy - Investors are unnerved by probes into food delivery platforms and an online travel agent, as well as the establishment of a “negative list of algorithms”. However, near-term regulatory hiccups are unlikely to derail long-term growth. The Chinese central government unequivocally supports domestic high-tech development that policies are expected to remain accommodative in the next few years.

- China New Energy Vehicle (NEV) - Unit sales of NEVs fell sharply in January 2026, amid scheduled resumption of purchase tax on NEV. Chinese NEV demand is likely to remain subdued in the first half of 2026, whilst potential roll-back of Europe’s additional import duties on Chinese-made electric vehicles would provide much-needed fresh air to the leading China NEV makers.

What happened?

US equities have continued to lag World equities year to date, underscoring our relative non-US equity markets preference, with volatility experienced in the equity market driven by AI disruption concerns. While remaining constructive on the multi-year growth story of the AI theme, we stay neutral on US equities given elevated valuations and currency headwinds, although FY26E earnings delivery is expected to remain healthy supported by solid sales growth and margins in a lower rate environment.

Our thoughts

US equities have been largely rangebound so far this year (as of 19 Feb 2026), which have underscored our selective stance on the equity market. Sector returns have been quite divergent, with double-digit percentage gains so far this year for Energy, Materials, Industrials and Consumer Staples, which we believe reflect investors’ efforts to diversify their portfolio exposures amid longer term AI disruption worries and spike in geopolitical tensions after the US intervention in Venezuela early this year.

The Q4 2025 corporate reporting season has delivered strong sales and earnings per share (EPS) beats, with EPS growth averaging at about 12% year-on-year, driven by Financials and Information Technology sectors. Excluding the impact of the largest stocks in the S&P 500 index, the median company is estimated to have registered +9% EPS growth in Q4 2025. US cyclicals reported stronger growth than defensives for a second quarter.

Post results, street estimates have modestly lifted for MSCI US, with FY26E EPS growth forecast at ~16.3%, driven by solid EPS growth expected from Technology (+36%) and Materials (+22%) sectors.

Hyperscaler capex plans have again surprised on the upside, which weighed on share buybacks and point to a combined USD650b spending plan expected for 2026. Within the technology sector, FY26E earnings growth this year is still expected to be led by the semiconductor industry given the ongoing AI infrastructure buildout, which should keep the sector in investors’ radar. Recent post-results commentary have also shown a further increase in the number of firms across sectors discussing AI disruption. While elevated AI capex, circular financing and a potential AI bubble are valid medium-term risks to monitor, we believe it is too early to make premature conclusions as enterprise adoption and software firms are still in an early stage of developing AI-enabled offerings. Valuations of MSCI US Technology sector remain well below levels reached during the 2000-2001 internet bubble, which burst with Fed rate hikes, vs more cuts expected. Recent technology sector pullback reflect investors’ portfolio de-risking efforts in our view, with accumulation points emerging for select technology & software leaders positioned to deliver better AI monetization over the medium term.

How to play the game?

🎯Areas on our radar: Hyperscaler capex plans, economic growth trajectory, Fed rate decisions

🔎Investment implications: Maintain prudence and diversification, favouring quality firms with healthy balance sheets.

Notable Developments in Selected Sectors

- Energy - Geopolitical tensions have underpinned the recent outperformance by energy stocks. The US intervention in Venezuela has been supportive for refiners along the US Gulf Coast that could benefit from the heavy sour crude that Venezuela is known for. Oilfield services companies could also directly benefit from oil company capital expenditure in the country. More recently, US military buildup in the Middle East, aimed at putting pressure on Iran, has led to a surge in oil prices, further supporting sector names.

- Materials & Industrials – Industrial metal prices have risen on solid global demand and limited supply, driving gains in both Materials & Industrials sectors. With an ongoing multi year commodity cycle supporting sector earnings, we stay constructive on commodity producers and select industrials positioned to benefit from electrification demand and AI infrastructure tailwinds.

- Information Technology - The S&P IT sector faced headwinds recently with intensifying memory shortages and a selloff triggered by Anthropic’s new AI model capabilities. However, mega-cap commitment remains robust, with USD650b in capex announced for AI infrastructure. We maintain a diversified approach focused on quality leaders to capture secular AI growth opportunities.

What happened?

European equities remained robust over the course of 2025, achieving further record highs in November 2025 and outperforming the S&P 500 in both local currency and dollar terms. The Spanish, German and Italian markets led the way.

Our thoughts

We maintain a Neutral rating for European equities with a relative preference for domestically-oriented businesses that are geared towards the region’s expansionary fiscal framework.

2025’s unprecedented fiscal spending plan in Germany, supporting both infrastructure and defence spending, was a key starting point for improved sentiment towards the wider European market. While German industrial growth has been challenging, opportunities are likely to emerge from Europe’s focus on rejuvenation and structural investment, albeit at a slower, more pragmatic pace than initial market optimism suggested.

Separately, investors have found further catalysts aligned with structural themes (e.g., renewable energy and AI), while an end to the Ukraine-Russia conflict would offer positive investment opportunities. The European Central Bank (ECB) rate-cutting efforts have supported an expansionary environment, though we are coming to the end of the cycle. Investors’ focus now shifts to fiscal spending plans.

Key to the earnings picture will be whether currently challenged sectors (e.g. Autos, Chemicals, Media, Consumer Staples) significantly recover in 2026, while they still face major disruptions coming from AI, China and new consumption habits. We have seen downward earnings revisions to companies with high US exposure, given the strength in the Euro, and this will be a focus going into 2026. Nonetheless, stronger European GDP growth should support, with consensus expecting earnings growth of ~10% in 2026. European stocks still trade at reasonable valuation levels (the Stoxx 600’s Price to Earnings (P/E) of 15.8x, as of 13 February 2026).

Separately, the FTSE 100 hit a new record high in February 2026 as investors sought out defensiveness during a period of AI-inspired market volatility. Trade agreements in recent months with the US, EU and India were helpful in terms of sentiment, while last November’s Autumn Budget was less onerous than many had forecast. Although the market is not as aggressively cheap as it was at the start of 2025, the UK still offers value, trading on 14.3x forward P/E for the FTSE 100 as of 13 February 2026.

How to play the game?

🎯Areas on our radar: Front-end loaded fiscal and defence spending in 2026; an end to ECB and BoE rate-cutting cycle.

🔎 Investment implications: Infrastructure and defence spending to become key driver of opportunities, given the lower support from monetary policy.

Notable Developments in Selected Sectors

- Financials: The Stoxx Banks index has now seen five years of continuous outperformance relative to the Stoxx 600. The sector has survived a dividend ban in 2020, Russia’s invasion of Ukraine in 2022, the Credit Suisse collapse in 2023, as well as US tariffs and fears over private credit in 2025. Although the sector has re-rated, we expect this relative “stability” feature to persist in 2026, as a favourable operational backdrop remains supportive.

- Materials: A global “critical minerals” paradigm shift is underway. Global demand for metals and different sources of energy continues to grow, partly thanks to expanding technology investment, while supply remains constrained after years of underinvestment in new production capacity. 2026 could see miners proactively reposition for future opportunities in copper, gold, lithium and rare earths.

- Utilities: The sector is underpinned by the themes of rising European power demand growth, decarbonization, and increased demand for energy security and independence. Despite high debt and cost inflation, the sector has shown strong performance, particularly in power generation and networks, driven by regulatory support.

Please read carefully the disclaimer here: https://wealthmanagement.bnpparibas/asia/en/disclaimer1.html