Equity Market Updates

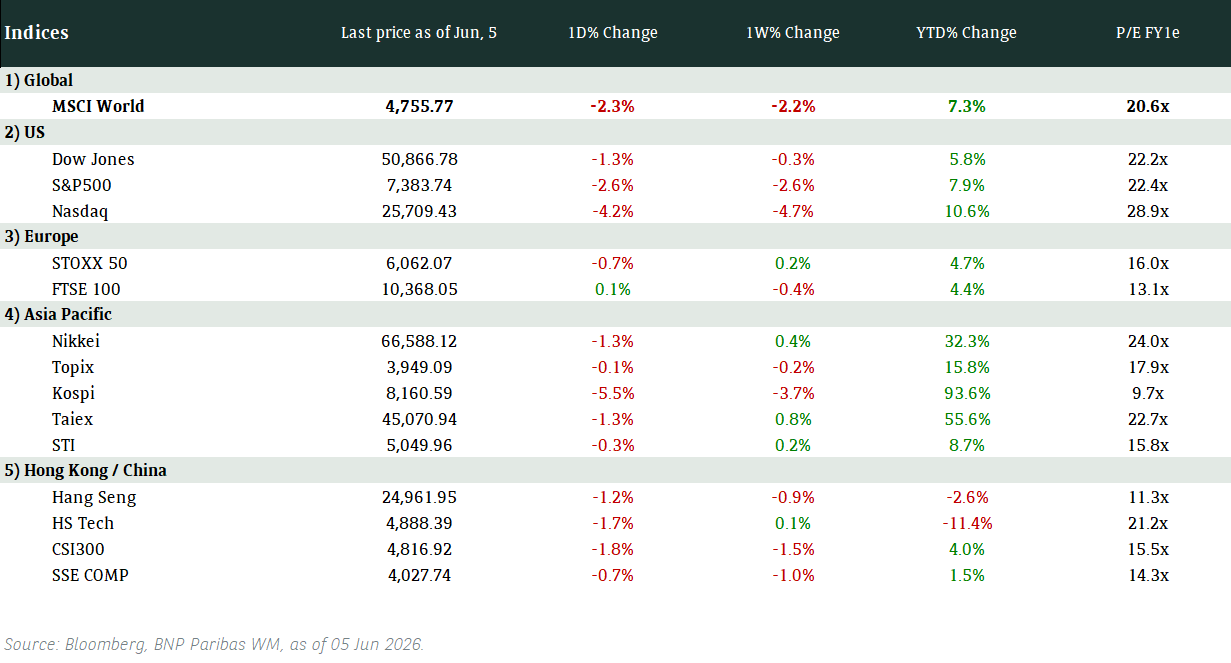

The key equity market focus this week will be the largest ever SpaceX IPO. Rule changes for SpaceX's "fast track" into prominent equity indices raise concerns about liquidity as large potential passive buying flows could imply significant selling pressure elsewhere, particularly after robust gains in semiconductors. In fact, equity markets were hit by a global sell-off in tech names last Friday. The Nasdaq 100 Index plunged nearly 5%, its deepest dive since April 2025.

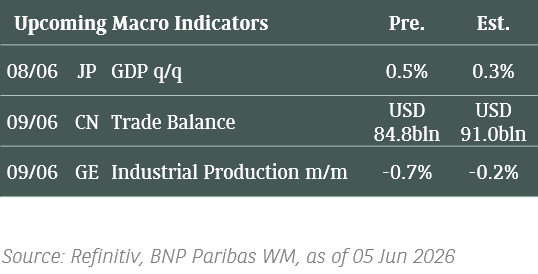

Market will also focus on the US Consumer Price Index (CPI) and Producer Price Index (PPI) numbers following the well above consensus non-farm payrolls report last Friday. The market moved to fully price in a 25bp hike from the Fed by year end. More evidence of inflationary pressure could see risk of further market repricing for the future Fed rate path.

The third focus will be on the European Central Bank (ECB) meeting this week. We expect the ECB to re-engage with tightening for the first time since 2023. With a hike widely expected, the focus will be on whether this is just part of a re-calibration of policy in the face of the energy shock, or the start of a longer-lasting cycle.

Equity Market Updates

Global equities fell on Friday amid concerns of an overstretched AI rally. Major economic reports and the SpaceX IPO this week further dampened risk sentiment.

Investors looking to seek shelter amid global volatility could consider UK equities and their defensive characteristics as well as relatively undemanding valuations.

SK Hynix (000660 KS)

SK Hynix announced today a multi-year technology partnership with Nvidia to advance next-generation memory as well as accelerate semiconductor design and manufacturing. Through this partnership, SK Hynix will co-develop memory for Vera Rubin AI supercomputers, Vera CPUs, RTX Spark-Powered PCs, and Thor robotic computing platforms.

MARKET CONSENSUS: 46 BUYS, 1 HOLD, AVERAGE TP KRW2501220

Alphabet (GOOGL US)

Alphabet’s Google announced on Friday that it had entered into a multi-year cloud services agreement with SpaceX to lock in computing capacity. As part of the deal, alphabet will pay SpaceX USD920mln monthly from October this year to June 2029, with capacity ramping up through September at a reduced fee. The compute capacity provided includes about 110,000 Nvidia GPUs, CPUs, memory and other related components.

MARKET CONSENSUS: 67 BUYS, 8 HOLDS, AVERAGE TP USD431.64

Meta Platforms (META US)

Meta is reportedly considering raising tens of billions of USD in a stock offering as it seeks new sources of capital to fund its AI ambitions. The report came after Alphabet recently moved to raise almost USD85bln in equity offerings. The world's largest tech companies are increasingly turning to debt and equity markets to fund AI infrastructure investments, marking a shift from their longstanding practice of funding investments largely with cash..

MARKET CONSENSUS: 74 BUYS, 6 HOLDS, AVERAGE TP USD820.76

Boeing (BA US)

Boeing is reportedly exploring raising production of its bestselling 737 jet beyond its publicly stated target of 63 aircraft per month. The target would likely test the resilience of Boeing’s supply chain and bring its production plans closer to rival Airbus’ output goals for its competing narrowbody family.

MARKET CONSENSUS: 26 BUYS, 5 HOLDS, 1 SELL, AVERAGE TP USD271.42

Earnings Announcements

Global Indices Changes (%)

Fixed Income Market Updates

With a strong jobs number and some risk-off last Friday, we expect the market to be cautious ahead of US CPI and PPI data this week. Any further dips are likely to be bought although this month has several high-profile events hence expect volatility. We would rebalance from expensive high beta credits into lower beta.

European Bank Coco (AT1)

Resilient market in AT1 despite the weakness seen in rates and equities over in the US. Slight weakness in USD longer calls (newer issues), and Euro remains resilient for now. HSBC, the outlier, traded weak on the back of headlines regarding report of HK bank account curbs, -25c across most of the curve. Overall if stocks hold these levels, AT1 may continue to feel firm. But if we have another day or so of equity volatility and cash coming out, we may begin to play catch up. Overall, selected AT1 bonds still look favourable for carry.

Asia Investment Grade (IG)

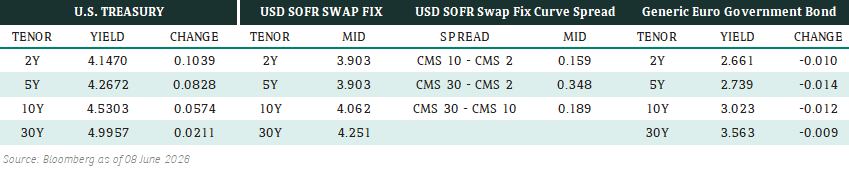

Credit spreads were 1-3bps (basis points) wider across Japan and EM. Kospi -8.8% at the open last Friday triggered a circuit breaker at the open. 10Y UST broke 4.5% (4.55% as of this morning) following the blowout jobs report on Friday. US IG is expecting ~30bn of new issuance this week. Rate hike narrative spurred a selloff in rates. Although this might aid high-quality spread products with corresponding higher all-in yield, cognizant though that we are heading into summer lull, so not sure how much of it will materialize.

Asia High Yield (HY)

HY cash opened lower on cash (-0.25-0.5pt) and spreads were wider as well (+5-10bps) with US HY closing 3bps wider as supply and tech weakness weighed on credit. Overnight flows were mostly mixed with real money covering underweights into the weakness during the US session while Asia was mostly sellers going into close. In the opening today, most benchmarks were down, but given the nature of Asia Mondays, don't expect much real money follow up into it but instead feel like we will see two-way flows from fast money.

Forex Market Updates

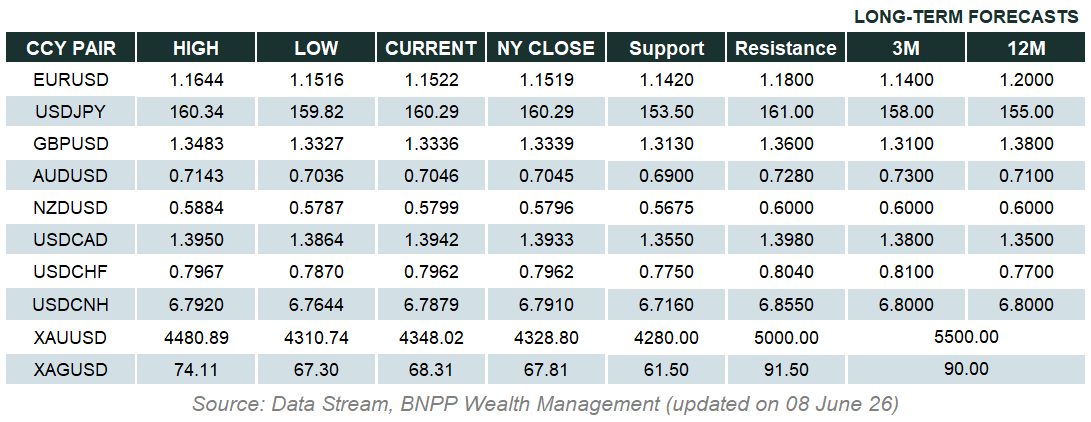

The US Dollar posted strong gains on Friday thanks to a blowout US jobs report.

USD

The US Dollar was Friday’s best-performing major currency as yields on US Treasuries rose after data showed that the US economy posted a third consecutive month of strong job gains in May. The NFP report confirmed that the US labour market remains on a strong footing in 2026 after stumbling last year, which gives the Fed more room to keep interest rates on hold in the near term amid rising inflation due to the ongoing Middle East conflict. Ahead of incoming Fed Chair Warsh’s first FOMC meeting on 17th June, analysts said that the blowout jobs report is likely to ease concerns among Fed officials about labour market weakness and allow them to focus their attention on inflation risks. Markets moved swiftly to bump up the odds of a Fed rate hike in December to around 68% from 50% before the NFP report, with Fed policymaker Hammack lending her support for policy tightening by commenting that inflation is “moving higher” and that it may soon be “appropriate” for the central bank to act if recent trends continue. In the Gulf, military skirmishes between the US and Iran continued over the weekend amidst the fragile ceasefire, complicating efforts to end the war between the two countries.

The Dollar Index should remain well supported above 98.85 in the near term.

EUR

The Euro weakened at the end of the week, closing at two-month lows against the USD after the release of strong US jobs data. Despite expectations of up to three ECB rate hikes this year, the first of which is likely to come later this week, analysts said that “the perpetuation of elevated energy prices” is likely to remain a drag on Eurozone activity and weigh on the common currency moving forward. With the economy of the 21-country bloc weaker now than during Europe's previous energy crisis in 2022, economists believe that EU policymakers are walking a challenging tightrope as they try to contain rising prices without exacerbating the growth hit from the ongoing Middle East conflict. Given the rise in European firms' selling price expectations as well as higher medium-term consumer inflation expectations since the start of the war, ECB Chief Economist Lane said that the central bank is almost certain to have to make upward revisions to its inflation forecasts. On the currency front, the most prominent warning sign now of more EUR weakness to come, from a technical analysis perspective, is a classic head-and-shoulders top forming on the monthly chart.

The common currency could see further near term weakness towards technical support around 1.1420.

GBP

The British Pound retreated around 0.6% on Friday in the face of broad USD strength, while data showed that UK house prices fell short of forecasts by dropping 0.1% on a month-on-month basis in May. The figures represented the latest sign of cooling in the market as higher borrowing costs and uncertainty caused by the US-Iran war weighed on property demand in Britain. On a year-on-year basis, prices were 0.5% higher, well below the 1.0% rise that was projected beforehand. A separate BoE survey published on Friday showed that UK businesses expect to increase prices less quickly in the year ahead than they did in April as some of the initial energy price shock caused by the Iran war fades. Markets expect the BoE to stand pat on rates at 3.75% this month but are currently pricing in around 44bps of tightening by the end of 2026. Elsewhere, political uncertainty looks set to loom over the UK for the foreseeable future after Labour Party member Andy Burnham said that he would seek to enter any potential party leadership contest should he win a by-election in the northwest of England on 18th June.

UK political uncertainty looks poised to keep Sterling price action capped below 1.3500 moving forward.

XAU

Gold prices retreated sharply to close the week, touching 10-week lows after a stronger-than-expected US NFP report reinforced expectations that the Fed will keep interest rates higher for longer amid inflation concerns fuelled by the war in the Middle East. With the US and Iran continuing to trade military strikes despite a ceasefire being in place, a peace deal has remained elusive, keeping the Strait of Hormuz virtually shut and oil prices high, which has weighed on the precious metal. Bullion prices have fallen more than 18% since the start of the US-Israeli war against Iran as energy-linked inflationary concerns have trumped the safe haven appeal of gold. Looking ahead, this week’s US CPI data is likely to drive price action in the precious metal heading into next week’s FOMC meeting, where rates are expected to be kept on hold.

With little clarity over a US-Iran peace deal, gold prices are likely to remain under pressure for the time being with $4,225 the next key support level.

Please read carefully the disclaimer here:

Asia Disclaimer:

https://wealthmanagement.bnpparibas/asia/en/disclaimer1.html

Europe Disclaimer:

https://wealthmanagement.bnpparibas/ch/en/disclaimer.html